Stockholm (HedgeNordic) – The global hedge fund industry has been under pressure for years as hedge funds have lagged behind a long-running historic bull market, which forced many managers to call it quits. The Nordic hedge fund universe has not been spared by a great wave of closures either.

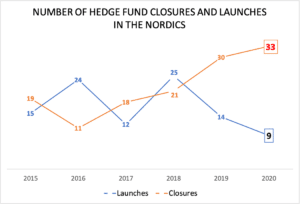

A total of 132 Nordic hedge funds tracked by HedgeNordic closed down or merged into other funds in the past six years from the beginning of 2015 through the end of 2020. The industry recorded more closures than launches in four of the past six years, with 2020 being one of the most painful years in terms of closures after an equally painful 2019. An estimated 33 Nordic hedge funds were liquidated during 2020, up from 30 closures in 2019.

Obituaries

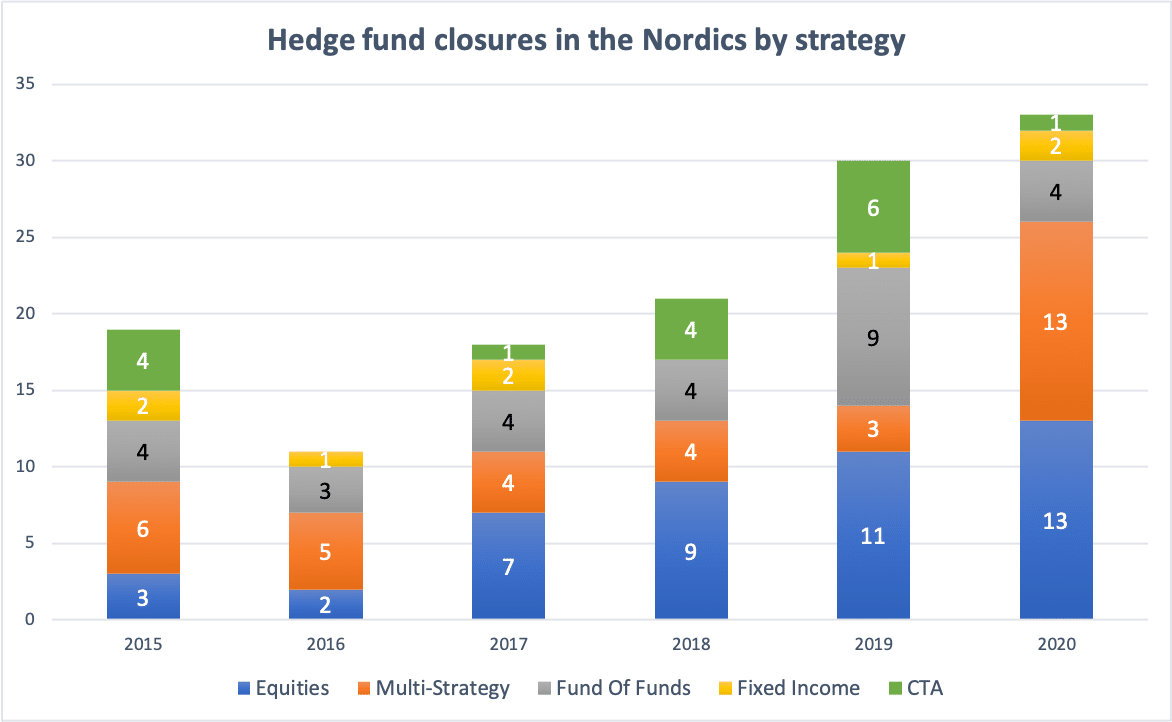

Of the 132 Nordic hedge funds that shut their doors during the past six years, 45 used equity strategies and 35 employed a multi-strategy approach to investing. Over the past six years, equity hedge funds accounted between 35 percent and 40 percent of the Nordic hedge fund industry. The fraction of closures in this strategy group out of the total number of closures ranged between 36.6 percent and 42.9 percent in each of the past four years.

Multi-strategy funds, meanwhile, constituted between 20 percent and 25.5 percent of the industry. The number of closures for this strategy group last year accounted for roughly 39.4 percent of all closures, marking a difficult year for multi-strategy hedge funds in terms of closures. The fraction of closures in this strategy group out of the total number of closures ranged between as low as ten percent to as high as 45.5 percent during five years between 2015 and 2019. Given the relatively high number of Nordic hedge funds categorized as either pursuing equity and multi-strategy approaches to investing, the number of closures in these two strategy groups is not exceptionally high.

