By Peter Lindahl and Mattias Lagerspetz, Evli systematic funds team: From a factor investor’s perspective, such as ourselves, quality is in many ways the new kid on the factor block. This might sound strange, since quality has been around as an investment approach at least since the Great Depression. To a great degree, quality investing is one of the more “fundamental” equity styles. Nevertheless, academic research has over the past couple of decades found different aspects on what quality investing might entail.

The many flavors of quality investing

There is no perfect answer on what quality is or how it should be defined. However, some relevant definitions have been presented through some renowned asset pricing models. Fama and French (2015), in their five-factor model, include profitability and investment as quality factors. In other words, companies which are more profitable and make less investments are shown to outperform. Also, the Q-factor model introduced by Hou, Xue and Zhang (2015), include profitability and investment as robust quality factors.

Besides these definitions, many other ways to measure quality have been proposed through leverage, accruals, earnings stability, payout and so on. Simply put, quality consists of not one but many different metrics. However, many of these quality measures have low correlations with each other. Hence, from a theory point of view, a valid risk factor which explains the quality premium seems hard to find. Contrarily, behavioral theories make more sense in trying to explain the quality factor.

There is no perfect answer on what quality is or how it should be defined. Simply put, quality consists of not one but many different metrics.

Intuitively, one may think that high quality is something you must pay a premium on. However, empirical studies have demonstrated that this is not necessarily the case. Yes, quality stocks tend to be more expensive, but less so than would be expected. Furthermore, evidence has been presented that analysts overestimate the earnings outlook for low-quality stocks, hence underestimating estimates on high quality stocks (Asness, Frazzini and Pedersen (2018)).

Profitability appears as one of the more robust quality definitions. Furthermore, profitability seems not to overlap too much with any other of the common factors.

Nevertheless, profitability appears as one of the more robust quality definitions. Furthermore, profitability seems not to overlap too much with any other of the common factors. The (Low) investment factor looks to have a high correlation with value. Leverage and capital structure measures are found to have an exposure to low risk factors (Hsu, Kalesnik and Kose (2017)). Growth measures, with regards to particularly earnings surprises, tend to have exposure to the momentum factor. Payout seems independent from other factors although it has been deemed to be a combination of low risk and value.

Quality may already be back in style

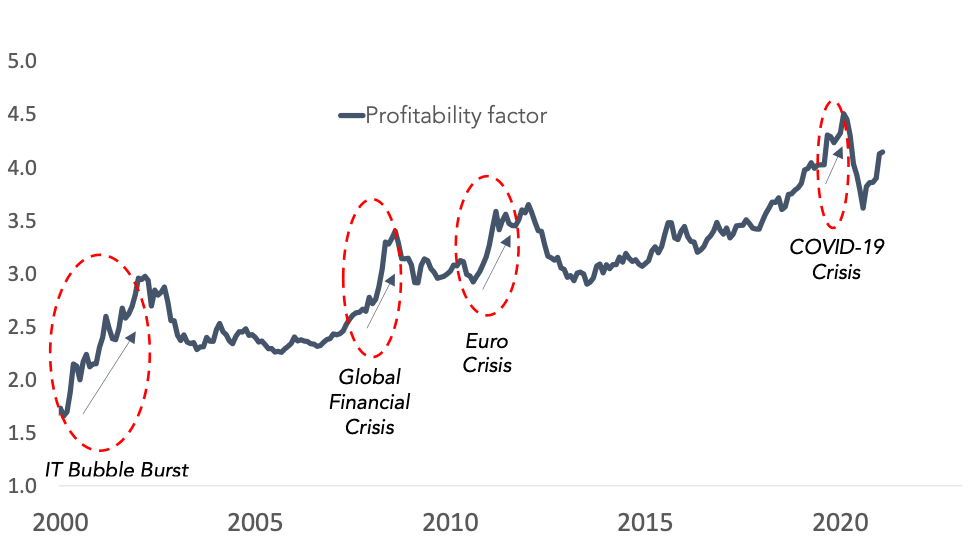

According to the various asset pricing factor models, quality stocks should be held in any portfolio targeting higher expected returns in the long term. However, in the short-term, quality stocks may underperform from time to time, and even for longer periods of time. Many studies have demonstrated a defensive nature in quality stocks, which makes sense. According to our own research, profitability seems to do better in relative terms when the economy is in a recessionary business cycle.

Currently, valuation measures point to extreme (expensive) levels in many stock markets, especially in the US. That said, we believe it may be sensible for long-term investors, who do not wish to reduce their equity allocations yet, to increase the defensiveness of the equity portfolio through a quality exposure.

During 2021, the global economy is entering a more mature mid-cycle. In the past, mid-cycles have been good entry points for quality styles. The global economy already reached peak growth in the spring; hence a more typical growth cycle is likely ahead of us before the economy starts to slow down eventually. Quality often does relatively well in such a cycle.

How to invest in quality?

Leaving formal factor models aside, practical applications in quality investing can be built in many ways. Quality metrics commonly used in practical applications are a bit of a motley crew that are each related to other factors.

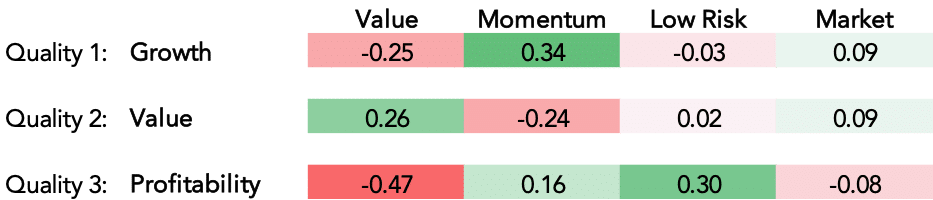

Using our proprietary Evli Atlas framework, we composed a set of global equity long-short portfolios (market cap weight, tilted) constructed using a (admittedly fairly arbitrary) list of metrics that could be broadly interpreted as quality. We further broke down the portfolios to three groups.

The first “growth” group, comprising 5-year sales growth, abnormal returns and standardized unexpected earnings is clearly positively correlated to momentum and negatively correlated to value. Perhaps unsurprisingly so, as all the metrics are related to the company’s growth.

The second “value” group includes accruals, balance sheet growth, cash flow to price and the payout yield metrics. Opposite to the first one, this group has commonalities, as one would guess, with the value factor.

The third “profitability” group is formed by earnings stability, return on equity and return on assets. The third group is closely related to the low volatility factor and has a strong negative correlation to value.

Constructing your unique quality portfolio

We believe that using these kinds of different building blocks, investors can “tilt” their quality portfolio in different directions. Quality investing lends itself efficiently to investors for expressing their individual preferences.

A more defensive nature is possible if you build the model using metrics from the profitability group and possibly the accruals metric, which signals conservative bookkeeping.

An investor may use metrics of the value group to buy into more reasonably priced stocks. Perhaps the more opportunistic may want to combine profitability, value and low risk to aim for a more (Warren) Buffettesque investment strategy.

Instead of playing defense, an investor may want to be more offensive, and pick metrics from the growth group and do well in strong markets.

As with any type of quantitative investment style, there is not only one correct way to do quality investing. Implementation details, ranging from the choice of portfolio weighting methods, benchmark orientation to neutralizing unwanted factor exposures are important considerations for all investment portfolios.

However, in practical applications of quality, even greater attention to detail is required in the selection of the metrics, as the resulting portfolio characteristics can vary to a much greater extent than with many other investment styles.