By Bjarne Graven Larsen: For decades during the great moderation, the 60/40 portfolio was the institutional investor’s Swiss army knife. Equities grew wealth; bonds benefitted from the secular deline in rates and cushioned the blows. The two assets moved in opposite directions when it mattered most. Investors slept soundly.

That sleep has become more restless.

When the Safety Net Frays

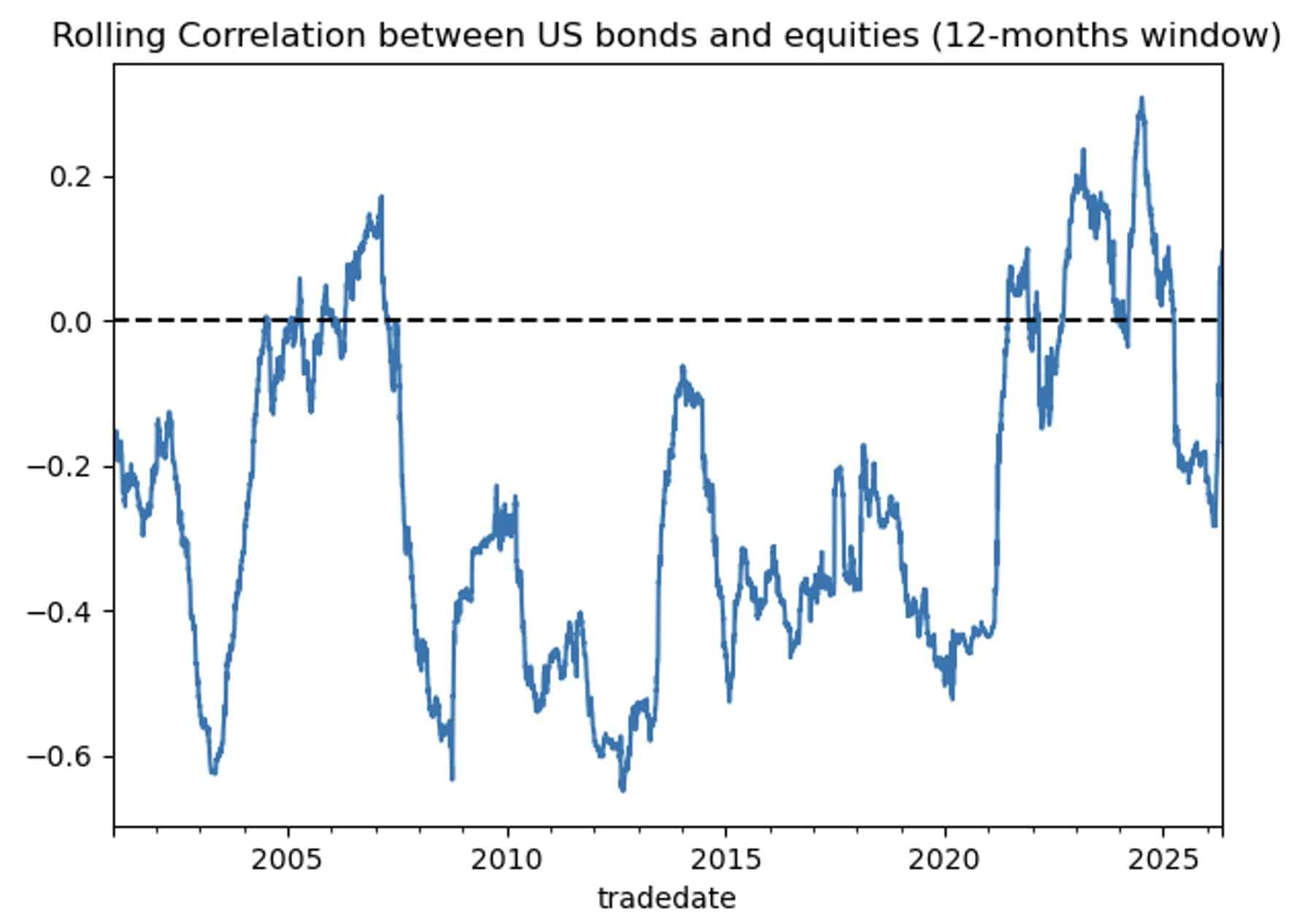

Since approximately 2021, the reliable negative correlation between equities and government bonds has been eroding. In the 2022 rate hiking cycle it disappeared entirely; bonds and equities fell in unison, delivering a simultaneous blow to traditionally balanced portfolios. The two-legged stool wobbled. The question every institutional investor now faces is simple: where do you find the third leg?

The Liquidity Trap

Many investors responded to the correlation problem by increasing allocations to private markets, including private equity, private credit, infrastructure. These can offer genuine return opportunities. But they come at a cost that is easy to overlook in calm conditions and impossible to ignore in turbulent ones: illiquidity.

