By Jesper Rangvid: We often hear about the strength of the US stock market, which is widely perceived to have vastly outperformed its European counterpart. However, since MSCI data collection began in 1970, the difference in performance is relatively modest, averaging just 0.8 percentage points per year. That said, a significant shift occurred around the time of the financial crisis. Prior to the crisis, European stocks outpaced those in the US, but since then, US markets have strongly outperformed Europe. If you had invested in European stocks in 2008, assuming their previous outperformance would continue, it would have turned out to be the wrong strategy. So, what should you do now, after a period of US market dominance?

If you were standing in early 2008, contemplating where to invest your money, you might have looked back and observed that the US and European stock markets had performed similarly over the long term, but Europe had strongly outpaced the US in recent years. Expecting this trend to continue, you might have decided to invest in Europe. In hindsight, that would have been a poor decision. Now, as you stand here considering where to invest your money, you might look back and see that the US and European stock markets have performed similarly over the long term, but the US has strongly outpaced Europe in recent years. Where should you invest now?

When comparing stock markets, we typically use MSCI indices, which were first introduced in 1970.

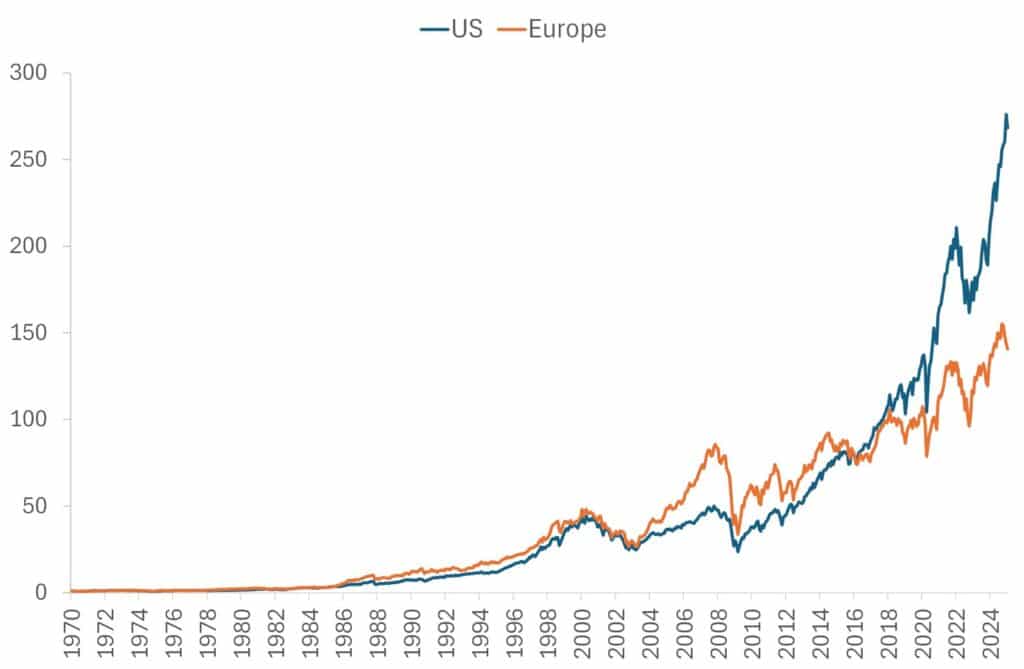

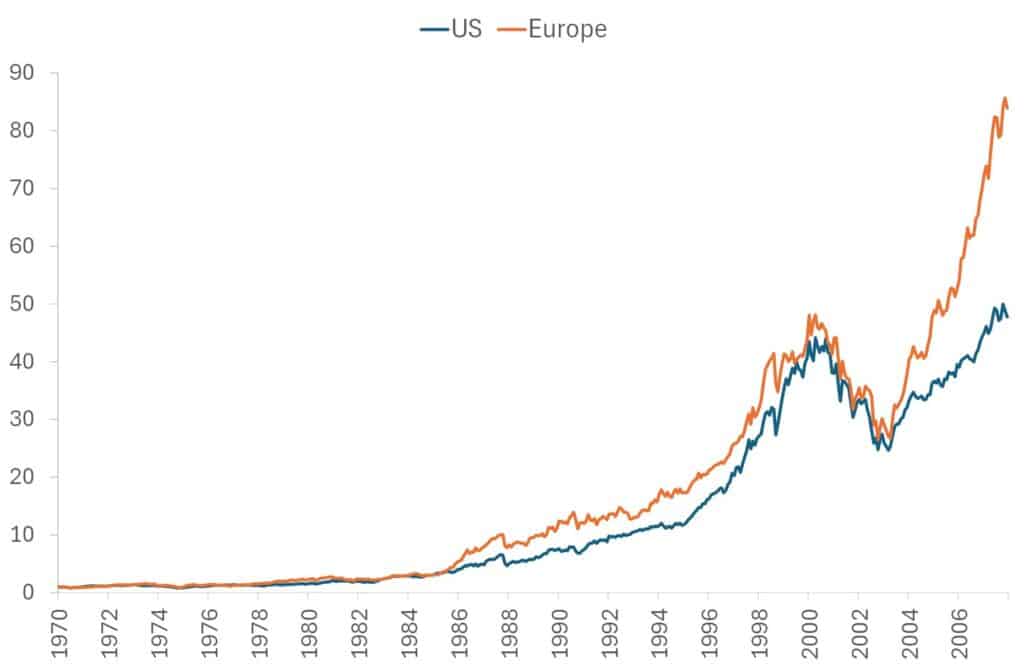

Figure 1 illustrates how one dollar invested in the US stock market in 1970 would have grown if the investment had been maintained and all dividends were continuously reinvested, i.e., the figure tracks the development in the total return index for MSCI US. The figure compares this to the cumulative return performance of the European market, represented by MSCI Europe.

Figure 1 demonstrates that one dollar invested in the US stock market index in 1970 would have grown to USD 268 by 2025. This is an impressive return.

Over the long term—55 years, 1970-2025—the US stock market has outperformed the European: The figure shows that if you had invested one dollar in the European stock market, it would have grown to only half as much as the US stock market—USD 141.

