By Alexander Mende and Per Ivarsson at RPM Risk & Portfolio Management AB: For many investors, manager selection ultimately comes down to intuition, whether inspired by personal preferences for a particular trading strategy or in-person meetings with the portfolio manager. While intuition may have value, it is difficult to demonstrate that it consistently identifies sustainable alpha generation.

The alternative is systematic analysis of historical performance. However, this approach has its own limitations: it practically excludes discretionary managers, whose results are inherently difficult to repeat, and places excessive emphasis on past returns. The familiar disclaimer ”past performance is not indicative of future results” exists for good reason.

We propose a different approach: prioritize strategy selection over manager selection. Once you have identified a strategy you believe in, choose the manager, or managers, that best embody its defining characteristics.

For full disclosure, we are non-believers in consistent alpha of individual managers, at least with regards to Managed Futures, which is our area of expertise. There might be long-lasting outperformance of single managers, for example, in the L/S equity space. We just wouldn’t know about it…

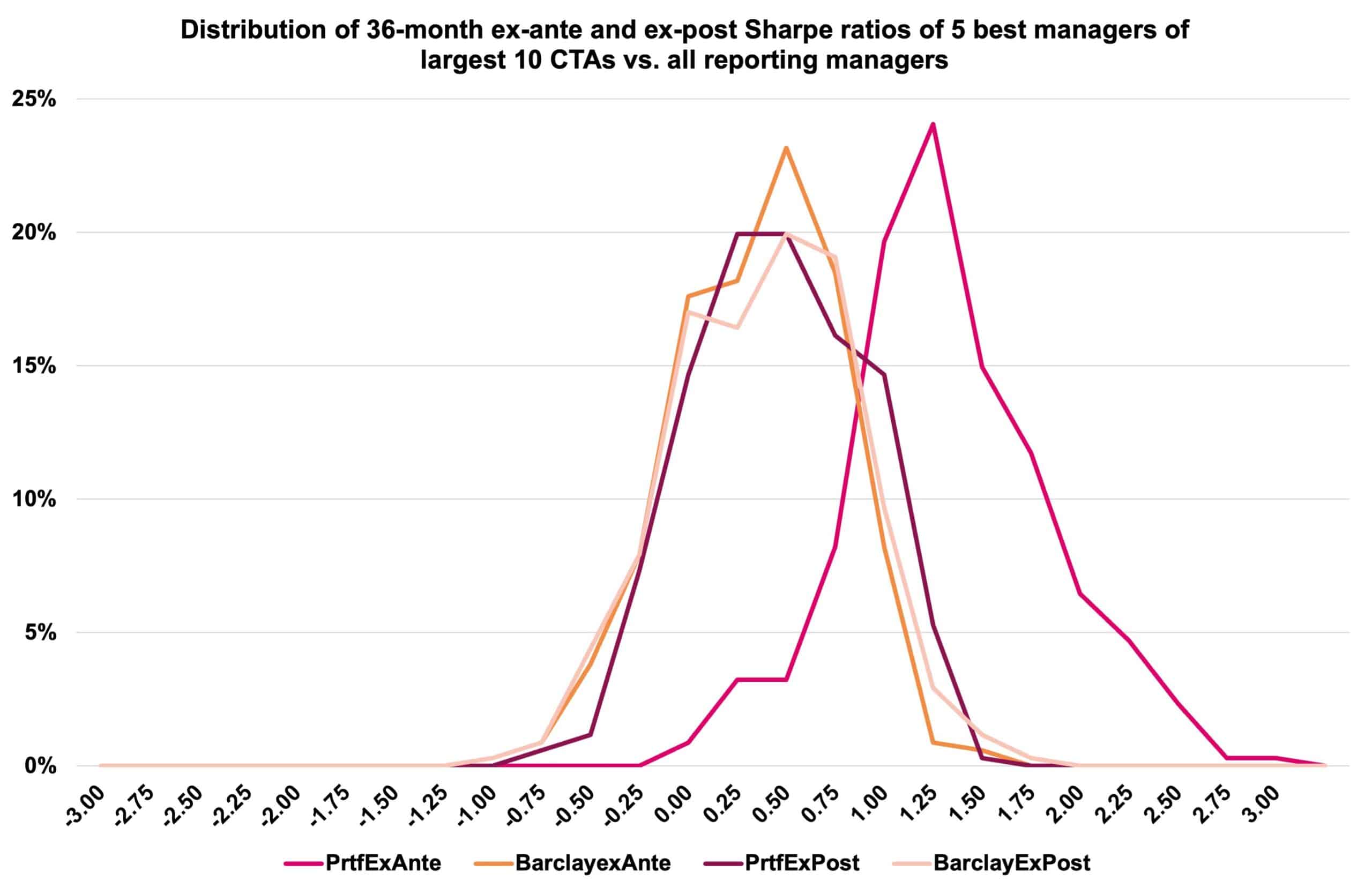

First, let us show once again that past (out)performance is a weak indicator for future returns, at least in the long-run. Figure 1 shows the distributions of 36-month rolling Sharpe ratios of all reporting managers to the Barclay Hedge database vs. the five “best” out of the ten largest CTAs (ex-ante) and the performance of the same managers after a potential investment (ex-post). As you can see, the previously identified outperformance vanishes after the point of observation. Managers still deliver benchmark performance, which is okay, but any alpha you thought you had identified disappears. This unsustainability of past (out)performance is especially true for systematic strategies as market environments change over time. What works well during one market regime does not work at all during another. Market regimes will reappear, in some shape, but the cycle is usually longer than most investment horizons. One can also note that investing in the ex-ante “worst” managers would also provide benchmark performance ex-post (however the survivorship bias is obviously strong in such analysis).