Grim Picture for CTAs and Funds of Hedge Funds

The picture becomes grimmer for funds of hedge funds and CTAs. The number of active funds of hedge funds in the Nordic declined in each of the past six years, from 31 funds at the beginning of 2015 to 25 at the end of 2016, 19 at the end of 2018 and only eight funds at the end of 2020. Over the past five years, a total of 28 Nordic funds of hedge funds closed down, with nine of those closures taking place in 2019 alone. An additional four funds of funds closed down last year. The business model of funds of hedge funds has long been challenged because of the double fee-layer and underwhelming performance.

Based on the NHX Fund of Funds, which reflects the aggregate performance of both defunct and up-and-running funds of hedge funds in the Nordics, the group delivered zero returns to investors over the past five years. The survival of the fittest has reduced the number of active funds of hedge funds in the Nordics, with the still up-and-running funds of funds demonstrating an ability to deliver stable and consistent returns over the years. As a group, the six oldest up-and-running members of the NHX Fund of Funds sub-index – out of its eight members – delivered an annualized return of 2.9 percent on average during the past three years and an average Sharpe ratio of 0.58. Their inception-to-date annualized returns and Sharpe ratios stand at 3.6 percent and 0.82, respectively.

The Nordic hedge fund industry is known for housing some of the world’s largest, oldest and best established CTAs, including Lynx, SEB Asset Selection, Estlander & Partners and IPM, whose systematic macro strategy is included in HedgeNordic’s CTA sub-index. Following several years of not-so-great performance for Nordic CTAs, the number of funds using this approach declined from 22 at the beginning of 2015 to 16 at the end of last year. A total of 16 CTAs closed down during the past six years, with the industry recording six closures in 2019 and an additional closure last year.

The Danish-dominated segment of the Nordic hedge fund industry focusing on fixed income has been in a very healthy state for several years, as reflected by performance figures, the number of new launches and the number of closures (or the lack thereof). The fraction of fixed-income hedge funds out of the total number of active funds increased from about 14 percent at the beginning of 2015 to 20 percent at the end of 2019 and 23 percent at the end of last year. The total number of closures in this strategy category amounted to eight in the past six years, with only three closures recorded in the past three years.

Meet the Rookies of 2020

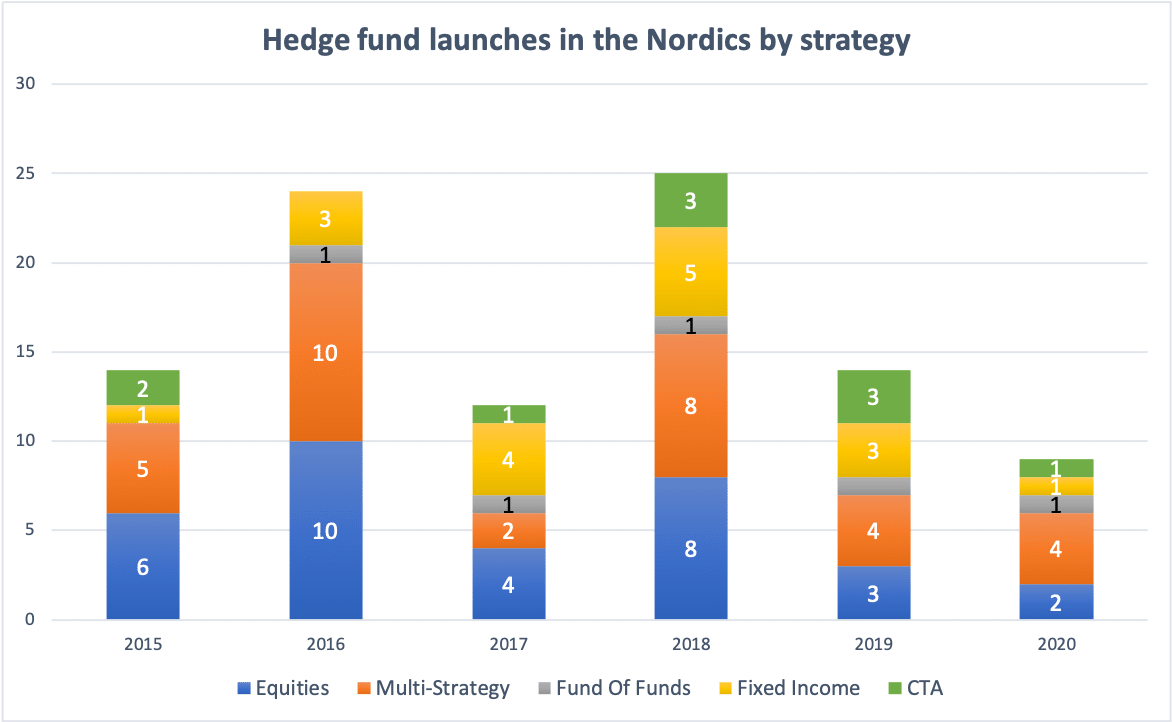

Hedge fund closures outpaced launches in four of the past six years, but there have been new launches in the Nordics too last year. While only nine new hedge funds were launched in 2020, the year with the lowest number of launches in the past six years, a total of 99 funds kicked off operations during that timeframe.

