Private assets are an increasingly important source of returns and diversification. The Q&A with Shaniel Ramjee, Senior Investment Manager of Multi Asset, Pictet Asset Management, takes us through the opportunities private markets offer, as well as the risks they pose.

Q: What do you see as the defining features of private equity – both as companies and as investments?

A: There are many reasons why companies might choose to remain private. They might be family owned, or not want to be subject to the administrative burden of public listing, or to the short-termism imposed by quarterly reporting. Typically they are in a different part of their lifecycle – usually at an earlier stage – from publicly-traded firms. They might have just found their niche in the world of business and are starting to grow. It’s at a stage where a lot of exciting things happen to some of these companies. And where a bulk of their returns is often generated. So for investors to be able to access investments at this stage is particularly interesting.

Q: Does it make any difference being a Europe-based private equity investor?

A: Europe has a long history of private companies, many of which have been in existence for decades and controlled by a founding family. These companies are extreme specialists in what they do. And there are lots of them – there are 23 million small and medium-sized enterprises (SMEs) in Europe, employing two-thirds of the region’s workforce. But we see with increasing frequency in these companies that younger generations are less involved in the business, or indeed, a first round of professional managers have stepped into the business hoping to expand or grow it.

Private equity can be one of the ways in which they do that without relinquishing family control. So they’re able to get financing through the private markets but still retain that ability to have that long term management style, long term vision in terms of where the company is going and how to grow it. They don’t need to go to the public market. They can align themselves with private equity capital, which has a similar mindset to that long term investment style. Private debt becomes important here too – historically, these companies were much more dependent on bank loans, but these can be relatively inflexible compared to contracts that can be struck with private lenders. But for the most part private lenders have focused on larger companies, so it’s a wide open field for new entrants focused on SMEs.

