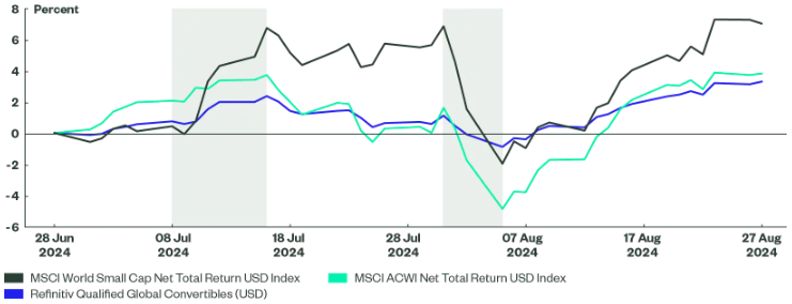

By Antoine Lesne, Head of ETF Strategy at SPDR: The Refinitiv Qualified Global Convertible Index returned 5.61% year to date as of 27 August 2024. While far from the performance of global large-cap equity markets, its performance has been closer to that of the global small cap equity index and it has outperformed many fixed income exposures thus far this year. As a mix of both fixed income and equities traits, the convertibles index is delivering what is expected of it.

Why Invest in Convertible Bonds? Built for Many Scenarios

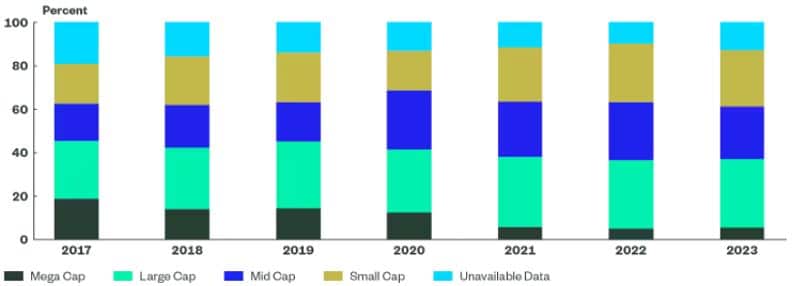

Should investors expect a goldilocks scenario of steady growth and lower inflation, duration could be a driver of performance, but less so spread compression given the already tight spreads observed in the high yield space. The majority of the underlying companies in the global convertible bonds index remain at valuations significantly lower than their highs. This means that convertible bonds would not only benefit from the duration moves, owing to lower rates (albeit less so than straight corporate bonds), but also from the impact this has on underlying company valuations. Thus, convertibles should also stand to benefit from equity participation. Convertible bonds are highly exposed to mid-cap and/or growth companies (Figure 2) which are likely to benefit from lower interest rates, something we saw during the July rally following the lower-than-expected inflation print for June (Figure 1).

Figure 1: Performance of Global Equity and Convertible Bond Indices Quarter to Date

Up With Small Caps, Down With Volatility Spikes: A Live Example Scenario

A hard landing scenario could be created by stubborn inflation forcing central banks to stay on hold — or even hike rates further — thus leading to a credit spread widening. In this case, convertible bonds will offer a more interesting profile than high yield and less equity sensitivity than a pure large-cap equity portfolio, given the relatively low valuation of the small- and mid-cap part of the portfolio (circa 60% as of end June 2024). Moreover, convertible bonds are a long volatility play and should benefit from a rise in volatility in a hard landing scenario. The low interest rate sensitivity (with a duration of around 2.7) compared with both global high yield and investment-grade indices provides some relative protection. Figure 1 also highlights the downside protection of convertible bonds relative to equities during the early August rapid sell-off following the JPY carry trade unwind and volatility spike.