During the COVID selloff of March 2020 and again during the Liberation Day tariff shock of early 2025, investors who needed to rebalance or reduce risk found themselves holding illiquid assets they simply could not sell. Simultaneously, the distributions from illiquid holdings slowed down significantly. Liquidity is like oxygen, you don’t notice it until it isn’t there.

This is the case for liquid, market-neutral alternative risk premia (ARP) strategies. An ARP strategy that is genuinely uncorrelated to equities and bonds and redeemable monthly offers something rare: diversification that actually works when you need it most[1].

Systematic Investing: Fundamentals, Without the Flaws

The word “systematic” can conjure images of black boxes. In reality, it is simply the disciplined, rules-based implementation of fundamental investment ideas: rigorously tested, academically validated, and robust across market regimes.

The intellectual foundations are well-established. Fama and French documented the Value and Size effects. Jegadeesh and Titman demonstrated that Momentum persists. Novy-Marx identified the power of Profitability. These are structural features of markets, underpinned by behavioural explanations that have survived decades of scrutiny. But in recent decades it has become increasingly clear that you need continuous improvements and innovation on how to harvest such premia as well as efficient trading to be successful.

The argument for harvesting these premia systematically rather than discretionarily is straightforward: humans are flawed. We extrapolate trends, anchor to recent experience, and become overconfident in bull markets. A systematic process removes those biases. It executes the same disciplined logic in February 2020 as it does in February 2021, regardless of what the headlines say.

Institutions like ATP, Denmark’s largest pension fund, understood this after the global financial crisis and rebuilt their investment approach around systematic, factor-based frameworks. This is not a new idea. It is a recipe that has been tested in real life.

The Transparency Advantage

There is an underappreciated argument for systematic strategies: transparency. Most discretionary managers will not tell you exactly what they own, why they own it, or what the portfolio’s true risk exposures are. A well-designed systematic strategy can and should do the opposite. When markets are stressed and your board is asking difficult questions, that transparency is not just reassuring. It is fiduciary.

