By Jessica Henry, Senior Responsible Investment Research Analyst – Man Group: Biodiversity loss is set to significantly disrupt the world economy over the next decade. Despite the data and engagement challenges ahead, systematic and discretionary portfolio managers should not be deterred.

1. Introduction

In the final days of 2022, a historic UN agreement on protecting nature was reached in Montreal at COP15.1 Nearly 200 countries signed up for the Kunming-Montreal Global Biodiversity Framework, a deal designed to halt and reverse biodiversity loss by 2030. Among the four goals and 23 targets set, governments committed to protecting 30% of land and sea by 2030, reforming environmentally damaging subsidies and recognising the rights of Indigenous Peoples.

Dubbed by many as the ‘Paris Agreement of Nature’, the deal has been met with cautious optimism. Many are hopeful that the agreement will drive alignment of public and private flows to protect biodiversity. However, the lack of detail and generic nature of the targets has caused concern amongst some. One aspect that remains indisputable is that the COP15 deal sends a strong message which the financial community cannot ignore.

With so many other ESG issues to track, biodiversity and nature-related risks have often been lost in the mass of concerns related to responsible investing. However, in a post-COP15 world, asset managers must respond to shifting investor priorities and increasing incentives for aligning portfolios with pathways to halting and reversing biodiversity loss by 2030. And whilst the plethora of biodiversity-related challenges cannot be effectively addressed without cross-collaboration across disciplines and decisions grounded in science, asset managers have an important part to play in directing capital away from the ‘worst offenders’ and towards companies providing innovative solutions.

2. Why Is Biodiversity So Important?

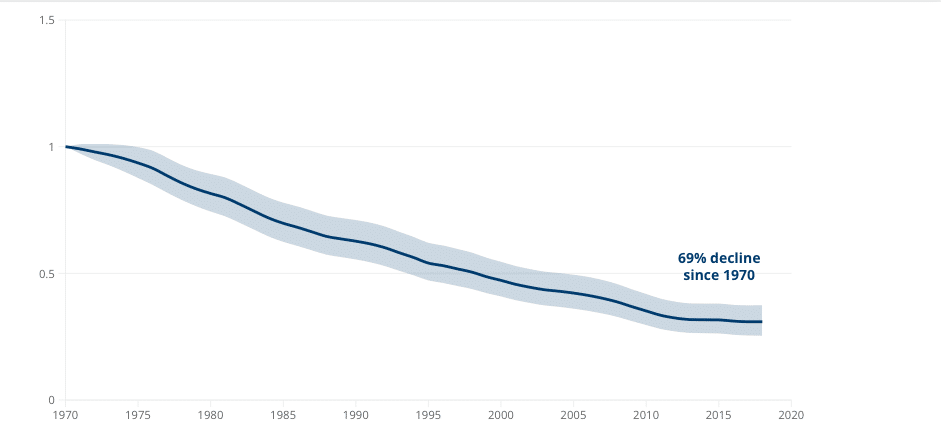

We’ve seen a significant acceleration in loss of biodiversity due to human activities.

Biodiversity in its simplest form is the variety of the different kinds of life found in a particular habitat, either plant life or animals.

An area’s biodiversity may increase and decrease over time due to natural fluctuations in biodiversity, associated with seasonal changes and natural ecological disturbances. The significant risks that we are referring to when we talk about the issue of biodiversity loss, however, are driven by human-driven activities, the impacts of which tend to be far more severe and longer lasting. In recent years, we’ve seen a significant acceleration in loss of biodiversity due to human activities. The five key drivers of biodiversity loss being identified are: changing sea and land use, direct exploitation of organisms, climate change, pollution and invasive species (Figure 1).2

But why is accelerated biodiversity loss such an issue? We depend on the biodiversity of nature in almost every aspect of our daily lives, from the bees that pollinate most of the world’s food production, to the raw natural materials required for medicine. In fact, a study which analysed nature-related socioeconomic risks to cities found that USD 31 trillion of city-based GDP is at risk of disruption, particularly within sectors such as supply chains, energy and travel (Figure 2). Industries may rely on either direct extraction of resources from forests and oceans or the provision of ecosystem services such as clean water, pollination and a stable climate. If biodiversity loss continues at its current rate, an estimated $44 trillion of economic value generation which is moderately or highly dependent on nature could be exposed to risks arising from nature losing its capacity to provide such services.3