Digging deeper

US outperformance has not been the historical norm, however. In fact, up until 2015, European stocks generally led the way. Although their outperformance may not have been dramatic on a year-by-year basis, the cumulative effect over time is significant. For instance, by late 2014, a one-dollar investment made in 1970 would have grown to USD 85 in Europe, compared to “only” USD 78 in the US.

This trend is even more striking for the period up to 2007. By that year, a one-dollar investment made in 1970 would have grown to USD 84 in Europe, compared to just USD 48 in the US—only half the return of European stocks.

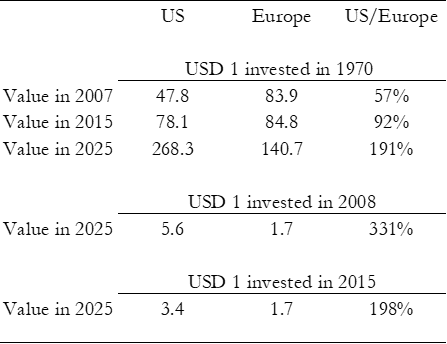

To make these figures easier to interpret, I have summarised them in Table 1. The table also includes the percentage under- or outperformance of US stocks relative to European stocks over the different periods. For example, a one-dollar investment in the US in 1970 would have grown to USD 47.8 by 2007, while the same investment in Europe would have reached USD 83.9. This means that the gain from a US investment would have been just 57% of the gain from a European investment.

The key point of this analysis is that it is risky to assume, “This stock market has dominated historically, so it will continue to do so.” I write the analysis because such statements are common today, with many expecting the strong US dominance to persist because it has done so recently. It might—but before jumping to conclusions, let’s at least evaluate such assumptions.

As an example: By 2007, Europe had significantly outperformed the US. However, had you concluded in 2007 that Europe’s remarkable performance was bound to continue, you would have made a poor investment decision. For instance, investing one dollar in the US in January 2008 would have grown to USD 5.6 by today, as also shown in Table 1. In contrast, the same investment in Europe would have grown to just USD 1.7, meaning the US outperformed Europe by an astonishing 331% over this period.

The same pattern applies to the post-2015 period, as also highlighted in Table 1.