What ARP Does to the Portfolio Maths

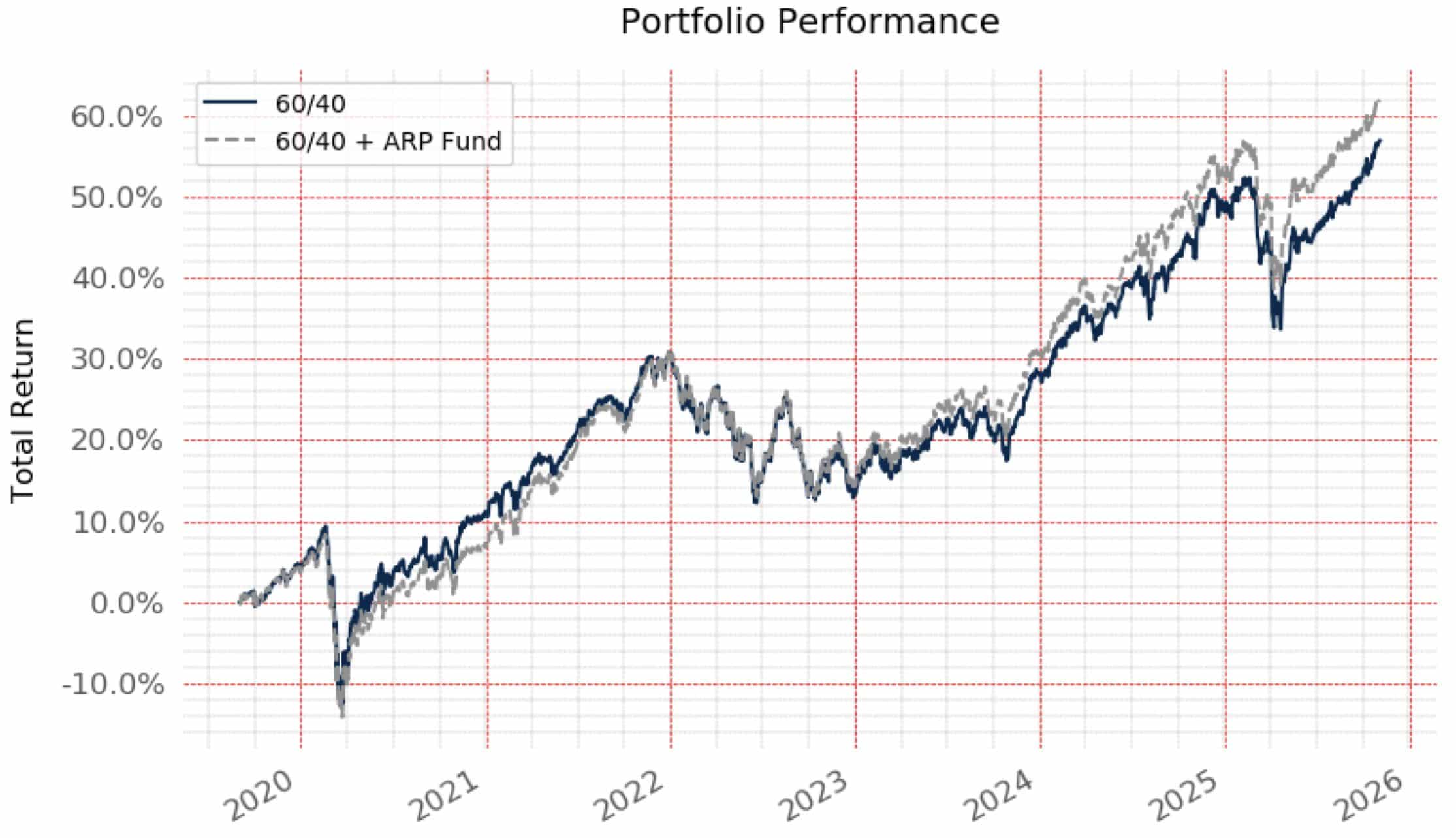

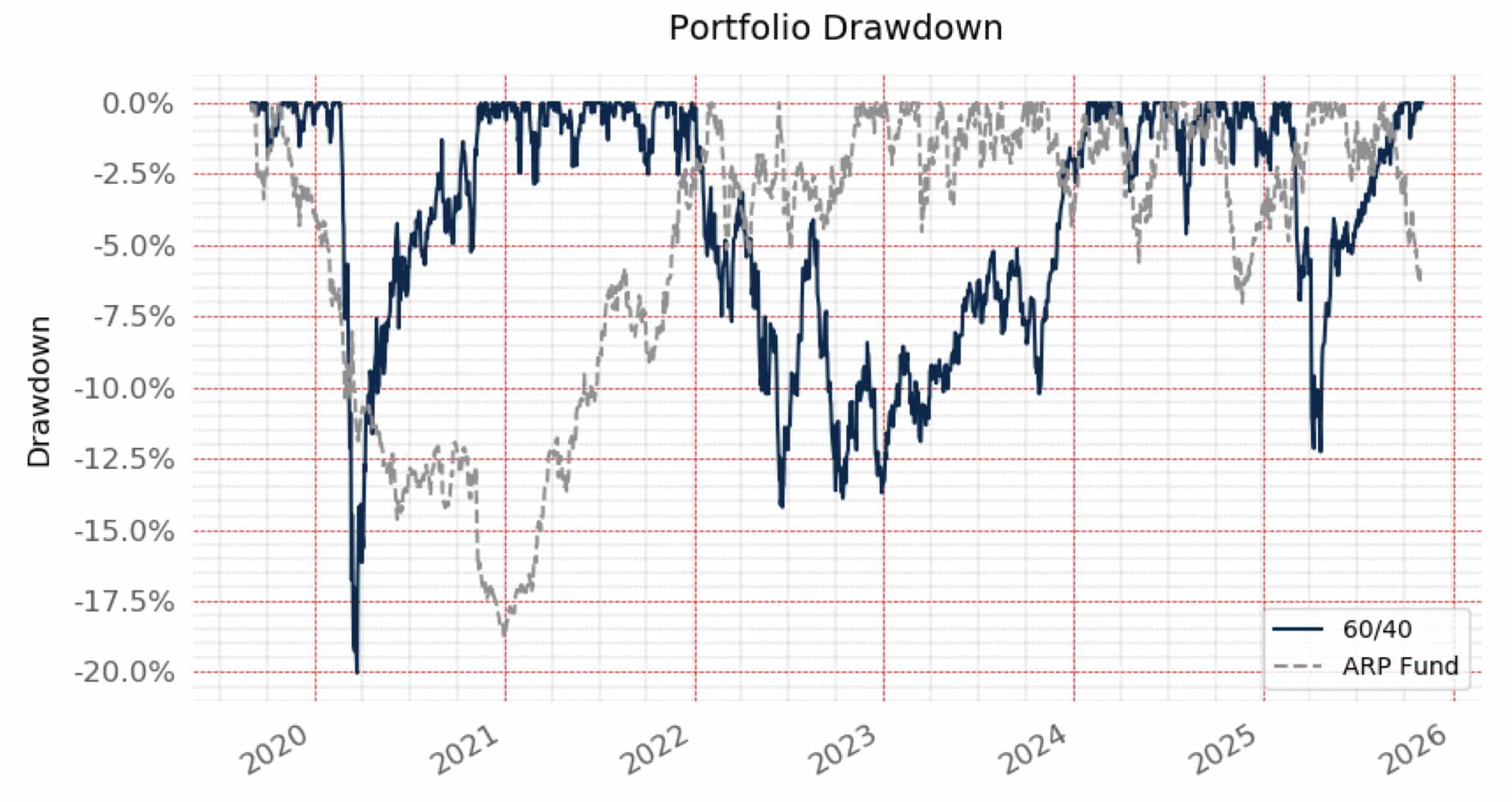

A standard 60/40 portfolio over the past three decades has delivered a Sharpe ratio, return per unit of risk, of approximately 0.54, which is quite good compared to long term historical standards. Introduce a 20% allocation to a well-constructed market neutral multi strategy fund and the Sharpe ratio improves to approximately 0.71. That is a 33% improvement in risk-adjusted returns, of which 25% is pure diversification benefit, with no increase in total portfolio risk.

The drawdown profile is equally compelling. In the COVID crisis, the 2022 rate hiking cycle, and the Liberation Day shock, a systematic ARP fund with genuine market neutrality, such as the strategy we manage, either held its value or appreciated while equities fell sharply. In the Liberation Day event alone, global equities fell 20.3%. The fund was up 6.8%.

This is not a tail-risk hedge. It is designed to be genuinely uncorrelated, day in, day out; a stabiliser rather than a second falling weight.

Where the Real Opportunity Lies

The well-known risk premia — Value, Momentum, Low Risk, Carry — are well-researched and intensely competed over. The more interesting opportunities lie in premia that require genuine expertise to design and implement.

Fixed Income Monetary Policy: Investors consistently underestimate the magnitude of rate movements during central bank intervention cycles, a persistent behavioural bias rooted in anchoring. A systematic monetary policy premium positions around the direction and pace of policy change, implemented across money market and bond futures. This strategy delivered a live Sharpe ratio of 0.69 since inception and was a material contributor during the 2022 hiking cycle.

Commodity Seasonality: Agricultural commodity prices follow predictable seasonal patterns driven by planting, growing, and harvest cycles. The opportunity is persistent, but implementation is everything. An outright short during the growing season carries catastrophic skewness when weather events strike. Trading calendar spreads instead of outright positions transforms the risk profile dramatically, delivering a live Sharpe ratio of 0.78 since 2019. Both strategies are proprietary risk premia developed and refined over a number of years of live trading.

Experience Is Not Optional