Figure 1. The Living Planet Index (1970 to 2018)

Figure 2. Disruption Risk in Cities from Biodiversity and Nature Loss , by Industry (Max = 100)

So, biodiversity is undeniably crucial to the function of the global economy. But why is it especially important for asset managers focus on protecting biodiversity through their investment practices? We’ve identified three key reasons:

- We cannot address the risks posed by climate change without also addressing the biodiversity loss;

- Biodiversity loss is already having a material impact on economic activity across different sectors;

- Biodiversity considerations are becoming increasingly enshrined in global policy, regulation and reporting.

We cannot tackle climate change without taking into account biodiversity.

2.1. Climate

It’s now widely accepted that we cannot tackle climate change without taking into account biodiversity, as the two issues are intrinsically linked. Healthy ecosystems play a crucial role in both climate change mitigation and adaption. Simultaneously, climate change exacerbates risks to biodiversity, from temperature rises affecting the functioning of ecosystems to extreme weather events such a storms and droughts destroying animal and plant habitats (Figure 3). If asset managers are to meet global targets on climate change and mitigate climate risks in portfolios, they will have to consider biodiversity as part of their strategy or otherwise risk harming one objective at the expense of another.

For example, poor quality carbon offset programmes may not only do little to mitigate climate change, but may also have adverse impacts on biodiversity i.e., planting trees to offset carbon on natural grasslands could negatively impact species which depend on open habitats. In addition, consideration of the potential conflicts between biodiversity protection and the energy transition is paramount. Mineral supply chains have extensive, yet often hidden impacts on biodiversity. Future demand for battery metals, such as nickel, cobalt and lithium, for electric vehicles may increase the likelihood that metal-mining companies develop mines in areas with high biodiversity importance.

Figure 3. Biodiversity Threats by Industry and Habitat

Issues relating to biodiversity are already materially impacting a number of sectors, both directly and indirectly.

2.2. Material Impact

Biodiversity loss is not a distant, intangible risk – issues relating to biodiversity are already materially impacting a number of sectors, both directly and indirectly. There are the ‘obvious’ sectors which are directly exposed to biodiversity risk through their activities and supply chains, such as agriculture, construction and fishing. The rise of aquaculture (the practice of fish farming) has boomed in recent years, now surpassing wild-caught fish in a bid to manage rising seafood demand (Figure 4).

Figure 4. Aquaculture Farming Overtakes Wild Fish Capture

But there are also more hidden risks impacting a wider range of sectors. Since biodiversity risks are not confined to the physical, companies may also be exposed to a host of legal, regulatory and reputational risks. In order to paint a more holistic picture of risks to bottom lines and portfolios, investors need an increased understanding of the specific biodiversity issues facing the companies they are invested in. It is only then that we can start meaningfully incorporating biodiversity into risk models and have more focused, constructive engagements with portfolio companies to drive positive change.

2.3. Global Policy and Regulation

Finally, the shift in focus to biodiversity from a global regulatory and policy standpoint means asset managers and companies will be under increasing pressure to monitor and manage biodiversity-related risks. For asset managers, this means elevated client focus on how biodiversity considerations are being incorporated into investment strategies and active ownership activities. For corporate assets, non-physical risks (such as those related to regulation) will be elevated across an increasing number of jurisdictions. For example, post COP-15, we may see more private projects being delayed or halted indefinitely as governments put measures in place to align with global biodiversity efforts.

3. How to Incorporate Biodiversity Considerations Into Considerations Into Investment Processes

Due to corporate disclosure being so poor, companies may be rewarded with higher scores for simply disclosing information on biodiversity, whether good or bad.

