By Mike Going, Mike Marcey, and Marat Molyboga, Efficient Capital – Inflation has been at the forefront of the agendas of investors and central banks worldwide this year. The current CPI Index, at 8.4% in July 2022, is as high as it has been in four decades. As a result, investors are scrambling to protect their portfolios and are looking for solutions beyond the common 60/40 approach. But history and intuition suggest the difficulty of knowing the duration and intensity of inflation, raising the question of whether to implement a strategy designed for an inflationary regime, only to have inflation end and the strategy become obsolete or ineffective.

In this short article, we want to do three things:

- Highlight an approach that has historically performed well in inflationary regimes,[1]

- Demonstrate that this approach does well after inflationary regimes have ended, removing the problem of market timing,

- Discuss specific ways to implement this approach

1. What has done well in inflationary regimes?

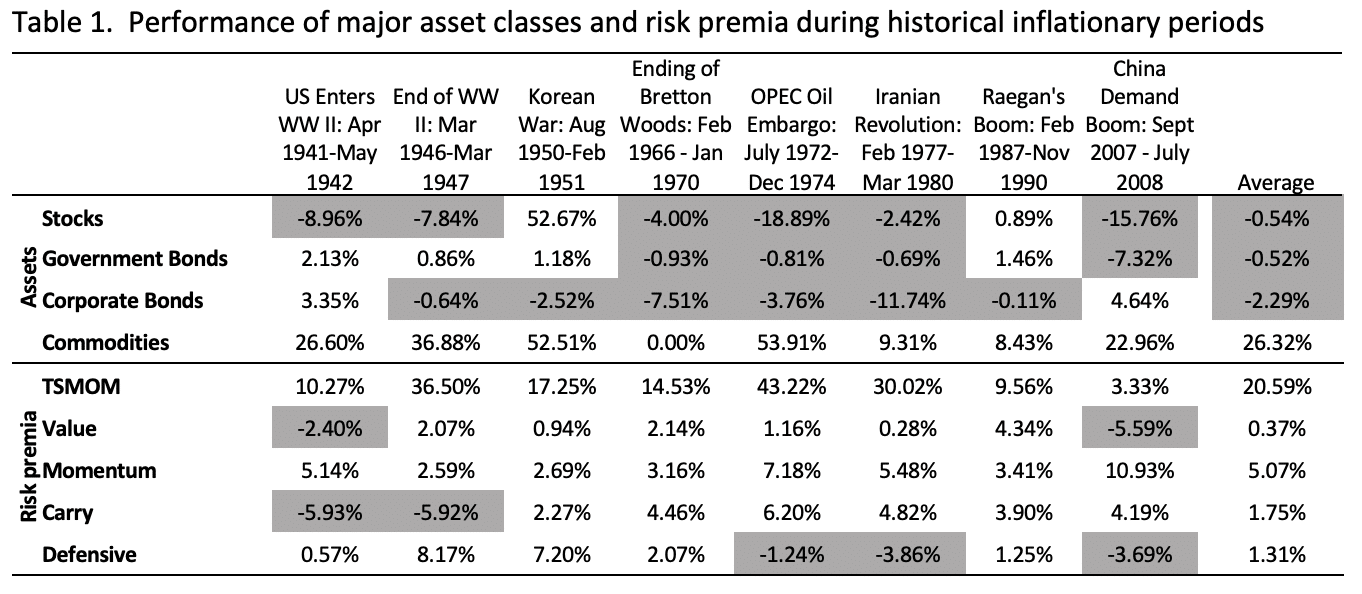

Table 1 summarizes the performance of stocks, bonds, commodities, and risk premia strategies across eight inflationary regimes since 1940.[2] Note that a portfolio of stocks and bonds experienced material losses in all but two inflationary regimes. By contrast, commodities and time-series and cross-sectional momentum strategies were profitable across all inflationary regimes.

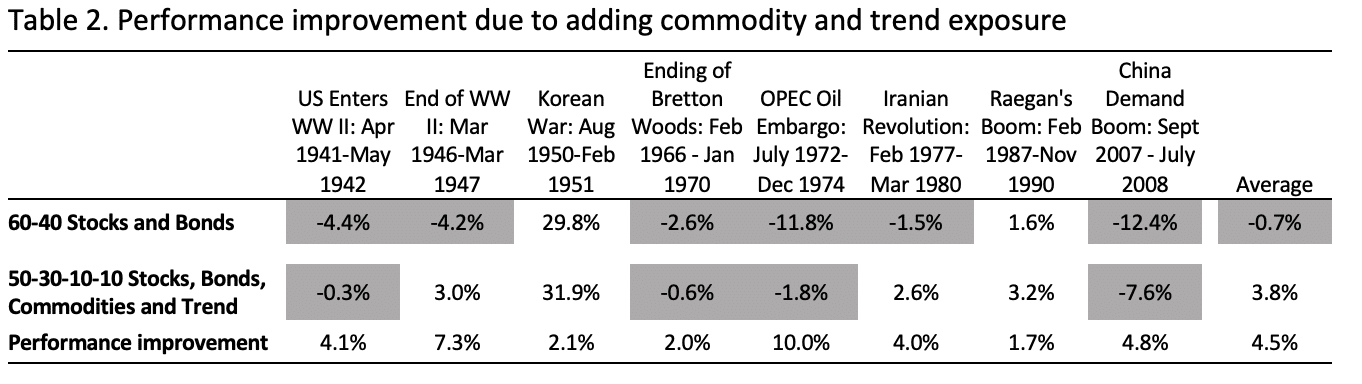

Based on these historical results, a 60/40 blend of stocks and bonds is now used as a proxy for the portfolio of an institutional investor. Trend and commodity exposures are added in equal parts to create a portfolio (Inflation Risk Offset) with a 50/30/10/10 blend of stocks, bonds, trend, and commodities, respectively, and rebalanced monthly. As shown in Table 2, allocating to trend and commodities strategies at 10% each improves the performance of the 60/40 portfolio in each of the inflationary regimes and has an average performance increase of 4.49 percentage points.