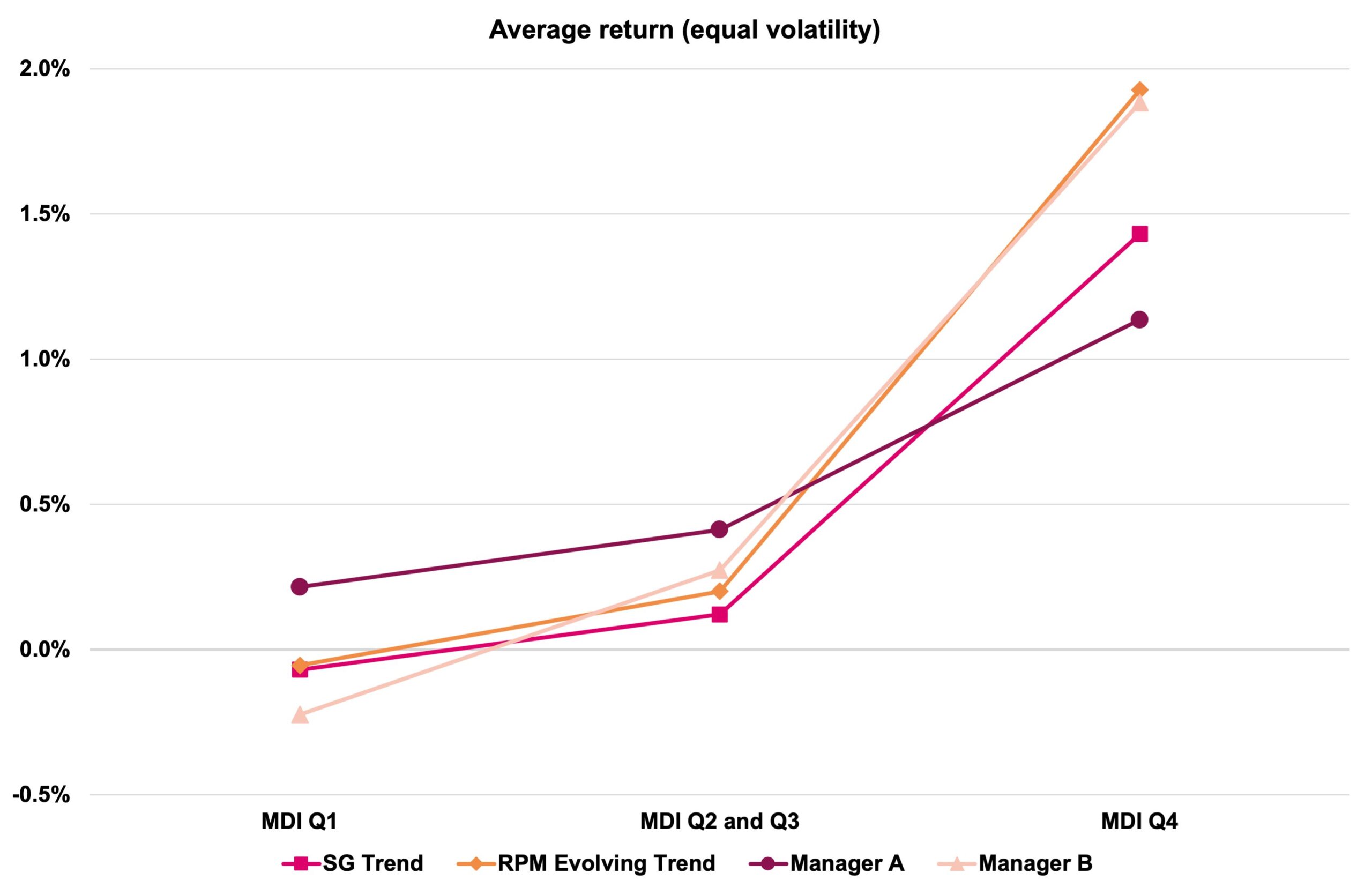

Now, let us illustrate how strategy selection can be done. The Managed Futures universe is dominated by diversified systematic medium-term trend following managers exploiting Time Series Momentum (TSMOM). In other words, most CTAs are trend followers generating profits in a trending market environment, i.e., when asset prices move substantially and sustainably in several different markets at the same time. Any trend following CTA should be able to capture TSMOM, by definition! That is what we would be looking for in a manager representing that strategy. Figure 2 shows the monthly performance of the SocGen Trend Index, of all trend following managers that have been part of the RPM Evolving CTA Fund (asset-weighted), and of two sample managers A and B for different MDI regimes (the Market Divergence Indicator MDI is RPM’s measure of TSMOM). As expected, the trend benchmark does best when MDI readings are in the fourth quartile; it generates (slightly) negative returns on average when there is very little to none TSMOM in financial markets. In contrast, the RPM trend index captures more TSMOM while not giving up more during choppy market periods, thus outperforming. This is achieved by dynamically allocating between managers that capture less trends but are able generate positive performance in non-trending market environments (Manager A) and managers that basically only capture TSMOM but underperform when there are no trends to be found (Manager B).