3.1. Approaches

Any strategy looking to incorporate biodiversity considerations, whether systematic or discretionary, should be mindful of oversimplifying an incredibly complex topic. For example, caution is required when looking at top-level biodiversity scores: due to corporate disclosure being so poor, companies may be rewarded with higher scores for simply disclosing information on biodiversity, whether good or bad. And since biodiversity disclosure is currently highest amongst the most impacted sectors, such as metals and mining, these companies may look relatively better based on top-level metrics linked to disclosure.

We believe that there are two main ways of incorporating biodiversity considerations into investment strategies:

- Mitigating biodiversity-related risks; and

- Investing in solutions.

In terms of solutions, managers may focus on investing in ‘biodiversity leaders’, (companies deemed as providing innovative solutions for preventing biodiversity loss or supporting biodiversity restoration) or in ‘enablers’ (companies further down the value chain which provide vital support and services to the leading companies). An example of an enabling company might be a biotechnology company developing an environmentally friendly pesticide which will help agribusinesses protect biodiversity. Importantly, investing in enabling companies allows exposure to biodiversity themes across a wider range of sectors, expanding the initial investment universe.

Investors should consider both the impact a company has on biodiversity through its operations and activities and its exposure to biodiversity-related risks.

If taking a risk management perspective, investors should consider both the impact a company has on biodiversity through its operations and activities (its ‘biodiversity footprint’) and its exposure to biodiversity-related risks. Through adopting a double materiality approach, managers will be able to focus on the most affected companies and assess how well they are managing potential risks.

3.2. Metrics and Scores

There remains a distinct lack of consensus on which metrics to prioritise in terms of both identification and mitigation of nature-related risks. This poses challenges for asset managers, whose investment activities are informed by regulation and often reliant on industry-standard frameworks and metrics to guide approaches on material ESG issues. The Task Force for Nature-Related Financial Disclosures (‘TNFD’), a global reporting initiative, should provide more clarity when it comes into play in late 2023. In its absence, however, investors should start exploring the various metrics and approaches since we don’t have the luxury of time to wait for guidance to materialise before addressing material biodiversity issues.

Biodiversity metrics can be divided into two groups: (1) granular metrics on specific topics, (such as deforestation and land use) ; and (2) holistic metrics or scores (which seek to quantify an issuer’s total biodiversity footprint and biodiversity dependency). It’s not necessarily the case that we will see a convergence in approaches to one holistic metric over time, in a similar manner to how emissions are used as a proxy for impact on climate. Biodiversity is inherently more complex, multi-faceted, and spatially variable.

One of the most the widely used metrics is mean species abundance (‘MSA’). This is a measure of local biodiversity intactness and has been adapted to seek to capture a company’s impact in terms of biodiversity degradation under one aggregated result. Several asset managers are already using variations of MSA metrics for reporting and investment purposes, and we deem this metric to be a useful starting point. However, we believe used on its own in its current form is not sufficient to comprehensively portray the full spectrum of impacts a company may have on local ecosystems. The metric currently relies heavily on modelled data and global biodiversity averages since corporate disclosure on this issue is typically limited and low quality. Although the efficacy of the metric is likely to increase as corporate disclosure improves, proper analysis should consider a range of other factors, including further location specificity (which MSA currently uses proxies for). This latter point is crucial as biodiversity is unequally distributed around the world, which means global averages may be misleading when applied to local conditions.

Data providers have also sought to produce holistic metrics, such as corporate biodiversity footprints and corporate biodiversity risk scores. Some of these scores may incorporate elements of MSA but others may take completely different approaches. Approaches may involve combining geospatial data on the location of companies’ operations and supply chains with a range of biodiversity datasets, or incorporating natural language processing to identify non-physical, reputational risks.

In addition, corporates have produced their own metrics. Notably, Kering developed an environmental, profit and loss measurement tool which seeks to quantify the total impact of the firm’s activities on nature. The tool measures carbon emissions, water consumption, air and water pollution, land use and waste production along the entire supply chain. These impacts are then converted into monetary values to quantify the use of natural resources. A number of other large corporates, such as Philips and Vodafone, now also report environment, profit and loss.

