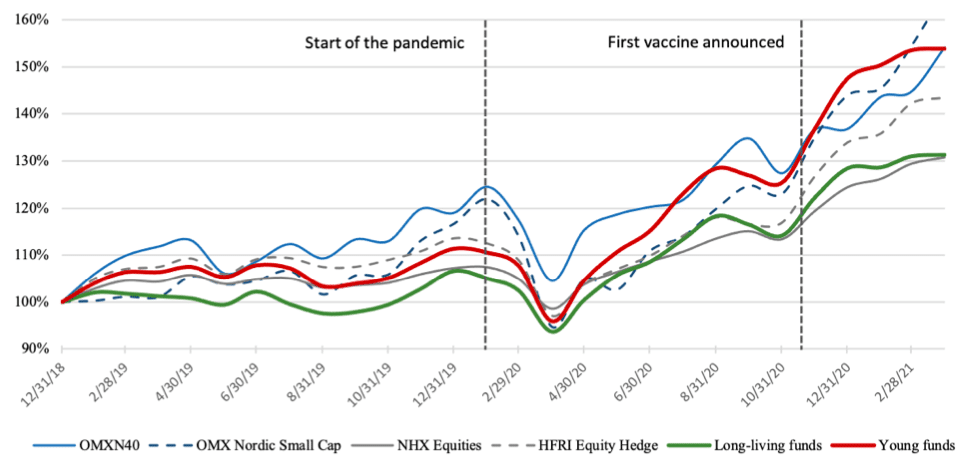

By Danielius Kolisovas – In January 2021, the BBC published a report on how the coronavirus pandemic changed the world economy. As the number of Covid-19 cases grew in the first months of the “crisis,” major stock market indices experienced steep falls that were comparable with the drawdown in 2008. Governments around the globe imposed extensive lockdown measures affecting a wide variety of services, unemployment rates increased, retail footfall dropped significantly, and global production chains came under serious pressure.

After recovering the lost ground during the February-March period, the major European, Asian and US stock markets have advanced further ahead following the announcement of the first vaccine to be available in November 2020. Despite suffering their worst quarter on record in the first quarter, Nordic equity hedge funds delivered a return of 16.1 percent last year, making 2020 the second-best performing year since HedgeNordic started tracking the industry in 2005.

Figure 1. The impact of pandemic on the stock and Nordic hedge fund indices.

In HedgeNordic’s 2021 “Nordic Hedge Fund Industry Report,” I presented some data showing the ability of long-living hedge funds to generate long-term alpha both in quiet and turbulent times. However, the Covid-19 crisis does not appear to have touched the financial markets. One may ask, has Covid-19 denied the “Law of Gravity” of the financial world? How did hedge fund managers adjust their equity investment strategies? And finally, did fund managers deliver excess returns, or alpha, in this unusual Covid-19 period?

Performance Decomposition

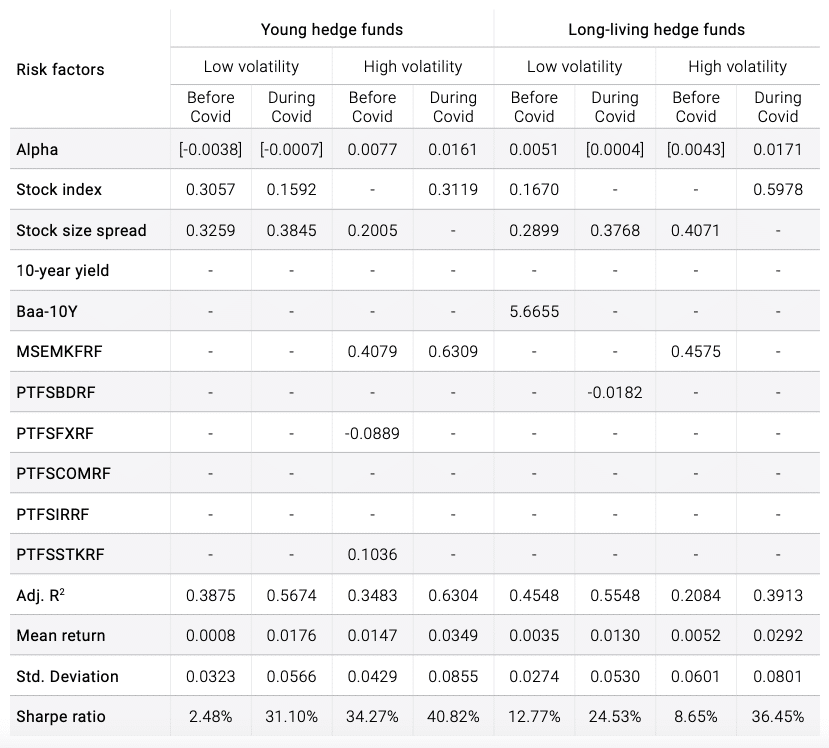

Let’s discuss these issues by analysing equity hedge funds using panel data regression models on cross- sectional data of pooled hedge fund returns. The funds were grouped into pools based on the following rules. First, all currently-reporting (alive) equity hedge funds launched prior to 2010 were classified as long-living funds, whereas those alive funds launched after May 2013 (i.e., after the Greece default crisis was considered over) but prior to the beginning of 2019 were classified as young funds. Second, two time-series periods were selected: 13 months covering the Covid-19 period (February 2020 – February 2021) and the same duration of 13 months prior to the Covid-19 turbulences (January 2019 – January 2020). Third, all funds were split into “high volatility” and “low volatility” based on the volatility of their returns as reported in the HedgeNordic database. These classifications allowed to compile 8 separate models, the results of which are presented in the Table below.

