Stockholm (HedgeNordic) – Nordic hedge funds advanced in April for the sixth consecutive month, with the industry gaining 4.1 percent in the first four months of 2021. Nordic hedge funds, as expressed by the Nordic Hedge Index, were up 1.2 percent on average (93 percent reported) last month, with equity managers driving the gains.

All five strategy categories within the Nordic Hedge Index enjoyed gains in April, with equity managers topping last month’s performance chart. Equity hedge funds, this year’s strongest-performing strategy group in the Nordic Hedge Index, gained 1.7 percent last month to take their 2021 advance to 6.7 percent. Nordic CTAs closely followed suit with an average gain of 1.5 percent, which brought the group’s 2021 performance further into positive territory at 2.4 percent. Last month, funds of hedge funds and multi-strategy hedge funds advanced 1.3 percent and 1.2 percent, respectively. Fixed-income vehicles edged up 0.4 percent in April.

At a country level, the Finnish hedge fund industry gained the most in April, with all 14 members posting positive gains for the month. Finnish funds gained 2.2 percent on average in April to bring the 2021 performance to 6.6 percent. Norwegian and Swedish hedge funds gained a similar 1.3 percent last month. Swedish hedge funds, which account for the largest portion of the Nordic hedge fund industry, were up 3.1 percent in the first four months of 2021, whereas Norwegian funds gained 6.2 percent during the same period. The Danish hedge fund industry, dominated by fixed-income vehicles, gained 0.7 percent in April to extend the year-to-date advance to 3.5 percent.

The dispersion between last month’s best- and worst-performing members of the Nordic Hedge Index decreased month-over-month. In April, the top 20 percent of Nordic hedge funds gained 4.2 percent on average, while the bottom 20 percent lost 1.3 percent. In March, the top 20 percent were up 5.2 percent on average, and the bottom 20 percent were down 3.0 percent. About four in every five members of the Nordic Hedge Index with reported April figures posted gains last month.

Top Performers in April

Long/short equity fund Coeli Absolute European Equity, managed by Malmö-based fund manager Mikael Petersson, was last month’s best-performing member of the Nordic Hedge Index with a monthly advance of 8.3 percent. The fund gained 17.1 percent in the first four months of 2021, rounding up this year’s top five list of best-performing Nordic hedge funds. Activist investor Accendo followed suit with a similar 8.3 percent advance in April. Accendo gained 23.2 percent in the first four months of 2021 and currently sits as the third best-performing member of the Nordic Hedge Index this year.

Systematic value-focused fund HCP Quant gained about 6.0 percent last month to take its 2021 advance to 33.4 percent. The fund managed by Pasi Havia sits second in the table of this year’s best-performing members of the Nordic hedge Index. IPM Systematic Macro Fund gained 5.6 percent in April in the final days of the systematic macro strategy. In late April, Swedish systematic investment manager IPM announced that the firm ceases all investment activities and returns capital to investors. The “Best Nordic CTA” at the 2020 Nordic Hedge Award, Volt Diversified Alpha Fund, advanced 5.5 percent in April to bring its 2021 performance to 2.3 percent.

Biggest Performance Surprises

Hedge funds exhibit different risk-return profiles and hence experience different levels of volatility in their returns. With a return of 3.5 percent in April, Coeli Multi Asset enjoyed the highest above-own-average return relative to its historical volatility in returns. The 3.5 percent-advance was 2.3 standard deviations above the fund’s average monthly return. IPM Systematic Macro Fund advanced 5.6 percent last month, which was 1.6 standard deviations above its average monthly return of 0.48 percent. Volt Diversified Alpha Fund’s gain of 5.5 percent was 1.5 standard deviations above its average monthly return since inception.

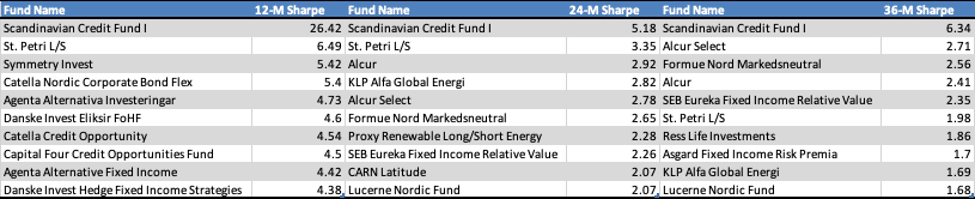

Highest Sharpe Ratios

Given the heterogeneous nature of hedge fund strategies, absolute performance numbers do not always reflect how successful hedge funds are. Risk-adjusted measures such as the Sharpe ratio are a good starting point in the process of identifying the best-performing hedge funds. The three tables below display the Nordic hedge funds with the highest Sharpe ratios over the past 12 months, past 24 months, and 36 months.

The Month in Review for April 2021 can be downloaded below:

Photo by Charles Deluvio on Unsplash