By Svein Aage Aanes, Head of Fixed Income and FX at DNB Asset Management – 2020 was a year for the history books in many respects. The Nordic High Yield market was no exception with credit spreads and returns showing the largest intra-year swings in the history of the market. The massive sell-off that we saw in all risk markets in March was exacerbated by some special factors in the Nordic credit markets.

In Norway the massive weakening and extreme volatility of the NOK (NOK weakened by more than 20% against EUR in a couple of weeks) led to large needs for generating cash as collateral in currency hedging contracts. The effect was an overshoot in credit spreads relative to other markets in this period. In Sweden there were massive outflows from credit funds resulting in 35 Swedish credit funds closing for redemption from the middle of March.

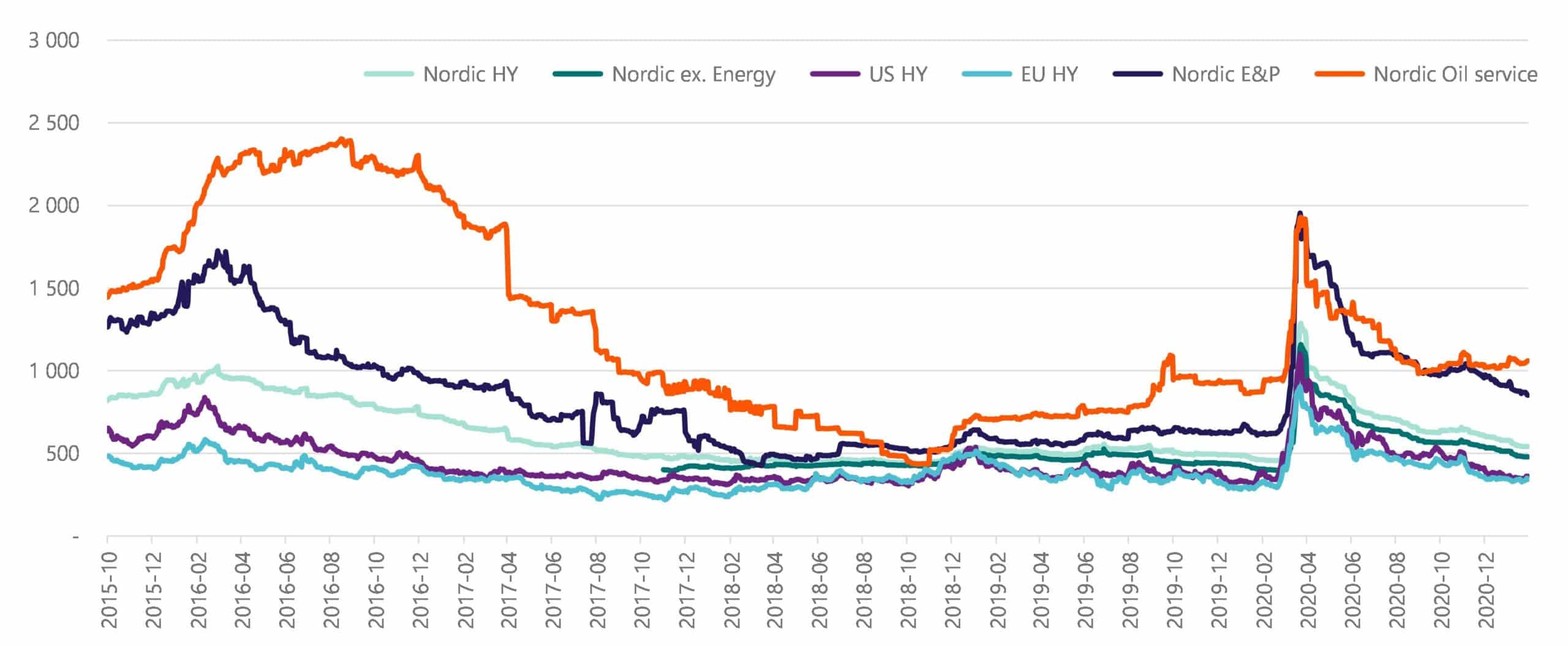

Credit spread (bp) development in international and Nordic high yield markets:

As the credit markets in the Nordic countries teetered on the edge the central banks came up with targeted solutions for the respective problems in market functioning. In Sweden, the chosen solution was the same as in the US and Europe, including credit in the already existing QE programs. This decision was taken by the Swedish central bank in June and they now have in place a relatively small program of 10 bn. SEK for buying credit bonds with the stated aim of establishing a presence in the credit market so that the program can swiftly be ramped up if the need arises. In Norway, which has no established QE program, the solution was that the central bank, for the first time since 1998, intervened in the FX market. The intervention was quite small and had the stated aim of reducing excess volatility. It was successful in that it restored market confidence and ended the vicious NOK weakening – credit spread widening cycle.

