By Payal Shah, Director, Equity Research and Product Development – CME Group: The COP26 climate conference was dubbed the ‘investment COP.’ Participants weighted their expectation on the global financial community and governments to mobilize finance flows at scale for climate mitigation. At the other end of the spectrum, sustainable investing also moved into the mainstream, despite – or perhaps because of – the COVID-19 crisis, as both institutional and retail investors recognize ESG investing’s potential to provide superior returns and mitigate risk.

Rapid Growth of ESG Derivatives

As sustainable investments grow, so too does the need for risk management solutions that are specifically tailored to ESG criteria. Specialized ESG versions of existing, highly successful and highly liquid benchmarks are market preferred.

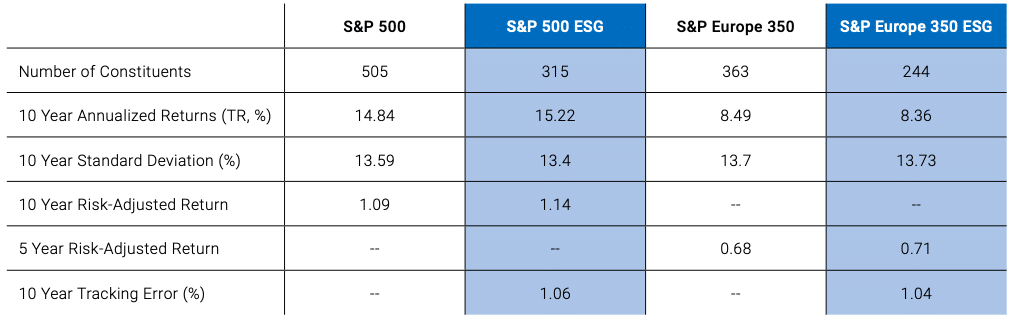

The S&P 500 index is perhaps the world’s most widely quoted index. Its ESG version – the S&P 500 ESG index – has a 5-year tracking error against the S&P 500 index of just 1.06%. As a result, the S&P 500 ESG index has emerged as a leading candidate to provide a general benchmark for the ESG investment sector that is backed by a deep, liquid futures market.

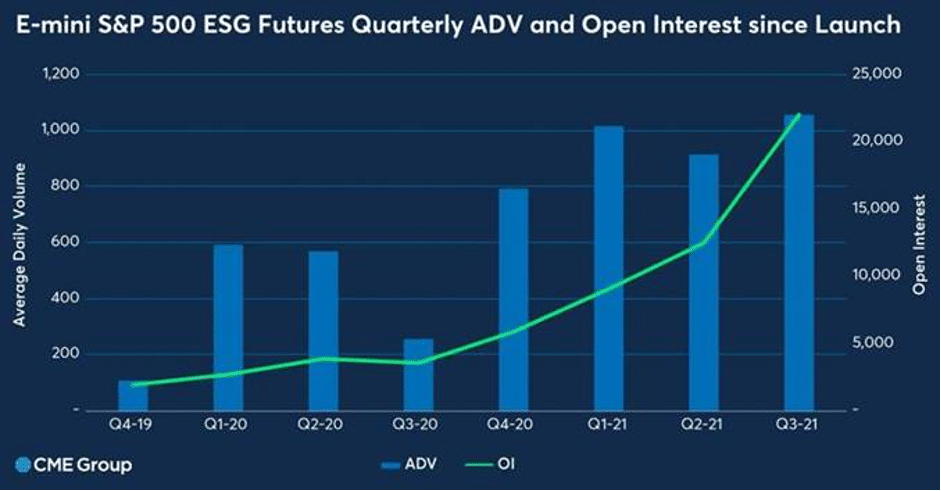

The E-mini S&P 500 ESG future reached its 2-year anniversary, establishing itself as the most liquid ESG equity index futures on the globe. The chart shows the accelerating Average Daily Volume (ADV) and Open Interest (OI) of the contract. Given liquidity begets liquidity, this pattern could continue into 2022. ADV for 2021 is 1,000 contracts per day and OI is currently over 14k contracts ($3bn notional) and reached a record of over 22k in the Sep expiry week.

Managing ESG Risks

The use of derivatives allows firms to manage specific risks related to ESG factors. They allow funds to meet target allocation in a more cash efficient way than investing directly in the underlying stocks – potentially enabling more capital to be channelled towards sustainable investments.

Futures on indices, such as the S&P 500 ESG or S&P Europe 350 ESG, provide a ready means for ESG investments. Both indices are Article 8 compliant which adheres to the recent EU taxonomy regulations. The European Green Deal and increased emphasis on ESG initiatives and the new U.S. administration will increasingly incentivise financial participants to meet their ESG targets.

ESG Index Methodology Matters

Both the S&P 500 ESG Index and the S&P Europe 350 ESG Index are based on an exclusion methodology that allows investors to eliminate certain types of exposures, while retaining similar risk-return characteristics to the parent benchmark. The ESG version excludes: Controversial Weapons, Tobacco, Thermal Coal (> 5% of revenue), Low UNGC Score and importantly also excludes the lowest 25% of S&P DJI ESG scoring companies in each GICS Industry Group.

Liquidity

Tight bid-ask spreads seen in both the US and EMEA morning hours are indicative of the fact liquidity is available. It is also worth noting that there is a strong arbitrage channel between the parent E-mini S&P 500 futures and the ESG version. The bid-ask spread during US hours when the underlying stocks are open is extremely liquid with a bid-ask of circa 2 basis points. The top of book size is on average 10 contracts ($2mn notional).

The EMEA bid-ask is 5 basis points wide outside of US hours. Investors are taking advantage of this out of hours liquidity as seen by the fact 20% of all trades in E-mini S&P 500 ESG are occurring before the US cash market opens.

Importantly during the recent roll activities, some clients performed an inter-product switch – out of the E-mini S&P 500 and into the E-mini S&P 500 ESG futures contract. High correlation with other ESG based indices (typically 99.5%+) has meant clients benchmarked to those indices are likely adopting this product for liquidity characteristics.

2022 Outlook

Developments in ESG are happening at speed. New regulations, such as the sustainable finance disclosure regulation (SFDR) and the EU Taxonomies are creating demand for more products.

The ongoing growth in ESG equity index futures will be crucial in facilitating the development of liquidity pools and will make risk management straightforward and economic.