The more likely soft landing scenario of gradual rate cuts should benefit small- and mid-cap companies given their recent underperformance relative to mega-cap companies. This is due to the impact of higher rates on their financing needs in particular, relative to large-cap blue chip names. We are now close to entering a more broad-based loosening interest rate cycle among developed markets. After the European Central Bank became the first G4 central bank to cut rates in June, the Federal Reserve is now expected to cut at the meeting on 18 September. Therefore the point at which investors will consider companies with a potential benefit from a steeper yield curve is getting closer, potentially leading to further stock market gains towards year end and into 2025.

Figure 2: Refinitiv Qualified Global Convertible Index Market Capitalisation Profile Evolution

It is also worth noting that issuers are returning to the market in 2024 with over $70B year to date[1]. Convertible bonds are generally attractive for diversification given their different and sometimes unique sector profile versus traditional equity and bond indices. This is especially clear as the primary market is currently very dynamic (with $18+B in issuances in May, $13B in June, and $8+B in July), with diverse issuers coming to the market helping increase the average coupon of the universe. We could witness some jumbo issuance across the market this year, a prime example being Alibaba making a surprising comeback with a $5B bond in May. Interestingly, there has not been any notable average quality deterioration that would be linked to cash-strapped companies turning to this market for financing. Most names are crossover-grade companies (between investment grade and high yield) funding growth development rather than deep junk companies looking for a lifeline.

Is the Increase in Default Rates and an Economic Slowdown a Concern?

The risk of default is indeed real given the deteriorating economic outlook. However, indexed investments can offer some real benefits. Indeed, we believe that portfolio diversification helps to limit idiosyncratic risk. In the Refinitiv Qualified Global Convertible Index, the weight of an issuer cannot exceed 4% and the top 10 issuers represent less than 14% together. In total, there are more than 345 convertible bonds.

Convertible Bonds in the Current Market

With higher coupon levels, a historically “normalised” rate environment, and a potential pick-up in volatility, balanced convertible investors are being paid to wait and are likely to benefit from pivotal thematic equity exposures such as artificial intelligence, healthcare and energy in the longer run, and simply from a rate pivot in the shorter term.

Why SPDR® ETFs for Convertible Bonds

State Street Global Advisors has strong expertise in index management for the complex asset class of convertible bonds, with close to $4.8B managed in two ETFs. In UCITS ETFs we offer several currency-hedged share classes of our global convertible bond ETF — in EUR, GBP, CHF and USD — facilitating the switching between them. You can learn more about convertible bond funds here, or see fund details below.

How to Access the Theme

SPDR® Refinitiv Global Convertible Bond UCITS ETF (Dist)

SPDR® Refinitiv Global Convertible Bond EUR Hdg UCITS ETF (Acc)

SPDR® Refinitiv Global Convertible Bond USD Hdg UCITS ETF (Dist)

[1] Bloomberg Finance, L.P., as of 27 August 2024.

Footnote

Marketing Communication.

Information Classification: General Access.

For Professional Clients Only

The information provided does not constitute investment advice as such term is defined under the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell any investment. It does not take into account any investor’s or potential investor’s particular investment objectives, strategies, tax status, risk appetite or investment horizon. If you require investment advice you should consult your tax and financial or other professional advisor.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU). This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate EU regulator) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

Investing in foreign domiciled securities may involve risk of capital loss from unfavourable fluctuation in currency values, withholding taxes, from differences in generally accepted accounting principles or from economic or political instability in other nations.

The S&P 500® Index is a product of S&P Dow Jones Indices LLC or its affiliates (“S&P DJI”) and have been licensed for use by State Street Global Advisors. S&P®, SPDR®, S&P 500®, US 500 and the 500 are trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”) and has been licensed for use by S&P Dow Jones Indices; and these trademarks have been licensed for use by S&P DJI and sublicensed for certain purposes by State Street Global Advisors. The fund is not sponsored, endorsed, sold or promoted by S&P DJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of these indices.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.Expiry: 31/08/2025

2015149.282.1.EMEA.INST

© 2024 State Street Corporation. All Rights Reserved.

This email is classified as General Access.