The difference between a robust implementation and a fragile one lies in the details: how you define each premium, how you control for unintended factor exposures, how you manage tail risk, how you execute efficiently at scale. These are not problems solved by reading papers. They require years of practice and the scar tissue that comes from managing real portfolios through real crises.

The team behind the strategy we manage has done exactly that: building and running large-scale systematic portfolios at leading pension institutions through the global financial crisis, the European sovereign debt crisis, COVID, and the most aggressive rate hiking cycle in a generation.

The Bottom Line

The 60/40 portfolio is not dead. But it is no longer sufficient on its own for an institutional investor who is serious about long-term, risk-adjusted returns and fiduciary responsibility.

Liquid, systematic, multi-strategy alternative risk premia offer what the traditional framework is missing, a third leg: uncorrelated, transparent, and accessible. The maths are compelling. The live track record is there. The only question is whether investors are willing to look beyond the familiar.

About the Author

Bjarne Graven Larsen is CEO & Founder at Qblue Balanced A/S, a Copenhagen-based systematic and sustainable asset manager founded in 2018. He was the, former CIO of ATP and Ontario Teachers’ Pension Plan. Qblue Balanced manages over USD 2 billion in assets for institutional investors globally.

Key Academic References

Fama, E.F. & French, K.R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics.

Jegadeesh, N. & Titman (1993). Returns to buying winners and selling losers. Journal of Finance.

Novy-Marx, R. (2013). The other side of value: The gross profitability premium. Journal of Financial Economics.

Ang, A. (2014). Asset Management: A Systematic Approach to Factor Investing. Oxford University Press.

Ilmanen, A. & Kizer, J. (2012). The death of diversification has been greatly exaggerated. Journal of Portfolio Management.

FI Monetary Policy and Commodity Seasonality are proprietary risk premia developed at Qblue Balanced A/S.

Disclaimer

This article is for informational purposes only and does not constitute investment advice or an offer to buy or sell any financial instrument. Past performance is not a guarantee of future results. Performance data referenced reflects the Qblue Alternative Risk Premia Fund. Back-tested results are hypothetical and may differ materially from live trading outcomes.

[1] The fourth building block, the liquid dynamic inflation strategy, is another important addition, which not covert in this article.