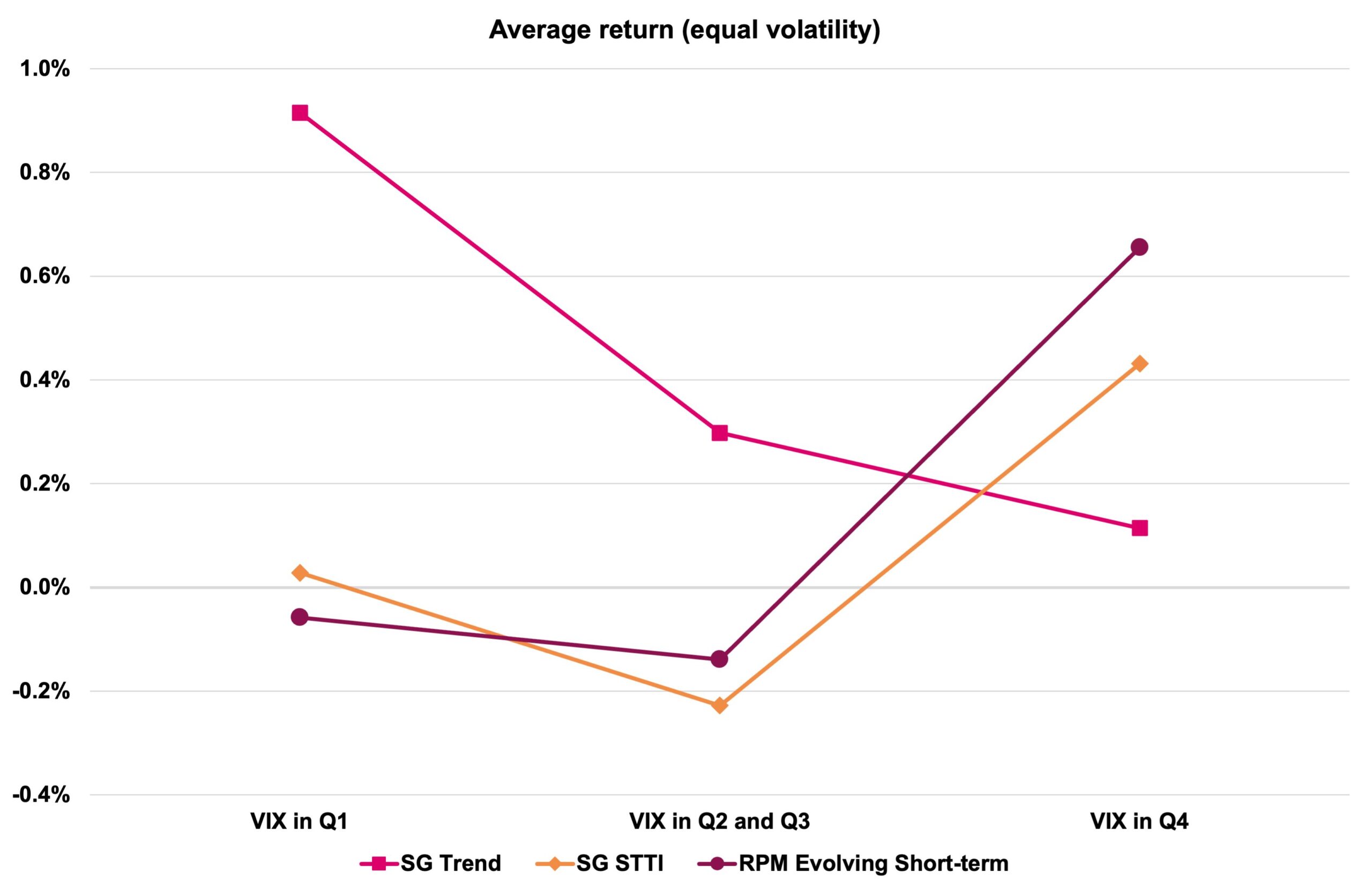

Once you have built your “perfect” trend portfolio, you can start working on overcoming the drawbacks of systematic medium-term trend following, i.e., give-back losses during major market reversals, which often occur when the VIX spikes. Similar to Figure 2, Figure 3 shows VIX regimes and the according performance of different CTA substrategy indices. Regarding monthly VIX levels, trend following CTAs perform poorly when market volatility spikes. Short-term trading managers, although they have, over time, underperformed slower systems, add value to a multi-manager portfolio during times of initial market distress. So, you want managers that perform best during high volatility market environments. No sooner said than done, RPM’s choice of short-term managers provides more protection during VIX spikes but performs slightly worse when everything is calm.

Hopefully, by now, we have been able to show the value of selecting strategies first before choosing which managers to pick. If this procedure generates sustainable outperformance is not a given, but it will at least provide the portfolio characteristics you have deemed necessary under certain market circumstances.

