By Danielius Kolisovas – “Most hedge funds fail,” says the headline of a Financial Times article back in 2014. With an average life span of about five years and numerous hedge fund closures over the past decade, most hedge funds do fail after all. But what is the secret sauce of the longest-running hedge funds? Thirty-four of the 50 up-and-running Nordic equity hedge funds are older than five years, 27 of them are running for more than seven years, and 22 of them are in business for more than ten years, how do they stay alive for so long?

Insights from my Ph.D. dissertation presented in a forthcoming paper “Determinants of Nordic Hedge Fund Performance,” which focuses on the Nordic hedge fund industry, reveal that the longest-running equity hedge funds from the Nordics from 2005 to mid-2020 share one common characteristic: crisis alpha. There is a trend of declining alpha observed after the financial crisis of 2007-2008, with some researchers claiming that positive alpha is becoming a rare occurrence. My Ph.D. dissertation finds that long-surviving Nordic equity hedge funds generated alpha during both crisis and non-crisis periods, particularly during severe crises.

Long-Running Equity Hedge Funds and Their Alphas

Whereas my research focuses on the entire Nordic hedge fund industry, the insights discussed in this article focus on 27 equity hedge funds with a track record longer than 100 months from 2005 to mid-2020. So how did these 27 equity hedge funds from the Nordics perform during the crises of the past 15 years? How much alpha did these funds deliver?

Before delving into how long-running Nordic equity hedge funds performed over the past 15 years, I feel I need to share more details about the approach for estimating hedge fund alpha. Hedge fund performance, in particular hedge fund alpha, is assessed using the most recognized Fung and Hsieh 8-factor model. This model is best known for incorporating asset-based linear return beta factors, and non-linear smart beta and alternative beta factors representing more exotic, alternative sources of risks such as momentum.

The Fung and Hsieh 8-factor model was initially designed to evaluate risk-adjusted hedge fund performance of U.S.-originating hedge funds, which implies that there are challenges in applying this model to other regions such as the Nordics. To overcome those challenges, I made several tweaks to the original Fung and Hsieh 8-factor model. First, stock and bond market factors, represented by U.S. stock market indexes, U.S. small-cap indexes, U.S. government bond yields and U.S. corporate bond yields were replaced with corresponding Nordic country factors. Second, local currency-denominated returns and factors were converted into U.S. dollar-based returns and factors. Third, alternative factors stemming from research by Fama-French, Capocci, Moskowitz, Adrien Verdelhan, Pástor and Stambaugh were also evaluated to find whether they can improve the model. Lastly, commodity market factors were analyzed to find their contribution to the Nordic hedge fund performance, in particular that of CTAs.

The risk-adjusted performance of Nordic hedge funds was analyzed using panel data regression models on panel data of cross-sectional data representing hedge fund returns and country-specific risk factors in the same time-series dimension. The time-series were not split into smaller specific periods, so the results reflect long-term performance measures.