In our view the experience of March 2020 and, more importantly, the Nordic central banks’ experience of this period taught some lessons that will be remembered. Thus, we think that the risk of a similar (close to) total meltdown in the future has been reduced as the instruments employed by the central banks in March 2020 are now sharpened and ready in the (hopefully unlikely) event that a similar situation should arise.

We think that the risk of a similar (close to) total meltdown in the future has been reduced as the instruments employed by the central banks in March 2020 are now sharpened and ready in the (hopefully unlikely) event that a similar situation should arise.

Turning to the latter half of 2020 we saw a continued spread tightening in the Nordic high yield market just as in high yield markets elsewhere but to a somewhat smaller extent. Particularly in Q4 the spread tightening in the Nordic market was not able to keep up with developments in high yield markets in the Eurozone and the US. Parts of the reasons for this development might be that mutual fund flows in the Nordic high yield market was not particularly strong in 2020. It was by no means catastrophic but total inflows were barely positive for the year.

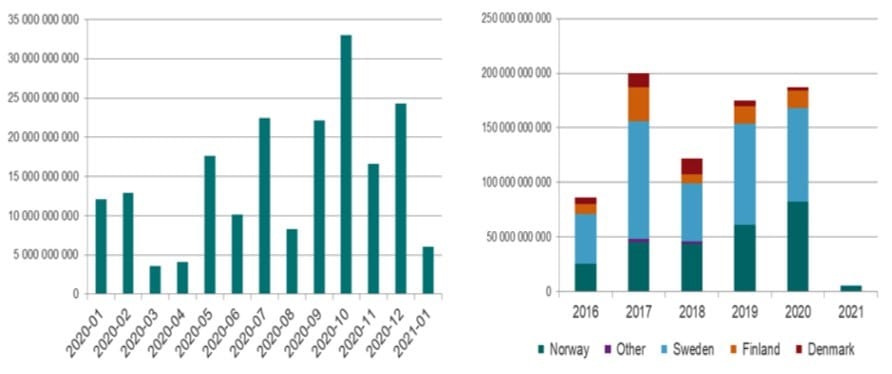

Norwegian high yield fund flows in 2020:

On the other hand, after a naturally quite weak first half of 2020 when it comes to new issuance we were back to business as usual in the second half of the year. The combination of relatively mediocre inflows and large supply in H2 2020 likely contributed to keep spread tightening in check.

Nordic high yield issuance in 2020 and historically:

We think these developments create an interesting starting point for 2021 and we are quite positive to the outlook for Nordic high yield for this year. Clearly, the outlook is dependent on the overall situation in credit markets going forward but given our main scenario which is based on economies opening up in the second half of the year on the back of vaccine roll-out and continued central bank support throughout 2021 we think credit markets can perform reasonably well even in the face of relatively tight spreads in many parts of the credit market. In this scenario Nordic high yield provides a pocket where spreads have not fully returned to their pre-crisis low and where the opportunity might still exist for some extra return.

This article was first published on DNBAM.com.

Disclaimer:

The information in this document is not binding. Statements in this document should not be understood as an offer, recommendation or solicitation to invest in or sell UCITS funds, hedge funds, securities or other products offered by DNB Asset Management or any other company within DNB Group or any other financial institution.

All information reflects the current assessment of DNB Asset Management, which is subject to change without notice. DNB Asset Management does not guarantee the accuracy and completeness of the information. This information does not take into account the individual investment objectives, personal financial situation or specific requirements of an investor. DNB Asset Management does not accept any responsibility for losses incurred on investments made on the basis of this information. Our general terms and conditions can be found on our website www.dnbam.com.

Picture courtesy of DNB Asset Management. Picture by Stig B. Fiksdal.