By Yann Groeger and Michael Wehrle of BlueOrchard, Schroders: Impact investors are used to looking at their investments and seeing more than just the financial return. Uniquely positioned to change society and the environment for the better, impact investments have become synonymous with sustainable investing goals. But that’s not all. They can also offer genuine diversification and compelling returns.

Over the past decade, two major themes have been instrumental in shaping investor behaviour: low rates and a rising awareness of environmental, social and governance (ESG) issues.

Record low rates have driven investors to either move up the risk spectrum or consider alternative or niche opportunities. Meanwhile, growing mindfulness about ESG has led to a huge increase in the stature of impact investing.

Impact and ESG-themed debt investments are often in the form of private rather than publicly traded debt. This is due in part to the smaller size of many of the issuers and the fact that private debt instruments can be more tailored to include impact and ESG-focused elements.

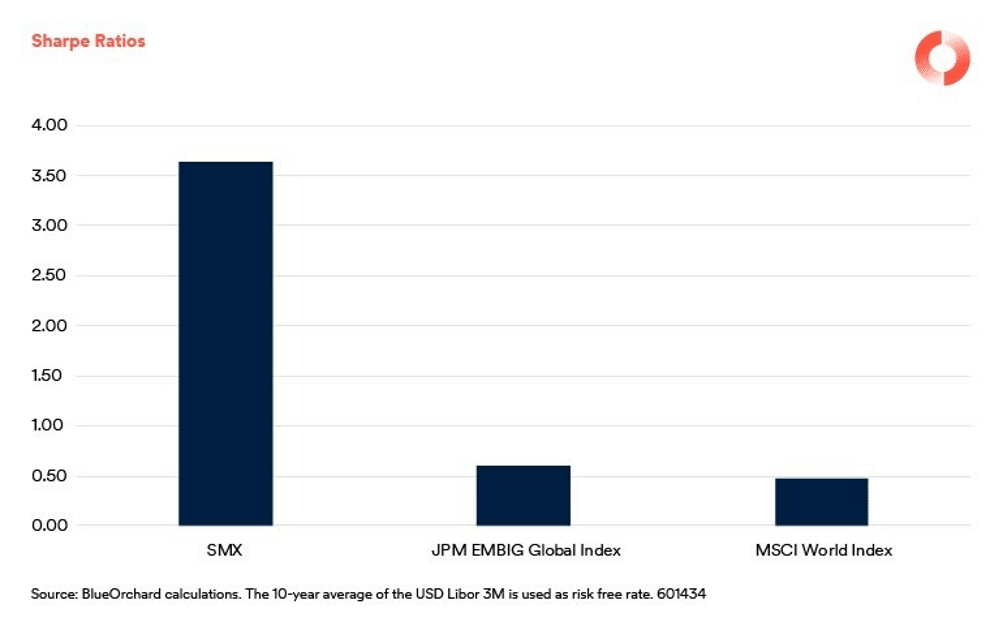

In addition to being better positioned for positive impact and ESG, private debt strategies can also offer higher risk-adjusted returns to investors. Outlined below, the Symbiotics Microfinance Index Sharpe Ratio – a measure of return adjusted for risk – as well as the index’s spread relative to public emerging market bonds, both compare favourably.

These extra returns can be split into illiquidity premium and complexity premium. The illiquidity premium compensates investors for the risk of tying up capital in a less liquid asset. If the market should fall, investors will need to stomach price drops.

In the current zero-yield world, investors have increasingly started to accept the illiquidity premium, with some even actively seeking illiquidity. However, the rising popularity of private markets means the illiquidity premium is in all likelihood, reducing.

But higher returns also exist due to complexity premiums inherent to private debt. Non-standard transactions need customisation – from analytics to legal work – and have various idiosyncrasies. They also lack a secondary market.

What is true for private debt overall, is particularly true for private debt in emerging markets (EM), where many impact investments are focused. Access is rather restricted and local circumstances are more unpredictable.

A private debt transaction with an investment-grade institution in Chile can yield more than twice as much as a public debt instrument from the same institution. We have seen an example of a private debt instrument carrying a spread of 230 basis points (bps) over USD 3 month Libor, versus 100 bps on the public debt instrument.

Complexity Premium in Impact Investment

The complexity premium refers to the additional return investors can earn as compensation for the extra work they have to put in for sourcing, and making the deal work.

Access to these deals is more restricted and requires dedicated resources. Illiquidity and complexity as reasons for higher returns is increasingly the subject of academic research.