Show me the alpha

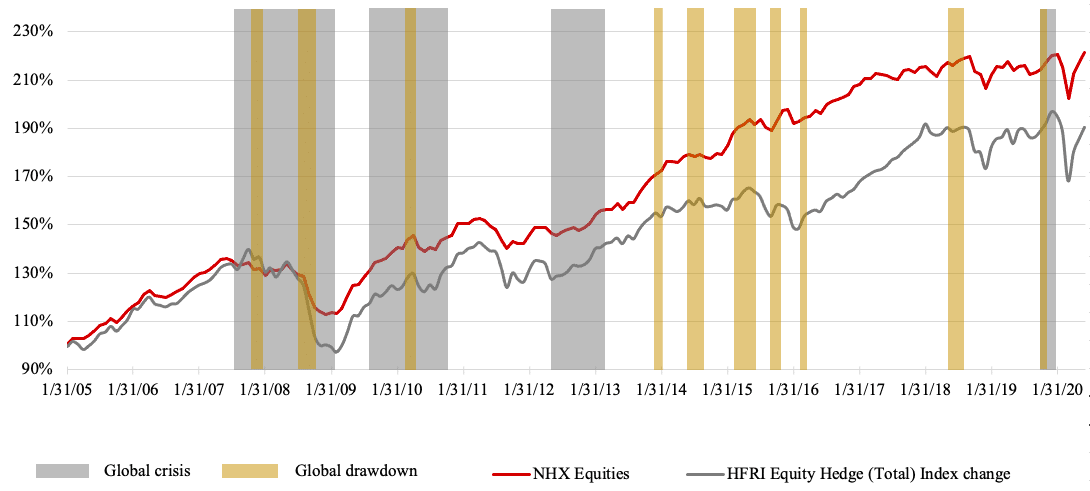

The grey areas in the figure below highlight the following crises: the global financial crisis that started in 2007, the European debt crisis of 2010, its continuation with Greece defaulting on an IMF loan in 2012, and the Covid-19 crisis in early 2020.

Figure 1. Indices performance and crisis periods

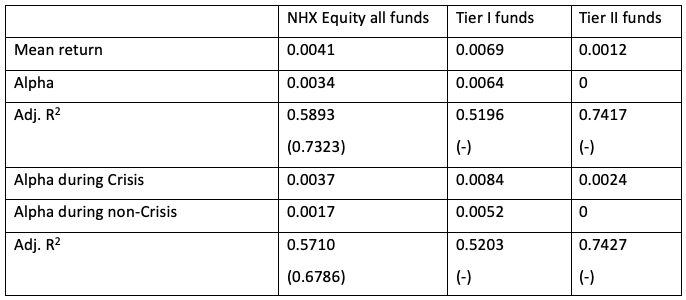

As shown in the table below, the 27 long-running equity hedge funds delivered an equally-weighted monthly alpha of 0.34 percent, translating into an annualized alpha of 4.16 percent. The monthly alpha reaches 0.37 percent during crisis periods, compared to 0.17 percent per month during non-crisis periods.

More interestingly, when splitting the group into Tier I, featuring funds with higher-than-average Sharpe ratios, and Tier II with lower Sharpe ratios, we observe that the weaker-performing pool of hedge funds, on average, delivers no alpha during non-crisis periods. The Tier II funds, however, deliver a monthly alpha of 0.24 percent during crisis periods. The stronger-performing funds provide alpha both during crisis and non-crisis periods. The Tier I funds generated monthly alpha of 0.84 percent during crisis periods, translating into an annualized alpha of 10.56 percent. In non-crisis periods, the Tier I funds deliver a monthly alpha of 0.17 percent.

Table 1. Summary of multiple regression models

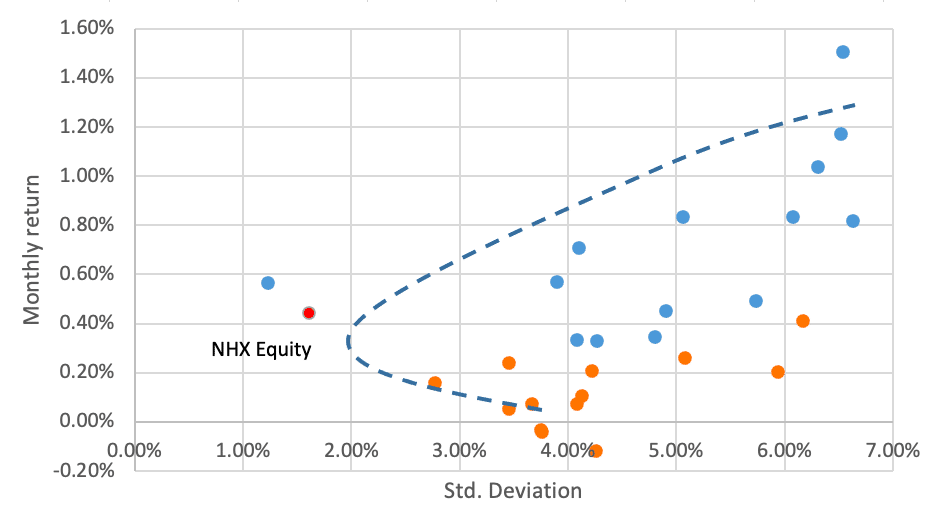

The figure below presents the risk-return distribution of Tier I and Tier II hedge funds, as well as the NHX equity sub-index, which is located further “north-west” from the supposed efficient frontier of Harry Markowitz’s modern portfolio theory (represented with the dashed line). This can be explained by the survivorship bias reflected in the data used for this study, as not all equity hedge funds were included in the study.

