By David van Bragt and Daniel Torres – Aegon Asset Management: Alternative fixed income assets have become increasingly important for institutional investors. They provide opportunities to increase the overall portfolio yield when the (often lower) liquidity of these assets is less of a constraint. This is typically the case for long-term investors, such as pension funds or life insurance companies.

Summary

- The alternative fixed income asset class is highly diverse, embracing many asset classes such as private debt, consumer loans, mortgage investments, insured loans, loans to small and medium-sized enterprises (SMEs), infrastructure debt and asset-backed securitizations. These assets can offer enhanced yields compared to government and corporate bonds, along with relatively low correlations to traditional assets.

- An alternative fixed income allocation can offer investors exposure to a wide variety of return drivers, many of which also have an environmental, social and governance (ESG) focus.

- Alternative fixed income is particularly attractive for long-term investors, including pension funds and life insurance companies.

- An interesting feature of many alternative fixed income assets are the additional safety measures compared to traditional corporate loans, such as covenants and guarantees.

- Alternative fixed income strategies exhibit great variety in terms of spread, risk, capital charge, liquidity, duration matching and ESG opportunities. This enables investors to choose those assets which best fit their particular investment needs, by taking the different characteristics of these assets into account.

Introduction

The alternative fixed income universe is rapidly expanding and has now branched into different directions. Some examples are given below.

| Consumer exposure | Many investors have a large exposure to sovereign and corporate risk. Alternative fixed income assets can offer exposure to consumer risk, for example through investments in residential mortgage loans or securitizations backed by credit card loans, auto loans or student loans. This helps diversify their portfolios. |

| Sustainable financing | A huge capital flow is required to transform the current society into a more sustainable one. Impact investing in infrastructure is already a major trend. Opportunities in water, water treatment, communications and mobility are also available. |

| Real estate & infrastructure debt | Property and infrastructure investments are a long-term, stable asset class, with the potential for an ESG and/or impact investment focus. Investors who need their private debt investments to contribute to long-term liability hedges can also find real estate debt or infrastructure markets very attractive. |

| Insured credit | Further diversification can be found in insured credit. These are loans with additional credit protection by a highly-rated insurance company. This strategy can be especially appealing for insurers due to its attractive return on capital under Solvency II. |

An alternative fixed income allocation can provide strong diversification benefits, with exposure to a variety of return drivers, often with a focus on ESG factors. Given the illiquid nature of most alternative fixed income categories, the practical allocation between sectors will not be particularly dynamic. However, the high income produced by many of these categories means there is a potential to reallocate income streams to new opportunities or increase allocations to favoured sectors. Regional diversification is also important, although there may be a preference for certain regions in some sectors, given the relative size of the markets and the expertise required for investing successfully in different parts of the market.

A high demand for impact investing – but still a limited supply of deals that conform to the strictest ESG definitions – makes building a diversified portfolio less easy, or at least a more time-consuming process. We believe, however, that the various existing opportunities and ongoing development of the alternative fixed income market make it a good choice for supporting long-term sustainable investing objectives.

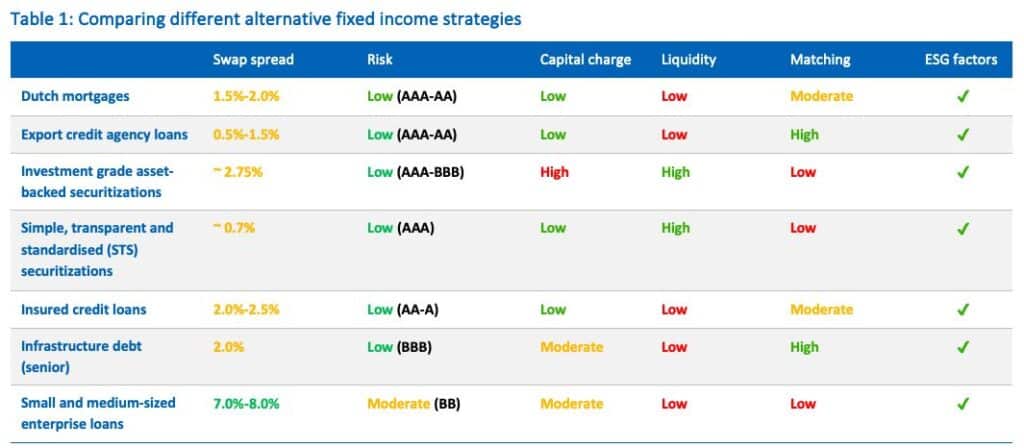

In table 1 we compare different categories within the alternative fixed income spectrum. It is important to note, however, that the scores on the different dimensions can (and will) shift over time and that the assessment is sometimes based on qualitive instead of quantitative measures (the ESG assessment being an example). Capital charges are determined with the standard formula of the Solvency II regulations.

ESG Considerations

Alternative fixed income strategies are well-suited for sustainable investing. They often finance projects that do not have easy access to capital markets and would otherwise receive less financing. Furthermore, many ESG solutions are driven by smaller, innovative, privately-owned companies, which are commonly involved in direct lending transactions.

Investors can be selective and specific when it comes to ESG. Investors, individually or in small groups, can negotiate terms to stipulate adequate reporting on ESG, or set interest rates contingent on general ESG performance or specific ESG factors. They can also have more direct controls and ways to engage with borrowers.

Integrating ESG is part of our investment process for each category of alternative fixed income. This is different for each strategy and opportunities for responsible, sustainable and impact investing can be found.

Conclusions

In recent years alternative fixed income assets such as mortgage loans, infrastructure financing and private debt have become much more important categories for institutional investors. They can provide opportunities to increase portfolio yield when the (often lower) liquidity of these assets is not a constraint. This is typically the case for long-term investors, such as pension funds and life insurance companies.

Many insurance investors will already be aware of the benefits of Dutch mortgages, which can provide an attractive return on capital. Other types of alternative fixed income can add diversification alongside mortgages, but also alongside public market investments. Higher yields are possible (even with well-collateralized senior loans), particularly in private corporate debt markets. An interesting feature of these categories is that greater safety measures can exist compared to traditional corporate loans, for example in the form of additional covenants or guarantees.

Alternative fixed income strategies demonstrate great variety, both in terms of spread, risk, capital charge, liquidity, duration matching and ESG factors. Investors have an opportunity to select those assets which best fit their particular investment needs, by taking the different characteristics of these assets into account.

Disclosures

For Professional Investors only and not to be distributed to or relied upon by retail clients.

All investments contain risk and may lose value. Responsible investing is qualitative and subjective by nature, and there is no guarantee that the criteria utilized, or judgement exercised, by any company of Aegon Asset Management will reflect the beliefs or values of any one particular investor. Responsible investing norms differ by region. There is no assurance that the responsible investing strategy and techniques employed will be successful. Investors should consult their investment professional prior to making an investment decision.

Aegon Asset Management UK plc is authorized and regulated by the Financial Conduct Authority. Aegon Investment Management B.V. (Chamber of Commerce number: 27075825) is registered with the Netherlands Authority for the Financial Markets as a licensed fund management company. On the basis of its fund management license Aegon Investment Management B.V. is also authorized to provide individual portfolio management and advisory services.

Adtrax: 6010295.1 Exp. Date: 01/10/24