Stockholm (HedgeNordic) – As an investment fund specializing in acquiring life insurance policies on the secondary market in the United States for over a decade, Ress Life Investments has effectively demonstrated the return potential and diversification attributes of this asset class. This strategy exploits the structural dislocation of valuations of life insurance policies. Despite the evident financial appeal of the asset class – which collects a financial benefit when the insured passes away, the growing emphasis on Environmental, Social, and Governance (ESG) principles in the investment landscape prompts consideration of the ethical and moral aspects associated with purchasing and owning such policies.

This consideration brings us to the reason behind the existence of the secondary market for life insurance policies. “The existence of a secondary market for US life insurance policies is a consequence of a structural inefficiency in the primary market,” explains Hanna Persson, Head of Sales at Ress Capital. The standard terms for life insurance in the US are often valid until the person reaches the age of 120, while many individuals do not need life insurance coverage once they have retired. “At retirement age, a person who has paid insurance premiums on a policy for many years, may own a life insurance policy with a significant positive value,” explains Persson. “Since the insurance policy has a positive value, the individual policyholder owns a financial asset worth a considerable amount of money.”

“The existence of a secondary market for US life insurance policies is a consequence of a structural inefficiency in the primary market.”

Hanna Persson

An insured who no longer wants, needs or affords the life insurance policy has three different options: 1) lapse the policy by not paying the premiums, 2) surrender the policy to the insurance company for a surrender value or, 3) sell it in the secondary market to capitalize on this asset.

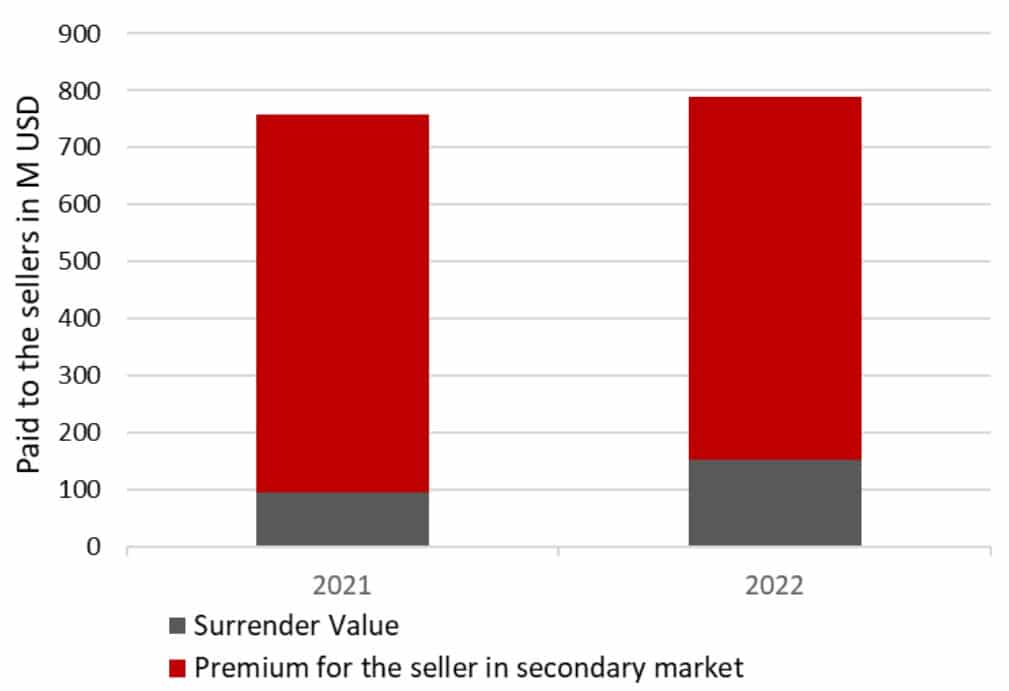

Unfortunately, “Most policyholders are not aware of the possibility to sell their policy,” Persson points out, leading to lapses that result in policies never paying out. In 2022 alone, policies with a total face value of approximately $650 billion lapsed, according to data gathered by the Life Insurance Settlements Association (LISA).

Fund managers such as Ress Capital provide liquidity for sellers and ensure a better pricing mechanism by paying the financial value of the sold policies. Data from the Life Insurance Settlements Association (LISA) indicates that sellers historically received 6-8 times more than the cash surrender value paid by the life insurance companies. The existence of a secondary market for US life insurance, therefore, has social benefits and can be used as an additional alternative funding option for retirement.

The Transaction

For many households in the United States, life insurance constitutes an indispensable component of family financial protection against unforeseen events. “It is of great importance that the sale of a life insurance policy occurs in a way that safeguards the interests of the whole household,” states Jonas Mårtenson, the founder of Ress Capital who also serves on the board of the industry association ILMA in the United States. ILMA actively works for prudent and stringent regulation of the life settlements market.

“It is of great importance that the sale of a life insurance policy occurs in a way that safeguards the interests of the whole household.”

Jonas Mårtenson

Regulatory bodies have duly recognized this need, with the secondary market for life insurance policies subject to regulation in 45 states, thereby ensuring transparency and consumer protection. The sales process of life insurance policies involves only intermediaries registered and authorized by state regulators, with clear reporting of brokerage fees and information about the policy’s surrender value provided to the consumer.