What Drives the Alpha?

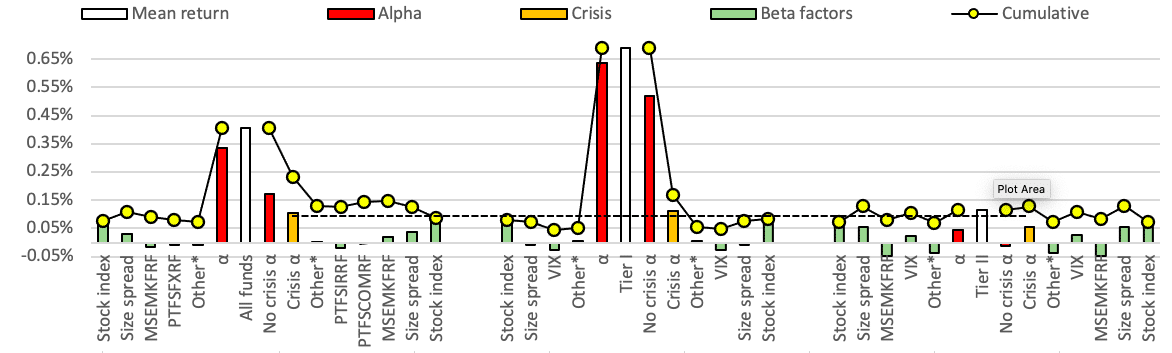

Pricing models normally utilize absolute statistical coefficients, which do not disclose how much each risk factor contributes to the modelled hedge fund return. The “elasticity at means” method allows presenting scaled coefficients, which show how much a given risk factor contributes to the long-term hedge fund performance.

The scaled graph below presents alpha’s proportion of the mean return and the relatively insignificant contribution from various market beta risk factors (on the left side modelled prior applying crisis factor and, on the right, with applied crisis factor). This somewhat contradicts recent studies showing that hedge fund alpha has disappeared altogether. We need to bear in mind that such long duration time series model diminishes the contribution from smart and alternative beta factors, which fund managers can have different exposures to depending on market conditions, and they can be frequently adjusted depending on the market situation.

Figure 3. Scaled factors

Conclusions

According to a wide body of research, hedge fund alpha may have sharply deteriorated in the decade following the financial crisis. But the hedge funds that survived the longest over the past 15 years did deliver significant alpha. Insights from my research reveal that the portfolio of 27 of some of the longest-running Nordic equity hedge funds delivered significant average alpha both in crisis and non-crisis periods. More importantly, the research presents the positive impact of crises on the long-term alpha. This contradicts some of the researches stating the opposite.

On the one hand, crisis periods are well-known for causing investors to panic and prompt closing some positions at higher discounts. On the other hand, highly skilled fund managers with solid crisis management experience are taking advantage of the low prices, applying more exotic strategies, and delivering higher returns. All in all, this article presents evidence that long-surviving equity hedge funds from the Nordics generated significant average alpha and crisis alpha during the past 15 years. However, individually the excess returns (alpha) of the hedge funds are more widespread.

Other findings from the forthcoming paper “Determinants of Nordic hedge fund performance”:

- In all NHX sub-strategies (i.e., Equities, Fixed income, CTA, Multi-strategy and Fund of funds), there is a consistent trend of increasing alpha during crisis periods relative to quieter times.

- The impact of tightening regulatory regimes by implementing the hedge fund-specific AIFMD directive and by changing of regulatory climate measured with World Bank Regulatory Quality Indicators is negative and opposite to the crisis. This supports the conclusion that regulation makes hedge funds more risk-averse, thereby, lowering the excessive return (alpha).

Danielius Kolisovas is a researcher with over 15 years of risk management experience holding leading positions in Central Bank of Lithuania, investment bank Finasta and crypto company Blockchain.com. Kolisovas ddvised the Office of the Government of Lithuania and other public institutions. He holds master’s degree in Finance from University of Greenwich and is FRM certified from GARP. Danielius is also PhD candidate in Economics at Mykolas Romeris University where he has been teaching classes on Financial Risk Management and Alternative Investment since 2011.