Stockholm (HedgeNordic) – Formuepleje’s Penta strategy, incepted in 1995, can leverage up to 500% and typically has around 400% gross exposure. The portfolio was comprised of 332% bonds, 127% global equities, and 12% equity market neutral, as of October 2020.

Yet its volatility, drawdown, and value at risk metrics are below that of an unleveraged portfolio 100% invested in global equities, and this is by design. “One of the risk management constraints is that forecast risk measures over 36 months indicate a probability of loss no higher than they would be for an unleveraged global equity portfolio. The simulation is based on a standard methodology of normalized statistical distributions, assuming a normal distribution”, says Søren Astrup (pictured), Director.

“One of the risk management constraints is that forecast risk measures over 36 months indicate a probability of loss no higher than they would be for an unleveraged global equity portfolio.”

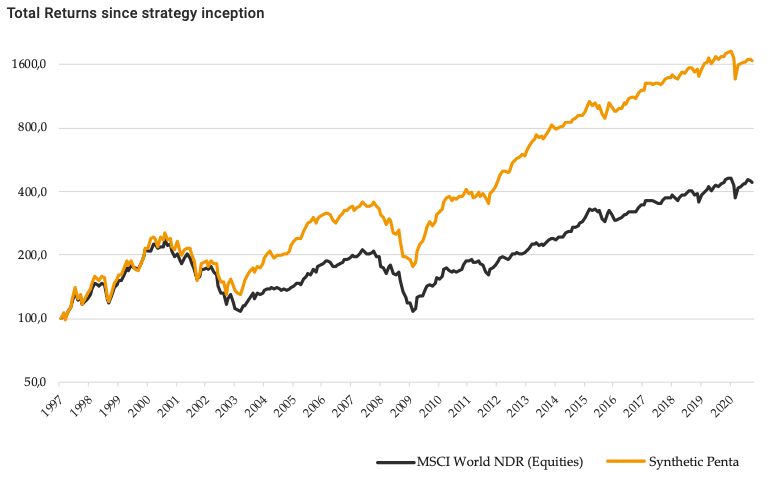

Historically, Penta has generated higher returns and Sharpe ratio than its benchmark of global equities. The simulated performance since 1997 would have been up by over 1500%, compared with global equities up by around 300% over the same period. This demonstrates the magic of compounding over 23 years. Global equities have annualized at around 6.4% while the synthetic Penta profile has annualised at 12.6%. Penta has also provided a smoother ride: the Sharpe ratio over this period has been 0.52 for synthetic Penta, versus 0.26 for global equities. (A simulation is used due to a change of approach after 2008, when Swiss Franc leverage caused some losses. The risk model has since been modified).

Volatility on Penta has been slightly higher than on unleveraged equities, but importantly downside risk, as measured by Value at Risk and Conditional Value at Risk are lower.

Diversification

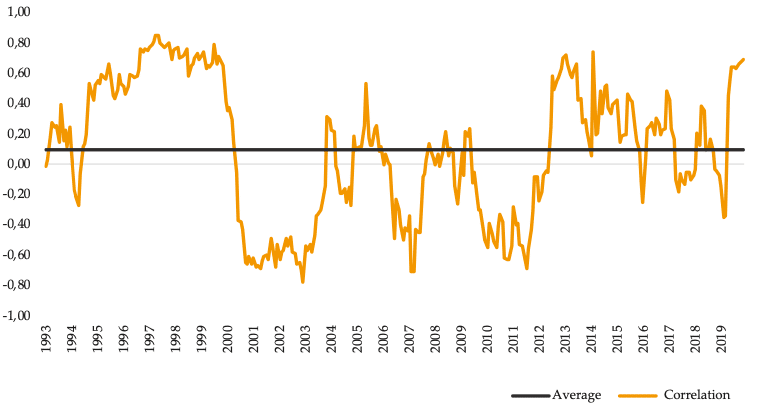

One reason why Penta has lower downside risk than unleveraged equities is the low correlation between the equity and bond strategies – and their near zero correlation with the market neutral sleeve.

Historically the correlations have ranged between roughly +25% and -25% though they can sometimes be outside this range. “During the Coronavirus crisis, in March 2020, there were periods when correlations spiked up to 0.7. Recently in October 2020, correlations between the two have been slightly negative. We take a quarterly look at correlations and form a view on their future behaviour”, says Astrup.