“As a part of the transaction process, the policyholder must certify that he, or she, makes a conscious decision to sell the life insurance policy,” says Mårtenson. “Additionally, beneficiaries, typically spouses or children of the policyholder, must agree in writing to the sale.”

As an active participant in the life settlements market, Ress Capital places a strong emphasis on adhering to ethical standards and ensuring consumer protection. “There is a systemized process for the settlement to take place and no contact will occur between Ress Capital and the original beneficiary of the policy,” emphasizes Mårtenson. The company’s dedication to the development of ethical norms centers around prioritizing the interests of the consumer and promoting a framework that ensures transparency and fairness.

Any Possible Moral Issues Facing the Asset Class

Investors collect policy benefits upon the insured’s death, prompting questions about the morality of investing in this asset class. “It is true that a policy paying out earlier will be beneficial financially. But keep in mind that the opposite holds where individuals outlive their life expectancy,” says Gustaf Hagerud, who is the CEO of Ress Capital and holds a PhD in Financial Statistics. Investing in this asset class, he clarifies, revolves around holding a diverse pool of policies that are paying out either earlier or later relative to mortality expectations.

“The asset class is not about a single individual’s death, it is about a large pool of policies that will either pay out earlier or later, relative to mortality expectations,” emphasizes Hagerud. The law of large numbers brings actual outcomes closer to expected values as the number of policies in the portfolio grows. “Through that mechanism, the longevity risk defined as the uncertainty of outcomes will be reduced.”

“The asset class is not about a single individual’s death, it is about a large pool of policies that will either pay out earlier or later, relative to mortality expectations.”

Gustaf Hagerud

The focus in portfolio management is to create a portfolio with policies that, on average, pay out as expected. Hagerud, drawing from his background in the pension industry with experience at employers such as AP3, AP1, and Alecta, points out that the possible moral dilemma in this asset class can be compared to that present in a defined benefit pension fund or for a financial institution issuing annuities to clients. “In a defined benefit pension fund, the level of cash flows paid to members will depend on the return of the fund’s investments and the survival probabilities of members,” explains Hagerud. “Members who live a shorter life than expected will subsidize members who live longer than expected,” he elaborates. “Thus, a steady pay-out to older members can only be possible if some members have a shorter life. Clearly, this business model is not regarded as immoral.”

Essentially, any product promising cash flows linked to longevity faces the reality of some clients benefiting more than others. However, at a portfolio level, the impact is limited to changes in the average longevity of clients. “It is important to neither under- nor overestimate longevity,” notes Hagerud. “This is true for pension funds, financial institutions issuing annuities as well as for funds that invest in life insurance policies.”

Ress Capital’s Own ESG Efforts

ESG investing has gained considerable momentum as investors increasingly aim to align their financial objectives with sustainable and responsible practices. While life settlements do not have a direct environmental impact, they offer a distinctive avenue for investors to make a positive social impact by facilitating fair compensation for policyholders willing to sell their life insurance policies as described above. Amanda Gustafsson (pictured left), a junior portfolio manager at Ress Capital, and Johan Jonson (pictured right), the asset manager’s risk manager, have been spearheading the team’s efforts to understand how the team can contribute to broader ESG objectives.

“Amanda and I have been looking at our operations to understand how we can incorporate ESG, contribute and make a positive impact on ESG,” says Jonson. As a buyer of life insurance policies, Ress Capital has focused its ESG integration efforts on assessing the risk associated with insurance companies, with a particular emphasis on their ESG ratings, among other factors.

“We are working to ensure that the life insurance companies in our portfolio don’t violate conventions for international agreements on human rights, such as the UN Global Compact or OECD guidelines,” explains Amanda Gustafsson. “To assess this, we retrieve ESG risk data from Sustainalytics and other data providers to make sure we minimize sustainability-related risk in our portfolio.” Sustainability risks are considered both during the investment process and regularly through portfolio screenings. If an insurance company behind certain policies has a poor ESG risk score, the Ress Capital team evaluates how to approach these investments.

“…we retrieve ESG risk data from Sustainalytics and other data providers to make sure we minimize sustainability-related risk in our portfolio.”

Amanda Gustafsson

The second area involves the decision-making process when considering the purchase of a particular policy. “We actively decide when analyzing policies, allowing us to exclude policies we are not comfortable with, either due to the issuing insurance company or other reasons,” according to Jonson. For instance, Ress Capital’s approach to mitigating longevity risk involves acquiring policies from healthy retirees with long life expectancies and opting for conservative estimates of life expectancies, avoiding policies from individuals with shorter life expectancies.

“We actively decide when analyzing policies, allowing us to exclude policies we are not comfortable with, either due to the issuing insurance company or other reasons.”

Johan Jonson

As an Article 8 fund, Ress Life Investments aims to promote social characteristics but does not have sustainable investment as its objective. As an additional step in their commitment to sustainability, Ress Capital signed the Principles for Responsible Investments (PRI) in 2017. In their efforts to effectively incorporate ESG issues into their processes, the team at Ress Capital has engaged with service providers by sending out a questionnaire with a set of questions on ESG-related issues.

Jonson emphasizes the importance of this engagement, stating, “This was a statement to our service providers, indicating that ESG-related issues are important for us and showcasing how we approach this area.” He concludes by acknowledging that Ress Capital, as a small firm with limited resources, can still make a meaningful difference by evaluating its business practices and finding ways to contribute positively to ESG objectives.