By Melanie Brooks, CARN Capital – Diverging strategies and confusing terminology regarding sustainable investment increase the risk for greenwashing and, in the worst case, misallocation of capital. For CARN, ethical exclusions and ESG tilts on their own are not enough to achieve sustainability. We have therefore chosen an alternative approach, investing actively for a sustainable future.

After decades of occupying a niche corner in the world of finance, sustainable investment is going mainstream. 2019 appears to have been a pivotal year in this transition, with over $20 billion of new money flowing into strategies related to ESG and sustainability more broadly, according to data from Morningstar.

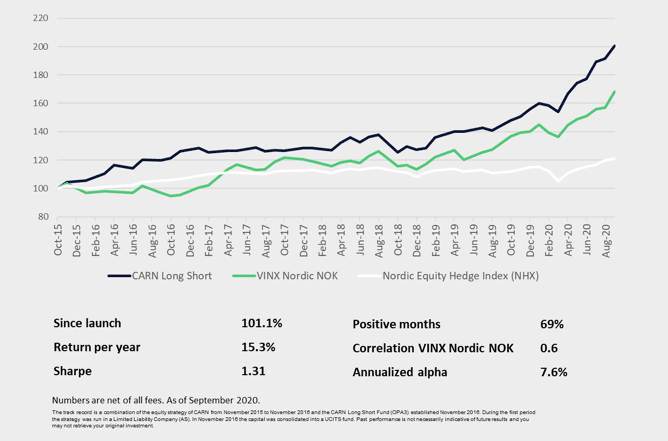

Driven by a growing awareness of sustainability issues, institutional and retail investors alike are increasingly interested in investing in companies they perceive to be part of the solution to global challenges such as climate change. There is also a realization that investing sustainably does not have to mean sacrificing returns, and that a sophisticated and well-executed sustainable investment strategy can create significant value for investors. CARN Capital’s Long Short fund is a great example of this. With sustainability at the core of our investment strategy, we have delivered 15.3% in annualized returns since the fund was started in 2015.

Growth in demand from sustainability-minded investors has resulted in an explosion in the availability of new or rebranded funds marketed by fund managers. According to Morningstar, more than 500 actively managed funds added high-level ESG language to their prospectuses in 2019. However, this appears to be due, at least in part, to otherwise conventionally managed funds saying that they now consider ESG factors, without sustainability being central to their investment strategy or decision making.

This increased interest in investing sustainably is undoubtedly positive as finance has an important role to play in the transition to a more sustainable and equitable economy. However, the devil is in the details. Sustainable Investment is an umbrella term covering a range of strategies with vastly different approaches and outcomes. This has resulted in terms with very different meanings being used interchangeably, such as ESG being confused with sustainability or even used as a synonym for cleantech. This unfortunate development can result in confusion at best and a misallocation of capital at worst. Investors need to understand the characteristics and limitations of various approaches. This will facilitate investments into sustainable solutions and avoid investors being disappointed by what they find in portfolios marketed as sustainable but that in practice fall short of this label.

“This increased interest in investing sustainably is undoubtedly positive as finance has an important role to play in the transition to a more sustainable and equitable economy.”

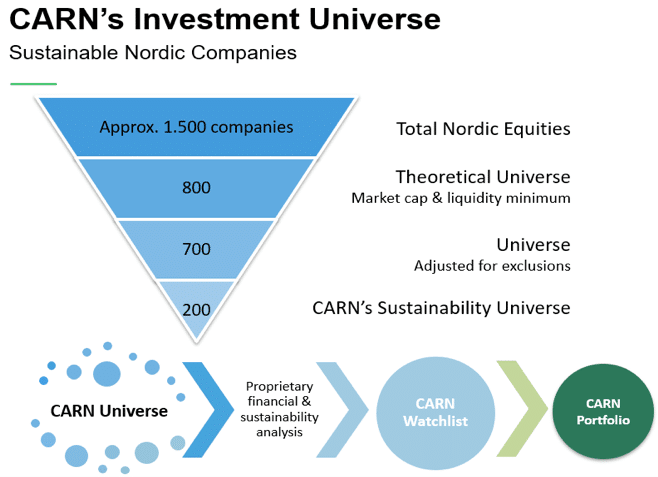

We’d like to help provide some clarity as to the main characteristics of the most common approaches to sustainable investment in listed equities today, and associated terminology. The figure below illustrates at a high level the spectrum of approaches often grouped under the umbrella of sustainable investment. It is CARN’s view that no single approach is sufficient to ensure sustainability and profitability on its own, and we have therefore chosen to incorporate elements of the full range of approaches in our investment strategy.