Skewness

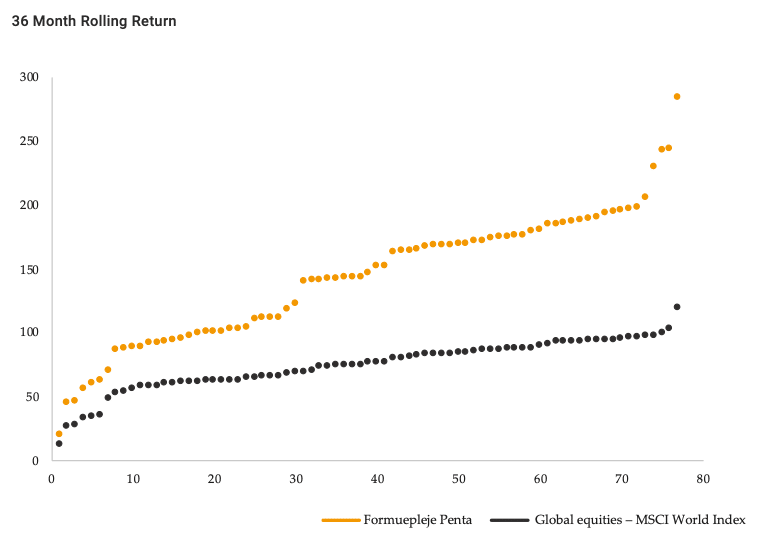

Another reason for Penta showing lower downside risk has been its pattern of returns, which has more positive periods and fewer negative periods than do global equities, as shown below.

Hedging and Constraints

The concept of leveraging relatively low volatility bonds may sound similar to risk parity, but whereas risk parity tends to be long only this strategy has some long/short exposures.

Interest rate duration on the bonds, which are mainly government and mortgage bonds in Sweden and Denmark, has averaged around 2.47, and this is multiplied by portfolio leverage of 3.25 to get overall duration of near 8. Penta does however have freedom to run slightly negative interest rate duration, but is not doing so in 2020. Though shorting bonds with negative yields might generate some degree of positive carry, Formuepleje’s ability to borrow at repo rates below the negative yields on bonds, means that it can extract positive carry from leveraged long exposure to bonds with negative yields.

“The market neutral allocation does not change the volatility much, but at the margin it stabilizes the risk and enhances the Sharpe ratio.”

There is also an equity market neutral allocation, which is no more than 13% of the overall equity exposure, which maxes out beta-adjusted equity exposure of 130%. “The market neutral allocation does not change the volatility much, but at the margin it stabilizes the risk and enhances the Sharpe ratio”, says Astrup. The market neutral strategy is a systematic, two times levered approach.

A Value Tilt in Equity Factor Exposures

Equity beta has tended to be close to 1, though it is slightly below that in October 2020 because Formuepleje is somewhat underweight of growth stocks and overweight of value stocks. “We do expect some sector rotation when conditions normalize, so we may miss out on momentum stocks. Valuations for technology stocks seem too high, but we are not making an aggressive tilt towards any factor. It is broadly factor neutral. Back in the year 2000, we missed out on some of the last leg of the bull market because we could not live with the high valuations”, explains Astrup.

It seems that Formuepleje has accurately judged that the growth versus value divergence was extremely extended. In the week of November 9th, 2020, equity markets saw some of the most violent factor rotation from momentum to value ever recorded, with a performance gap as high as 20% between the two.

Academic Foundations

Behavioural finance might go some way towards explaining the extreme enthusiasm for growth and hatred of value in equity markets, but the core academic foundations for the Penta strategy date back to the 1950s, specifically Harry Markowitz’s 1952 paper in the Journal of Finance. His Modern Portfolio Theory made the basic case for combining lowly correlated assets, and he received the Nobel Memorial Prize for Economic Sciences for this in 1990. Markowitz argued investors should optimize returns relative to volatility, and let the efficient frontier be their guiding star.

Tobin’s risk separation theory built on this foundation, and argued that the optimal portfolio decision should be separated from the decision about how much cash to hold or borrow. Investors’ appetite for leverage depends on their degree of risk aversion.

These theories provide the top down arguments for diversification and careful use of leverage, but the academics assumed that investors would be buying the entire market. Formuepleje is not simply combining betas but is seeking to add alpha through its extensive experience of forming macro views on government bonds, interest rate moves, yield curves, and mortgage prepayment rates, primarily for Danish and Swedish government and mortgage bonds. And Formuepleje is also seeking to add alpha to equity markets. The purest form of this is the equity market neutral strategy, while the long global equities strategy also aims to outperform a passive approach.

This article featured in HedgeNordic’s report “True Diversifiers.”