Annual returns

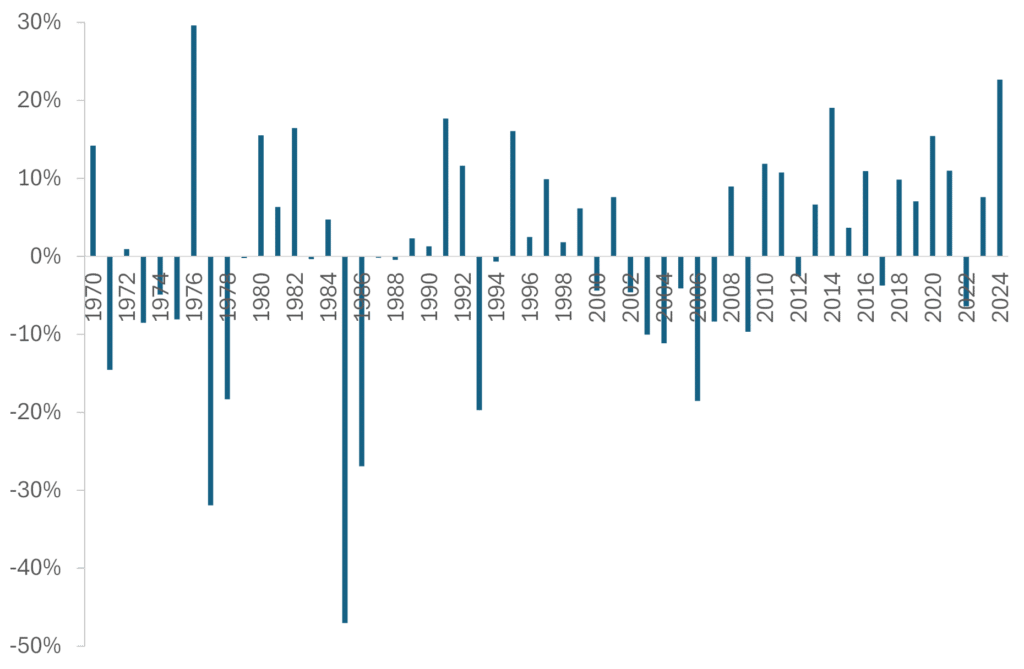

While Figure 1 and Table 1 focus on cumulative returns over extended periods, analysing annual returns offers a more detailed perspective. Figure 2 illustrates the annual outperformance (or underperformance) of the US stock market compared to the European market.

The US stock market outperformed the European market by 23 percentage points (25% vs 2%) in 2024. As you see from Figure 2, this was the second-largest annual outperformance on record, surpassed only by the 30-percentage-point gap in 1976, when the US market surged by 23.2% while the European market declined by 6.4%. In other words, the 2024 outperformance was exceptionally high and an infrequent occurrence. Do not expect such outperformance to be the new normal.

Conversely, there have been periods of strong European outperformance. For example, in 1985, both markets delivered spectacular returns, but Europe outshone the US, soaring by an incredible 80% compared to the US market’s 30% gain. This was followed by another strong year in Europe in 1986, with the European market rising by 44%, compared to 18% in the US.

Before and after the financial crisis of 2008

The figures and table collectively illustrate that US outperformance is largely a post-financial crisis phenomenon.

Prior to the financial crisis—over the 38 years from 1970 to 2007—the US market underperformed Europe in 21 years and outperformed in 17 years, a nearly even split. However, since 2008, this trend has shifted dramatically: the US has outperformed Europe in 13 of the 17 years.

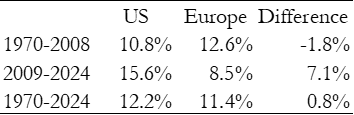

Across the entire 1970–2025 period, the average annual return for the US market was 12.2%, compared to 11.4% for Europe—a relatively modest difference. Yet, this overall figure conceals a significant divergence between the pre- and post-financial crisis periods, as illustrated in Table 2.

Before 2008, the US delivered an annual return that was 1.8 percentage points lower than Europe. Since 2008, the US has significantly outperformed Europe, with a 7.1 percentage-point annual advantage.

What now?

Some of you might be thinking: “Comparing with 2008 doesn’t really make sense. The strong European performance leading up to the financial crisis was clearly unsustainable—European outperformance before the 2007 financial crisis was essentially a bubble.” Fair enough, you could be right. But take a look at Figure 3. It presents the same data as Figure 1—showing how one dollar invested in either Europe or the US would have grown—but now with the timeline ending in 2008.

To me, Figure 3 looks strikingly similar to Figure 1. Up until 2003, the two markets delivered almost equal performance, followed by a period of strong outperformance—at that time, by Europe. In 2025 (as shown in Figure 1), we see a similar pattern: nearly equal performance up to 2015, followed by a strong outperformance, but this time by the US.

This US dominance might continue, fuelled by high expectations for the future of AI and subdued growth prospects in Europe. It is also true that the recent US outperformance has been more consistent, lasting now almost ten years, since 2015 at least, while European outperformance lasted only three to four years before the financial crisis. Alternatively, US dominance might not continue, if investors come to believe that the very few—but very successful—stocks driving the US stock market (link) will fail to meet these lofty expectations.

One thing we can say with certainty is that buying US stocks today means paying a premium for their underlying performance. Table 3 compares various valuation metrics for the two markets.

The price you pay for one dollar of earnings (P/E) in the US is twice as high as in Europe. For one dollar of expected future earnings (P/E forward), the US market is priced at 1.7 times higher, and for one dollar of book value, it is more than twice as high—2.6 times, to be exact.

Research has shown that, over the long run, valuation prevails—investing in assets with low valuation typically delivers higher returns over time (link). That said, of course, there’s always the possibility that this time might be different. Also, it is important to remember that valuations work over the long run, that is over the next five or ten years. High (or low) valuations say little about next year’s return.

Conclusion

For yet another year, the US stock market has outperformed European stocks. In 2024, US stocks rose by 25%, compared to the nearly flat performance of European stocks, which gained just 2%. This continues the trend from the previous year, where US stocks also outpaced their European counterparts.

However, such clear US outperformance is not the historical norm. Before the financial crisis, European stocks delivered superior returns, particularly in the years leading up to the crisis.

What should we expect next? Who knows? The US may continue to power ahead, or stock prices could revert, bringing US valuations more in line with historical norms. Only time will tell. The main point of this analysis is that one should be cautious when using historical trends to predict the future.

As for what I’m doing, I’ll keep that to myself.

This post originally appeared on Rangvid’s Blog.