The first approach shown is exclusion, also commonly referred to as negative screening. This approach has a long history and entails excluding companies deemed unethical or otherwise unacceptable from the investment universe. It is relatively straightforward to implement due to transparent rules and thresholds rooted in commonly accepted definitions of unacceptable products or behavior. An example of this is excluding companies that produce tobacco or certain types of weapons, or that have been found in breach of ethical norms such as those related to human rights. The Guidelines for Observation and Exclusion from the Norwegian Sovereign Wealth Fund are a good reference on ethical exclusions.

On the other end of the spectrum is thematic and impact investing, where the goal of the strategy is to invest more or exclusively in companies that create a measurably positive impact on society and/or the environment, in addition to delivering financial returns. An example of this would be targeted investments in renewable energy. The main difference between the approaches is that the return requirements may differ. Thematic investing aims to make strong or even superior financial returns while investing in sectors, companies and technologies that help solve sustainability challenges. Impact investing on the other hand usually places more emphasis on measurably positive outcomes for society and/or the environment, with secondary emphasis or even reduced expectations on financial returns.

While now ubiquitous, ESG as a term and concept is a relative newcomer to the scene, having been engrained in the Principles of the UN PRI in 2006. ESG is an umbrella term and covers all environmental, social and governance considerations that companies encounter in their business activities. ESG relates primarily to processes in a company, rather than the products or services it provides. In this way it is different from thematic and impact investing.

One consequence of the rise of ESG has been a shift in focus to relative rather than absolute sustainability performance at the company level. The scoring of companies on ESG indicators in relation to their industry peers means that companies can receive positive ESG ratings on a relative basis, even if in absolute terms they generate negative externalities to the environment or society. To illustrate, a tobacco manufacturer or thermal coal producer can score relatively well on ESG if they have well-functioning boards, treat their employees well and reduce inputs of water and energy in their production processes.

Integrating ESG considerations in company analysis and portfolio construction can encourage companies to improve on ESG in order to attract capital. There is also some evidence that companies who are better at managing material ESG issues relative to their industry peers may also be characterized by lower earnings volatility and higher returns than peers with poor ESG performance.

“Integrating ESG considerations in company analysis and portfolio construction can encourage companies to improve on ESG in order to attract capital.”

Excluding unethical companies and assessing ESG on a relative basis are both good places to start when embarking on a process to invest more sustainably. Moreover, these approaches are not mutually exclusive and are often combined. We would argue though that as investors we cannot exclude our way to a sustainable future, nor can we get there by assessing relative ESG performance in unsustainable industries. Investing in a way that is truly aligned with sustainable development requires an approach that channels capital to companies that are sustainable both in terms of how they operate and in terms of the impact their products and services have on society and the environment.

This is the CARN way. We do not provide capital to companies or industries that inherently undermine sustainable development. We invest in companies whose business models, products and services are aligned with economic, environmental, and social sustainability, concepts which are also the basis of the UN Sustainable Development Goals (SDGs). Moreover, we expect companies we invest in to have good ESG practices embedded in their processes, including how they treat their employees, manage natural resources and work on behalf of shareholders and other stakeholders.

“Our sustainability focus is integrated into each step of our investment process, from defining our investment universe to carrying out company analysis, portfolio construction and active ownership.”

Our sustainability focus is integrated into each step of our investment process, from defining our investment universe to carrying out company analysis, portfolio construction and active ownership. We believe this is the best way to protect and grow our investors’ capital and to contribute to sustainable development.

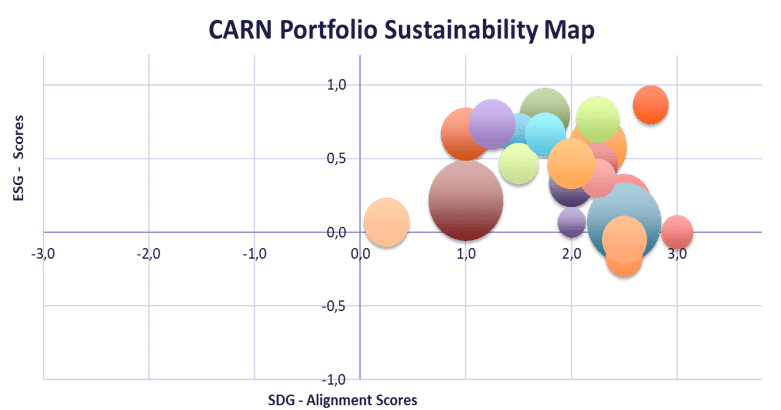

Our approach has resulted in strong risk-adjusted financial returns and a portfolio that scores high both in terms of ESG performance relative to industry peers and sustainability, measured in terms of alignment with the UN SDGs.

This article featured in HedgeNordic’s report “ESG in Alternative Investments.”