By RPM Risk & Portfolio Management: Following a year of low Time Series Momentum (TSMOM) and relatively weak performance, in 2024, CTAs generated positive returns as trendiness soared above long‑term average levels on the back of record‑breaking trends in softs and stocks, especially during the first quarter of the year.

The CTA universe is dominated by diversified systematic trend following managers exploiting Time Series Momentum (TSMOM). In other words, most CTAs are trend followers generating profits in a trending market environment, i.e., when asset prices move substantially and sustainably in several different markets at the same time.

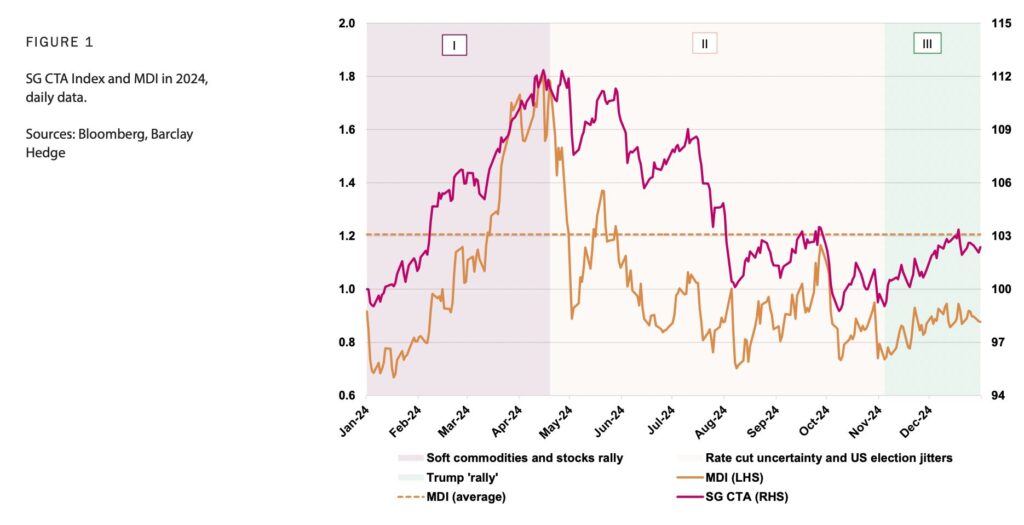

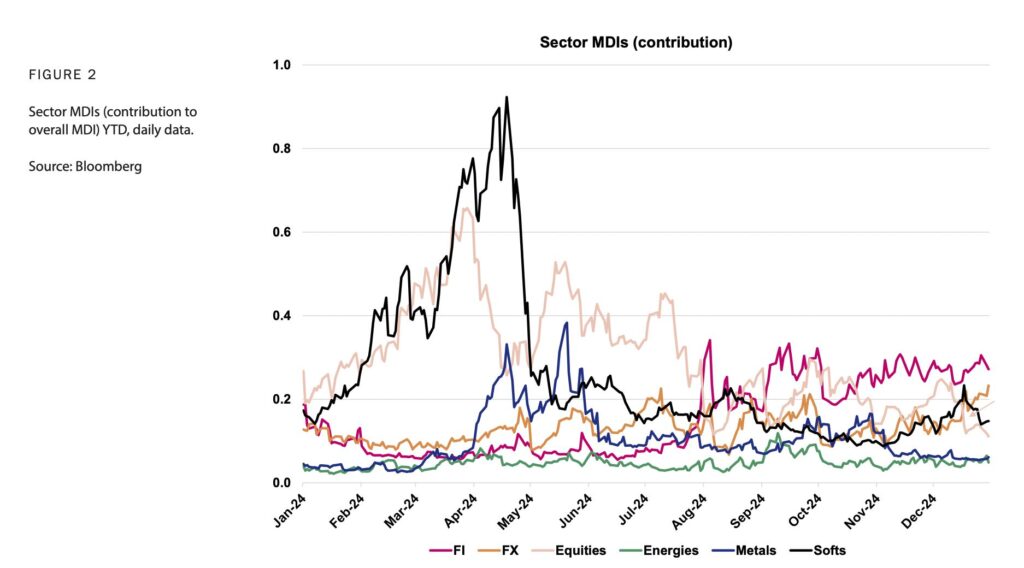

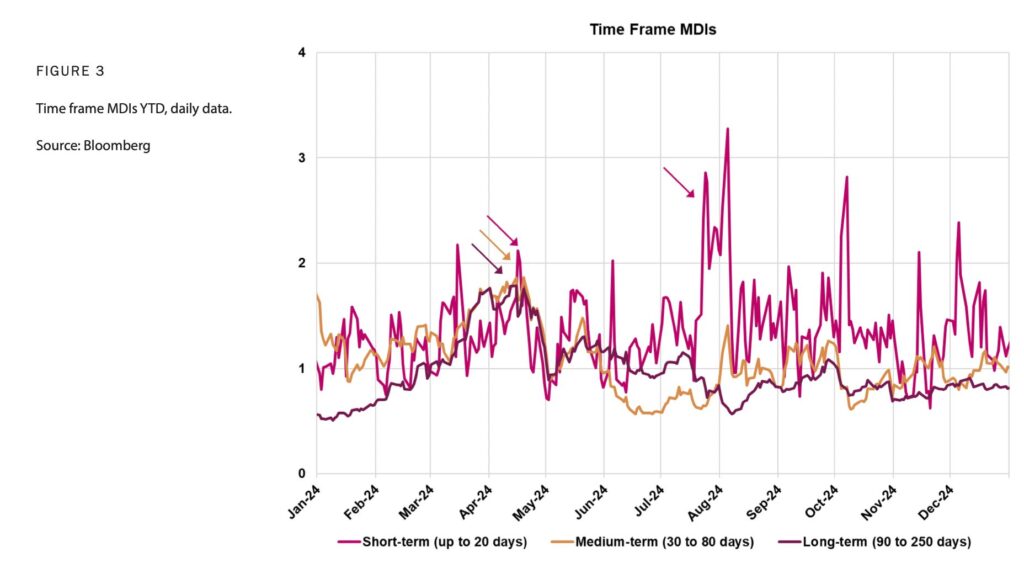

Figure 1 shows RPM’s measure of TSMOM, i.e., the Market Divergence Indicator (MDI), its 32-year average level, and the SG CTA Index in 2024.1 Figure 2 shows MDI contributions broken into sectors, i.e., fixed income, currencies, equities, energies, metals, and soft commodities. In Figure 3 MDIs are calculated over different look-back periods, i.e., short-, medium-, and long-term.

Following a year of low MDI readings and negative performance, in 2024, CTAs generated positive returns as trendiness soared above long-term average levels on the back of strong trends in equities and soft commodities in the first quarter of the year. The remainder of the year was characterized by below average levels of trendiness amid rate cut uncertainty and US election jitters. Trump’s election victory only slightly improved TSMOM towards year-end.

In more detail, from a CTA perspective, the year can be divided into three subperiods (see Figure 1):