It’s important to note that when seeking to identify how a company may be exposed to biodiversity risks, investors cannot rely solely on quantitative metrics as deep analysis of a company’s entire value chain is required. In addition, some understanding of the legal and regulatory environment in which companies operate is essential to assess the likelihood and magnitude of the potential legal and reputational risks a company may face, along with a view on the credibility of companies’ plans to manage these risks.

Across MSCI ACWI constituents, 36% of companies report having biodiversity policies in place.

3.3. Engagement and Stewardship

Engaging with portfolio companies on their impact on nature and the risks that they are exposed to is an important step all managers can and should take. Simply asking companies whether they have a biodiversity policy is a useful starting point to encourage greater transparency and awareness. For example, across the MSCI ACWI constituents, 36% of companies report having biodiversity policies in place. However, far fewer companies have land impact reduction policies or project assessments for environmental impact (Figure 5). Engagement work will need to evolve quickly to delve further into company and sector-specific biodiversity issues and drive impactful engagements. The formation of collaborative engagement initiatives, such as Nature Action 100+, will also help in bringing concerted action towards key sectors deemed systemically important in reversing nature and biodiversity loss.

Given that many companies themselves do not fully understand their own biodiversity risks and dependencies, there are also opportunities for asset managers to increase awareness at the corporate level. For example, asset managers can employ the use of geo-spatial biodiversity datasets that companies themselves may not have access to, to inform engagements surrounding more hidden, localised supply chain risks.

Figure 5. Disclosure Rate of Select Biodiversity-Related Metrics from MSCI AC World Constituents (%)

There are alpha opportunities for asset managers able to make sense of messy and disparate ESG datasets.

4. Challenges Arising from Poor Quality Biodiversity Data

Poor quality data is frequently cited as one of the greatest barriers to incorporating ESG considerations. While we believe that there are alpha opportunities for asset managers able to make sense of messy and disparate ESG datasets, the current lack of corporate disclosure on biodiversity issues poses challenges to even the most data-savvy managers.

The absence of clearly defined industry frameworks, coupled with limited consensus on which metrics to prioritise, means that many companies are unsure of what to focus on in terms of reporting on nature-related risks. Compounding this issue is the existing burden corporates face for other ESG-related reporting requirements, such as climate reporting under the Taskforce for Climate-Related Financial Disclosures (‘TCFD’) which will become mandatory in 2023 for large publicly listed companies.

As a result, corporate disclosures on biodiversity are poor, being both low in coverage and inconsistent. As such, much of the existing corporate-level biodiversity data tends to be either modelled or estimated, impacting the efficacy of biodiversity metrics. For discretionary managers, a deep-dive analysis into companies’ business models and value chains can substitute lacklustre. However, for many systematic strategies which at the mercy of inputted data, the challenge to surmount is much greater with little obvious remedy in the short term.

Neverthless, we do foresee positive tailwinds, such as the advent of TNFD, which puts biodiversity at the forefront of corporates’ reporting agendas (Figure 6). Although it is initially voluntary, it’s likely that TNFD will eventually become mandatory for publicly listed companies. And while biodiversity is inherently more complex than climate, corporates should be better positioned to adhere to new reporting requirements with relevant experience and infrastructure in place from addressing TCFD requirements.

Figure 6. Change in Reporting rate by Sector – 2020 Versus 2022

As data and methodology improves, making biodiversity a key part of the responsible investing criteria of a strategy will become easier.

Conclusion

For the foreseeable future, incorporating biodiversity concerns into investment portfolios will remain a challenge. Nevertheless, the importance of the issue cannot be overlooked: without concerted action, accelerated biodiversity loss is set to significantly disrupt the world economy over the coming decades. As such, asset managers have a part to play. Discretionary investors can – and should – be analysing the biodiversity record of companies within their portfolio and demand higher levels and disclosures from corporates. As data and methodology improves, making biodiversity a key part of the responsible investing criteria of a strategy will become easier and more mainstream – for both systematic and discretionary investors.

1. 15th Conference of the Parties to the United Nations Convention on Biological Diversity.

2. Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES), Models of Drivers of Diversity and Ecosystem Change.

3. World Economic Forum (2020).