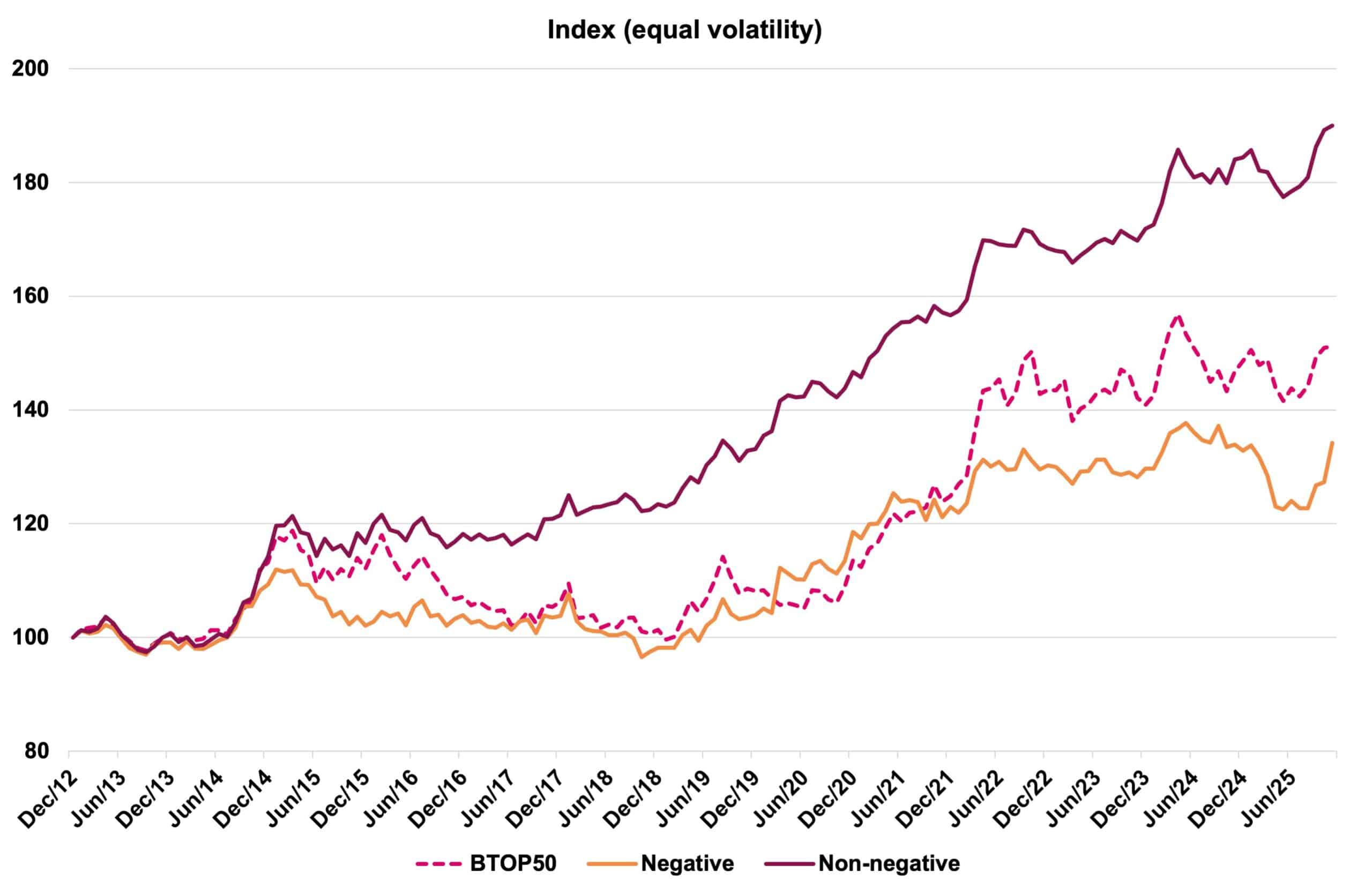

Now, let’s get back to the intuition decision making factor mentioned above. While we do not believe it is possible to identify manager alpha just by talking to a manager, it is possible to separate the wheat from the chaff, nevertheless. Figure 4 shows the (post meeting) performance of managers we met throughout the years after the initial meeting based on our subjective impressions. Apparently, it doesn’t matter if we intuitively like a manager or a certain strategy. However, once something smells fishy or doesn’t add up, this is a good warning sign to stay away. So, we not only crunch numbers but also listen to our collective “corporate gut”.

The lesson is simple: stop searching for the best manager and start building the best portfolio. Sustainable returns are less likely to come from identifying rare managerial genius than from combining complementary strategies that behave differently across market regimes. Manager selection should serve strategy selection, not the other way around.

And what about intuition? Use it as a filter, not as an investment thesis. Numbers tell you what a manager has done; strategy tells you what a manager is likely to do; intuition can help you avoid what neither reveals. In the end, successful investing is not about finding stars – it is about assembling the right constellation.