I. In 2024Q1, CTAs generated strong gains primarily from long positions in stock indices and soft commodities as TSMOM rose to above-average levels across many different time frames (see Figure 3). US equities rallied to new records amid hopes for a soft landing, expectations of upcoming rate cuts, and an unprecedented AI-hype. Cocoa also soared to new highs due to unfavorable weather conditions in West Africa which made the MDI in soft commodities the main contributor to overall trendiness in the first quarter (see Figure 2).

II. Between late Apr- and Oct-24, TSMOM decreased unevenly amid several major reversals and rebounds across financial markets due to uncertainty with regards to when the Federal Reserve would start cutting rates and the course of the US presidential race.2 Stocks and bonds sold off as the Fed did not deliver the already priced-in pre-summer rate cut due to uncomfortably high inflation figures and stronger-than- expected economic data. Then, cocoa prices reversed sharplyamid liquidity drying up. During the summer, the Bank of Japan intervened several times in the currency market, ultimately triggering a global market rout and a major volatility spike in early August. In 2024H2, markets changed direction many times, which favored short-term managers over medium- and long-term strategies as can be seen in Figure 3.

III. In Nov-24, TSMOM began to increase again after Trump had clinched victory in the US election. The US dollar rallied, and US stocks surged to new highs whereas cocoa and coffee prices also hit all-time high levels on renewed supply worries.

However, the stock rally was cut short when the Fed triggered an equity rout as it scaled back the number of expected interest rate cuts in 2025 (see Figure 2, arrow).