2. How does this approach do when inflationary regimes have ended?

It is well known that timing environments is challenging. Even if the IRO has strong performance during inflationary regimes, there is a risk of mistiming the investment and experiencing losses if a post-inflationary environment is unfavorable for the portfolio. Therefore, we now want to examine the performance of this approach for three years after each inflationary regime.

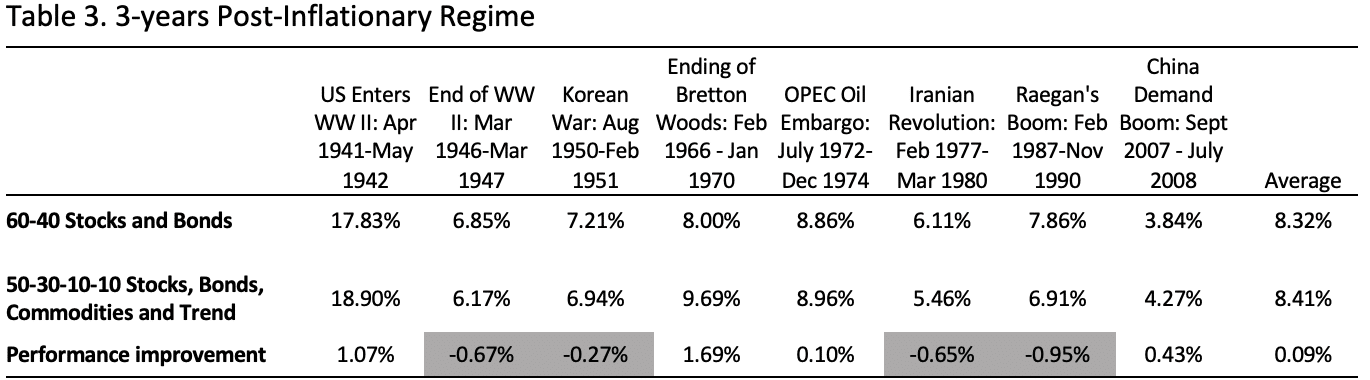

Table 3 shows that the IRO portfolio protects against inflationary periods while delivering modest performance improvements over the three years immediately after the inflationary regime ends. With an equal allocation of 10% to both trend and commodities, performance improved by nine basis points during the post-inflationary period. These results represent a peculiar case in which an investor gets paid handsomely to own a portfolio during inflationary environments but also receives a small payment to own that portfolio in non-inflationary environments. Therefore, the risk of mistiming the Inflation Risk Offset portfolio is relatively low.

3. Implementation considerations

Our analysis shows striking theoretical benefits of the Inflation Risk Offset solution. Moreover, investors have a variety of ways to actually implement this approach, depending on their specific objectives and constraints. For instance, multiple cost-effective, well-diversified commodity indices are readily available to investors. Two of the most popular indices are the Dow Jones Commodity Index, (which includes 28 commodity futures contracts and is equally weighted across the three sub-sectors of energies, metals, and agricultures/livestock and liquidity-weighted within the sub-sectors) and the S&P Goldman Sachs Commodity Index.

In addition, one can access the trend-following component in either a passive way (through something like the Mount Lucas Management Index) or by investing directly in trend-following managers. Because of the high return dispersion that exists even among highly correlated trend managers (up to 40 or 50 percentage points per annum with relatively low return persistence), a multi-manager approach may be an attractive option.[3] Investing in five or six trend-following managers improves the Sharpe ratio by roughly thirty percent and poses less idiosyncratic risk.

We believe that institutional investors should consider two potential solutions. Those investors who are very cost-sensitive, and have a strong preference for passive investing, may want to consider a portfolio that includes the Dow Jones Commodity Index and the MLM index. Others may want to consider a portfolio that includes the Dow Jones Commodity Index and an actively managed portfolio of five or six trend-following managers. Both solutions require little funding due to their cash efficiency and can be structured as an overlay on top of the equity and bond exposures.

Concluding remarks

Whether inflation is transitory or not, we have illustrated the value of adding commodity and trend following to traditional portfolios. In addition, because the IRO portfolios have historically done well in periods after inflation has ended, the need to correctly predict the duration of inflation is mitigated. Rather than having a cost associated with it, the proposed inflation protection portfolio actually pays an investor to own the inflation risk offset. Finally, there are multiple ways that an investor can implement a simple Inflation Risk Offset solution.

[1] We use the eight inflationary periods defined in Neville, H., Draaisma, T., Funnell, B., Harvey, C.R., and O. Van Hemert (2021) “The best strategies for inflationary times.”

[2] We rely on the time series of excess returns from the AQR data library.

[3] See Marcey and Molyboga “Commentary: the value of diversification in CTA investments”, Pensions and Investments, April 13, 2020.

Picture: By Casper1774 Studio—shutterstock.com