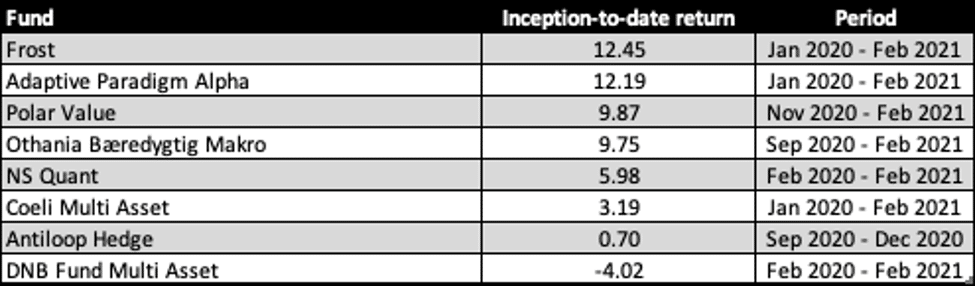

Six of the nine funds launched last year set sail in the first quarter of last year, the busiest in terms of new launches. Relative-value fixed-income hedge fund Frost was launched under the umbrella of Brummer & Partners in January of last year. Paradigm-focused long/short equity fund Adaptive Paradigm Alpha, managed by Linköping-based fund manager Alexander Hyll, and Coeli Multi Asset, a long/short equity fund with an extra feature of global tactical allocation, were both launched during the first month of last year.

DNB’s multi-asset, multi-strategy fund, DNB Fund Multi Asset, and NS Quant, a vehicle launched by Finnish asset manager Northern Star Partners to capture price trends early across several asset classes, were launched during the month of February. Oslo-based multi-strategy hedge fund Polar Multi Asset gained 20.5 percent in its first month of operations in March, and delivered a cumulative return of 6.4 percent through the end of October, when the fund’s strategy was relaunched in a new fund shell with more restrictions and limitations to reduce uncertainty and volatility for investors. Polar Multi Asset’s founders, Ole Christian Presterud and Kent Torbjørnsen, launched Polar Value in November of last year to keep running the same strategy that delivered a gain of almost 21 percent during the month of March.

Anna Svahn co-founded multi-strategy, multi-asset hedge fund Antiloop Hedge in September of last year alongside Martin Sandquist, one of the co-founders of Lynx Asset Management, and Karl-Mikael Syding, former partner and portfolio manager at Brummer & Partners-backed hedge fund Futuris. During the same month, Danish boutique asset manager Othania launched a fund of funds – Othania Bæredygtig Makro – that represents a “one-stop” solution providing access to a wide range of asset classes via investments in its own hedge funds, as well as other hedge funds, alternative investment funds, and exchange-traded funds (ETFs).

Origin and Strategy of New Launches

Swedish hedge funds account for the largest portion of the Nordic Hedge Index, with more than half of existing constituents being based in Sweden or having Swedish origins. Four new Swedish hedge funds joined the Nordic hedge fund arena last year, making this the largest group among the Nordic countries. Two Norwegian, one Danish and one Finnish hedge fund picked up operations last year.

Of last year’s nine new launches, three vehicles employ a multi-strategy approach to investing. Two of the new launches invest mainly in equity markets, and one new vehicle invests in fixed-income markets. One new trend-following CTA and one new fund of funds also joined the Nordic hedge fund universe.

Performance and Size

Most of last year’s rookies had a good first year of operations despite launching during a highly-unusual and volatile economic and market environment. Frost, the relative-value fixed-income hedge fund managed by Martin Larsén and Anders Augusén, had nearly €440 million under management at the end of February this year after a very successful first year. The fund gained 10.6 percent during the entire 2020 and is now up 12.5 percent since inception through the end of February.

Alexander Hyll’s Adaptive Paradigm Alpha also enjoyed a strong first year of operations after gaining 10.3 percent last year and recording positive returns in 13 out of its 14 months of operations. Othania’s fund of funds, Othania Bæredygtig Makro, advanced 8.4 percent in the last four months of 2020 and gained an additional 1.2 percent in the first two months of 2021. Stefan Åsbrink’s Coeli Multi Asset returned 4.7 percent during 2020 after finishing the first quarter in positive territory.

This article featured in HedgeNordic’s 2021 “Nordic Hedge Fund Industry Report.”