Soft Commodities: Hot Chocolate and Coffee Craze

Throughout the year, cocoa and coffee prices rallied, making soft commodities the most profitable sector for CTAs in 2024 (see Figure 4). With regards to cocoa, prices soared to new record highs during the first quarter of the year due to dry weather conditions impacting harvests in West Africa.

However, in 2024Q2, cocoa prices slumped by more than 20% as higher margin calls sparked long liquidations causing market liquidity to dry up. With regards to coffee, prices rose continuously throughout the year reaching multi-decade highs as concerns over global supply shortages added to market uncertainty over the impact of incoming EU legislation on deforestation. Towards year-end, both cocoa and coffee hit all-time high levels on revived global supply worries.

US Stocks 2024: AI, FED, BOJ and Trump

In 2024, US stocks had another record-breaking year propelled by hopes for an AI-driven economic boom, a soft landing of the US economy, continued interest rate cuts, and hopes for significant tax cuts after Trump’s election victory, raising calls for American exceptionalism and making equities the second most profitable sector for CTAs last year.

However, the journey was not a smooth one with the rally being interrupted by several painful (intramonth) reversals throughout the year (see Figure 5):

In Apr-24, stocks sold off as investors dropped expectations of a pre-summer rate cut by the Fed amid stubbornly high inflation. Geopolitical tensions amid Israeli airstrikes on Iran also rattled investors.

In Jul-24, equities retreated due to missed earning targets in the tech sector. A global technology outage shutting down airports and disrupting businesses around the world added to the stock market woes.

Aug-24 was a decisive month regarding CTAs’ overall performance 2024. Stocks slumped and the VIX soared to levels not seen since the early stages of the 2020 pandemic as US recession fears and a hawkish BoJ turned existing market perceptions on its head. The rise in the Japanese yen caused a dramatic unwinding of the yen carry trade seeing Japan’s main stock index suffer its worst selloff in 37 years dragging global indices down with it. Whereas global equities recovered until month-end, CTAs ended the month in negative territory, but faster system were able to profit from the rebound and generated significantly better performance than slower managers, a lead that was kept until year-end (see Figure 6).

In Sep-24, US stocks slumped on renewed recession fears before rallying to new highs after the Fed had delivered a jumbo half-point rate cut. At the end of Oct-24, a tech-lead sell-off wiped out all of October’s gains.

In Nov-24, US stocks first surged to new highs in a frenzied rally sparked by Trump’s sweeping election victory before sounding the retreat as investors shifted focus towards expected tariffs and their implications for world trade.

In Dec-24, US stocks rose to new record highs before the Fed triggered an-other rout when it scaled back the number of expected rate cuts in 2025.

Energies: Range-Bound Markets Par Excellence

Last year, concerns about the health of the Chinese economy and its impact on global demand kept a lid on crude oil prices for much of 2024 despite a market in deficit and countering spikes from geopolitical tension in the Middle East and Eastern Europe. Numerous extensions by OPEC+ of its voluntary output cuts also contributed to price stability.

This generated a difficult trading environment for managers as prices were largely range-bound for most of the year making energies the worst performing sector for CTAs in 2024, by far.

Market Summary Quarter by Quarter

In 2024Q1, CTAs generated strong returns on the back of record-breaking rallies in US equities and soft commodities amid receding recession fears and AI-enthusiasm in the US and unfavorable weather conditions in West Africa respectively.

In Q2, CTA performance reversed due to losses in soft commodities, energies, fixed income, and equities. In financials, stocks and bonds sold off as the expected pre-summer rate cuts in the US did not materialize amid persistently high inflation and strong data. In commodities, oil prices remained in a tight range whereas cocoa prices reversed sharply amid drying up liquidity.

The third quarter was the worst quarter for CTA benchmarks last year. In Aug-24, the VIX soared to levels not seen since the pandemic amid a market rout as US recession fears and a hawkish BoJ shocked investors causing a dramatic unwinding of the yen carry trade. However, short-term managers were able to quickly profit from the ensuing market rebound, thus limiting losses notably compared to their larger (and slower) peers.

In the fourth quarter, CTA benchmarks were largely flat as profits made during the Trump rally were not enough to outweigh losses made in Oct-24.