A recent paper¹ by economists from universities in Trento, Italy and Wiesbaden, Germany, uses a multi-variant regression analysis on loan interest rates, credit, and market factors to analyse individual components of private debt returns.

The authors conclude that there is a large residual component in private debt returns that remains unexplained by credit, volatility or liquidity. They attribute it to the complexity inherent in private debt transactions.

The logic is that if a transaction involves a greater degree of complexity, this will naturally narrow the field of investors who are able to analyse it. This reduces the supply of capital, thereby improving the risk-adjusted return available to those investors that are willing to undertake the necessary work.

Sourcing Private Debt Transactions

The main challenge in sourcing private debt transactions is that gaining access to institutions in EM is not easy. Investors depend on resources with relevant networks.

Conventional platforms like Pitchbook are only of limited use, as most transactions would not be listed there. It is therefore essential to be able to count on a strong local presence and relationships that have been developed over time, even more so in the context of EM where relationships and trust matter a lot.

In many instances, investors can rely on intermediaries or brokers to identify potentials as well. These are specialised firms that focus on certain sectors, manage a client pool of institutions that are seeking to increase financing.

Alternatively, investors can also engage with others to form a club or syndications for specific transactions. We can illustrate how this works with a real-world example.

Case study – sourcing and deal execution with a microfinance institution (MFI) in Bolivia

The MFI is a traditional institution with a strong social orientation and overall solid financial position. It manages total assets of about $400 million, serving roughly 220,000 micro-entrepreneurs. The average loan size is close to $1,500 and the MFI finances both individual businesses and lends through groups, benefiting from the traditional group solidarity scheme (by which the group is liable for loans of one of its members). 76% of clients are female, working in trade or agriculture. The MFI’s operations are spread across 73 locations and employ more than 1,300 people – a complex organisation.

During the (virtual) due diligence, we looked particularly closely at portfolio quality metrics. Prior to the pandemic, the MFI consistently kept “portfolio at risk 1” loans (loans with 1 day of delay in payment) below 1.8% between 2017 and 2019. As of Jan-21 the ratio of non-performing loans (NPLs) was of 1.4%.

The MFI operates as a non-bank financial institution (NBFI) under the supervisory umbrella of the banking regulator. As for many others in this segment, access to its information is rather restricted, as it does not publish many details on its accounts.

In 2021, the MFI is looking to grow its loan portfolio and has therefore sought out potential funding partners. Access is via an established network of investors. No roadshow was organised, or a professional broker engaged. Still, the pipeline was quickly closed – reaching about $42 million in international debt.

As in many other cases in emerging market private debt, additional complexity may arise on the legal side. Contracts in Bolivia must be tied to local regulations that can be very specific and not always intuitive. Investors need legal counsel with local knowledge to ensure fair treatment and protections.

Another challenge is the lack of publicly available information. It’s safe to say that default statistics are generally less accurate in countries like Guatemala or Nigeria than they are in OECD countries. Investors have to collect data directly from portfolio companies and other sources and develop monitoring tools to keep up-to-date.

Control, Transparency and Security

For investors who are willing to engage in the extra work involved in complex transactions, attractive return is not the only sweetener. Private debt transactions in EM offer access to detailed, privileged information.

Individual security agreements and tailored covenants are commonplace and provide protections not typically available to public debt owners. Covenants can prove instrumental, for instance, if capital adequacy deteriorates.

Last but not least, the extensive due diligence process positions private debt very well in terms of ESG and impact assessments, as policies and implementations can be reviewed and monitored individually.

These in-depth reviews serve to pin-point key deficiencies and achievements in the implementation of environmental policies, consumer protection, social impact and other areas. Investors can dive into details not always disclosed in published documents.

This allows for more precise impact and ESG assessments and monitoring of impact objectives.

Invest with Intent

To benefit from the double (financial and impact) benefits, firms need a dedicated and specialised workforce. It’s also important to be locally present, with own teams or via intermediaries.

In-country knowledge is as important as relationship building. In the private-assets business, both sides need to develop a standard of trust.

With impact and ESG-themes becoming “mainstream” and the search for better returns as challenging as ever, impact-focused private debt is a natural fit for a rising number of investors.

The complexity premium inherent to these investments is a result of hard-won experience and skills.

But it’s worth it.

[1] Giuzio et al. (2018) – The Components of Private Debt Performance

Title Pic: by johan10 – envato.elements