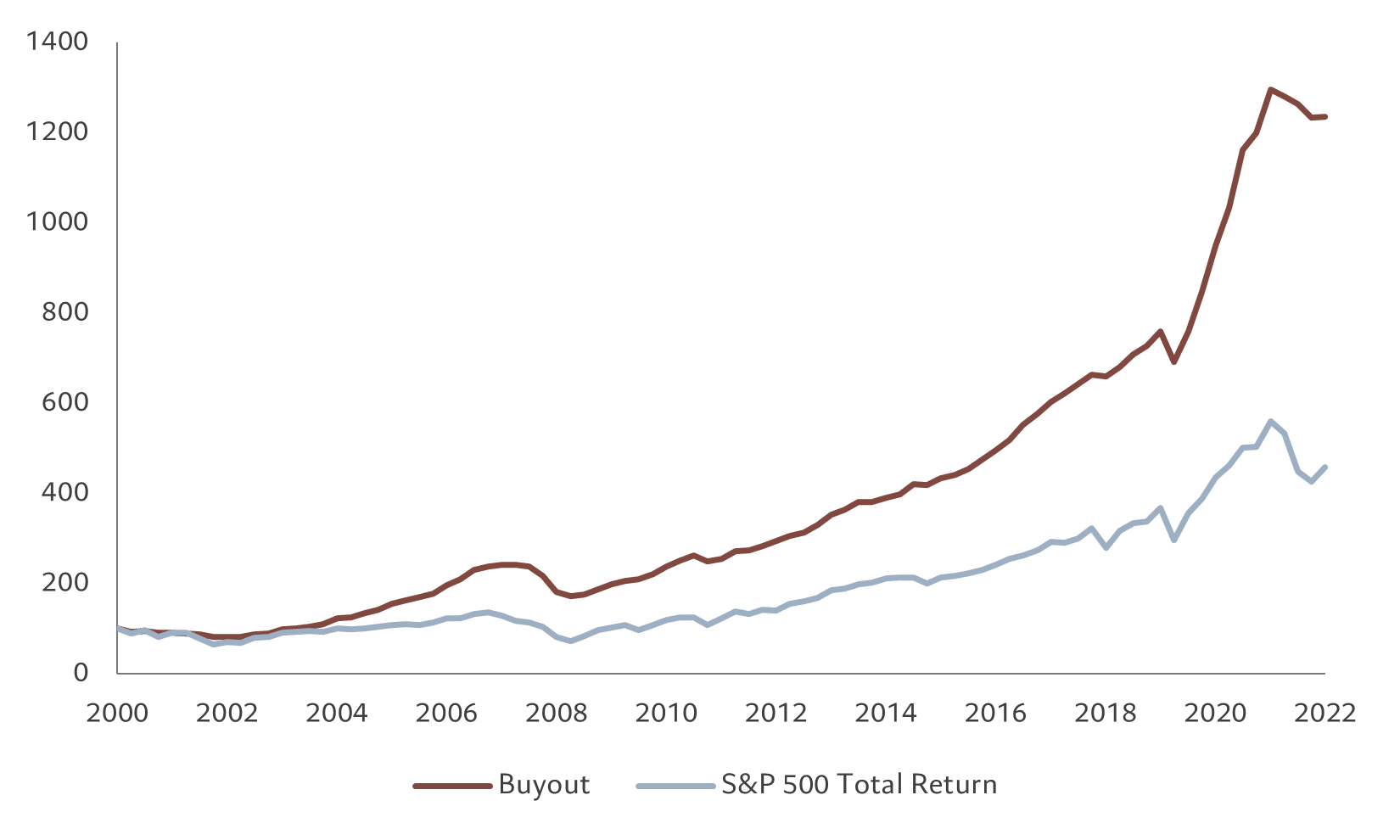

Performance of Private Equity Buyouts vs S&P 500, rebased Dec 2000 = 100

Source: Prequin Pro, Pictet Asset Management. Data covering period 01.12.2000-31.12 2022

Q: Ultimately, is what makes private assets special the fact that they are illiquid and that investors expect to be paid a premium for holding illiquid assets?

A: The illiquidity premium in and of itself doesn’t garner extra return. It’s what you do with that illiquidity that matters. So, for example, private companies are able to set longer term objectives, longer term goals, which management can work hard to achieve without having to focus on the market’s quarterly reporting demands. We believe that illiquidity in itself doesn’t generate the return, it’s the value creation it allows that does.

It’s also important for investors to really understand how much illiquidity they can manage in their portfolios. They need to realise the degree to which leverage was employed in private equity and to have a very clear understanding of what the value creation proposition was in private equity deals, especially now that interest rates have gone up.

Q: Rising interest rates have clearly been a wider risk for the markets, but are there any risks that are specific to private assets?

A: Due diligence is crucial. We know that, on the face of it, these companies are slightly less transparent than those in the public markets. So what investors in private equity partnerships need to understand is how these due diligence processes are undertaken and the guiding philosophy of each private equity transaction that is undertaken. Meanwhile, private equity teams need to be able to source deals in a competitive landscape.

Vintage diversification – holding a spread of investments in private equity companies, coming due in different years – therefore, is extremely important because we know once we’re invested, we are invested for quite a long time, we might be able to choose when we start investing, but when we start after that, there’s very little we can do about the economic environment. So understanding how the thinking behind investments that are being made in various economic environments is extremely important in that risk management.

Exits are also important. When conditions for initial public offerings (IPOs) are robust, taking private companies public becomes more likely. But in some market environments this is more difficult. In those circumstances, expertise in trade sales becomes necessary, that’s to say selling companies to other parts of the value chain – mergers and acquisitions that build conglomerates that become worth more than the sum of their parts.

Q: What does that sort of concentration imply about the relationship between investors in private markets and the assets they hold?

A: In all private markets, the investor or the manager is very close to the companies in which they invest. It really is an active approach.

They’re close to the boards. They often have seats and they are able to draw on not just their capital to fund the growth of these companies, but also their know-how, their expertise, their operational excellence to build these companies over time.

That’s not just private equity, but private debt and private real estate.

For example, in private debt, investors can write specific needs or objectives into the contracts they make with borrowers, in other words the terms and conditions of the of the loans.

These can be around key points of company performance or even something broader – think about sustainability of a company in terms of its environmental impact and goals around that. For example, if the company has a target of, let’s say, reducing its carbon footprint over time, the contract could be written such that the coupon on its borrowings drops once the target is hit. Its borrowing costs drop. But the investor benefits because in hitting its targets, the company becomes more secure and its credit rating rises. Everyone wins. In a way, private markets offer a much more active role to investors.

In many cases, this develops into a very strong symbiotic relationship between the private equity or debt managers and the companies in which they invest. That is true active investing.

Q: As an asset manager, does it make a difference to you that the firm you work for is also privately held?

A: Absolutely. I think at Pictet we understand uniquely what strength private structure gives us: the ability to think long term; to invest long term; to be able to be contrarian at times; and to think about what truly matters in terms of growth. It is always about the quality of that growth, not just the quantity or the speed. And we appreciate that.

For more information, scan the QR code or visit am.pictet

Important notes

This marketing material is for distribution to professional investors only. It is not intended for distribution to any person or entity who is a citizen or resident of any locality, state, country or other jurisdiction where such distribution, publication, or use would be contrary to law or regulation. Any investment incurs risks, including the risk of capital loss. Information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.