Table 1. Summary of panel data regression models.

The other rather unusual trend can be seen in the models of high volatility pools – both Young and Long-living equity hedge funds shifted their Small Cap and Emerging Market stock positions into Large Cap long positions reflected with the main Nordic stock indices. Surprisingly, Large Cap indices’ volatility is higher than MSCI Emerging Market index volatility and Small Cap indices’ volatility before Covid-19 period and during it: Large Cap indices’ volatility is 0.0494 and 0.0905 respectively; Small Cap indices’ – 0.0461 – 0.0839 respectively and MSCI Emerging Market index volatility is 0.0467 and 0.0670 respectively. Even if intended as a preventive measure, such shift towards Large Cap positions did not reduce the volatility in returns.

Risks Behind Covid-19 Performance

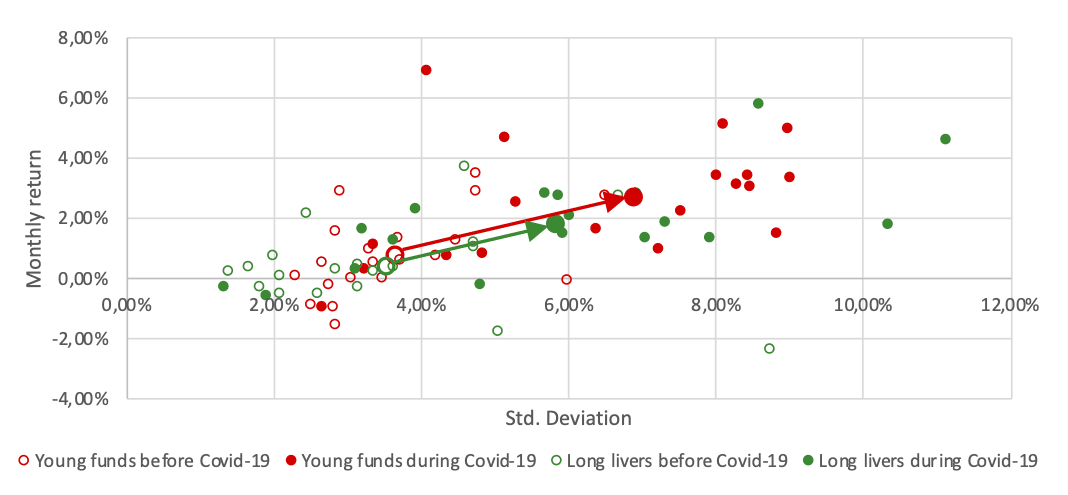

Portfolio theories explain that higher returns stem from higher risks presented in the increased beta indicator, or alpha-generating investment decisions. Looking from the risk-adjusted performance prospective, Covid-19 Sharpe ratios are superior to ones before the Covid-19 period. The scatter in Figure 2 presents the trend of higher return and volatility. The shifts of Long living funds index and Young funds index are surprisingly parallel. Such parallel shift can either confirm the hypothesis of a coherent change in strategies with the beginning of the pandemic or can reflect a certain rigidity in the strategies despite the challenging situation. It is obvious, however, that higher performing and therefore higher risk Long-living and Young funds benefited the most during the Covid-19 period with average annual returns of 35.04% and 41.88%, respectively.

Figure 2. Risk-Return scatter.

However, did this abnormal period cause alpha changes? Alpha indicators presented in the “Nordic hedge fund industry report 2021” were positive during the quiet time periods and during crisis periods, reaching 10.56% per annum for high Sharpe ratio funds. Those alphas were biased as long-term time series models diminish the impact of some of the market risk factors. The annualised crisis alpha of high volatility hedge funds during Covid-19 reached the range of 19.32%-20.52%, nearly double the long-term historical statistics. Crisis alphas of low volatility funds, however, are ambiguous.

I have enquired several investment strategists on such tremendous increase in alpha and to hear their own experience in aligning their alternative investment strategies to cope with Covid-19-like challenges. The replies were a bit surprising: although all appreciated such high return, the sustainability is what they care about the most. And they admitted: it’s hard to beat stock indices using alternative strategies nowadays.

Take Covid-19 Seriously

Like the World Health Organisation warns the public to take the Covid-19 threat very seriously, investors shall also take the “crisis” situation for granted. The Financial Crisis Inquiry Report issued a decade ago and other studies named credit risk concentration, high level of leverage, liquidity risk and concentration of exposures with the same prime brokers as the main reasons behind the “squeezes and losses” experienced by hedge funds.

Banks and other regulated financial institution must perform stress-tests simulating the crisis scenarios and prepare the bank recovery and resolution plans which may also rely on public financial stability recovery measures. Hedge funds are not a subject of recovery and resolution framework for EU credit institutions and investment firms; therefore, as a risk professional, I strongly recommend hedge fund managers to run the severe stress tests and consider recovery and resolution measures by following their own risk appetite and past hedge fund crisis management experience.

Danielius Kolisovas is a researcher with over 15 years of risk management experience holding leading positions in Central Bank of Lithuania, investment bank Finasta and crypto company Blockchain.com. Kolisovas ddvised the Office of the Government of Lithuania and other public institutions. He holds master’s degree in Finance from University of Greenwich and is FRM certified from GARP. Danielius is also PhD candidate in Economics at Mykolas Romeris University where he has been teaching classes on Financial Risk Management and Alternative Investment since 2011.