London (HedgeNordic) -In the past few months, investors have been scratching their heads perhaps more than ever trying to answer the question ‘where to now?’ in terms of investments in order to find that exclusive alpha.

Altamar Capital Partners, the Madrid-based private assets specialist, believe they have at least a part of the answer, namely GP-led deals in the less crowded and less competitive lower-market secondaries space.

These strategies aim to provide a tool for GPs and investors to manage their liquidity and are more transaction-driven investments often involving resetting of terms. As the portfolios tend to be smaller, they lend themselves to a more bottom up approach, more akin to direct private-equity investments, providing that the right incentives and alignment of interests are in place for all parties involved.

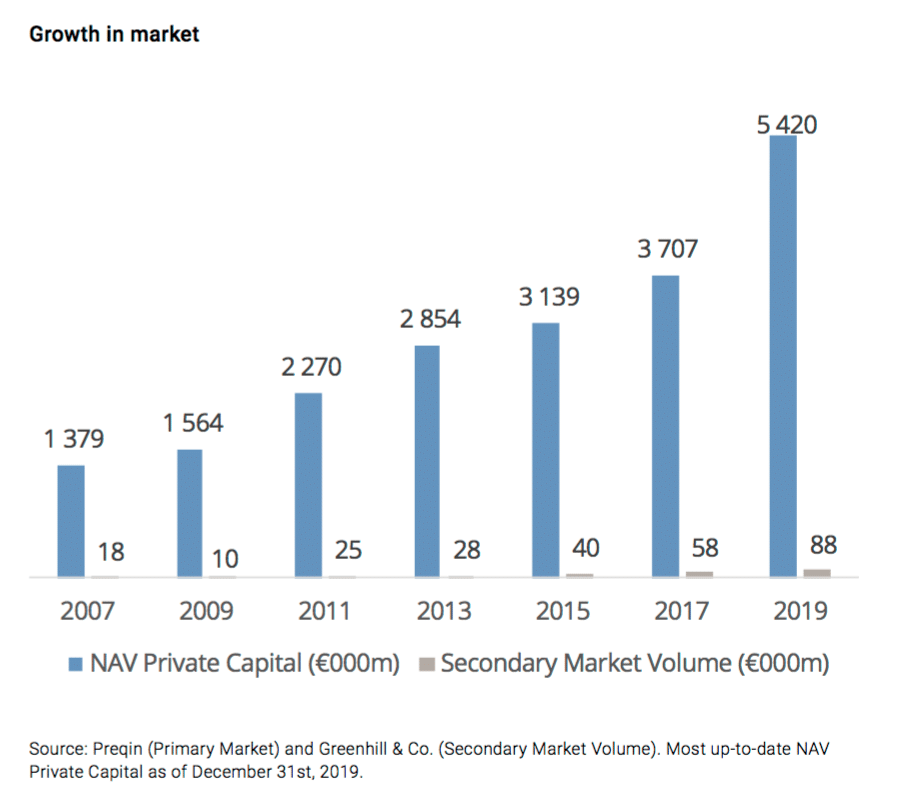

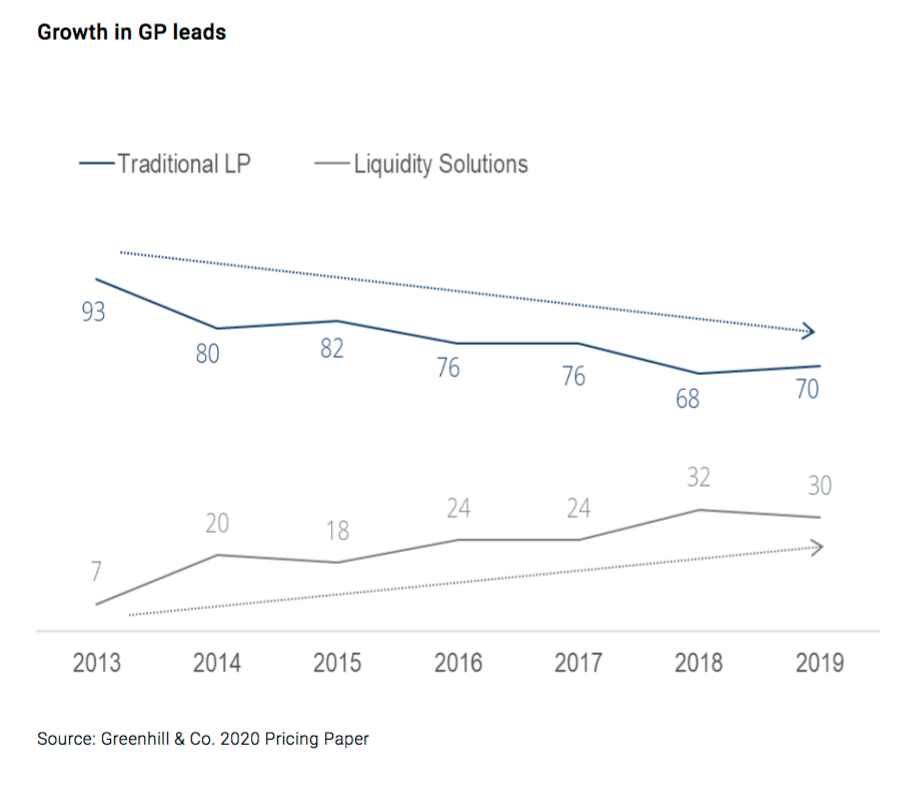

Miguel Zurita (pictured), Managing Partner, Head & co-CIO of Private Equity at Altamar, said that there is now an ideal opportunity in this segment as there has been a healthy and balanced growth in the market for some time. The overall secondaries market has grown from USD18bn in 2007 to USD88bn in 2019. The GP led segment was pretty much non-existent in 2007 but now represents approximately one third of transactions today. “In addition, there has been a shift from the larger plain vanilla Limited Partner (LP) trade transactions to more complex General Partner (GP)-led liquidity solutions. You have to keep in mind that increased complexity does not necessarily equal increased risk as long as the complexity is identifiable and terms and incentives can be negotiated.“

“Risk mitigation and capital preservation are central facts to this strategy for us, targeting low leverage at the asset level and zero transaction-level leverage”, he added.

“The growth in private equity in general is set to continue as the asset base grows and as the secondaries market also expands, this smaller niche area has emerged, as most players go for the larger segment. Large funds make up the bulk of the secondaries market but some 20% of transaction volume comes from small/mid-sized funds”, he noted.

In the large plain vanilla secondaries market a buyer simply buys the stake from the selling LP at a discount but with the same financial terms as the original LP, with no room to renegotiate. These transactions typically involve larger portfolios with a vast number of underlying companies. If the buyer is a secondaries fund, often leverage is put on the transaction, a good way of getting exposure to the beta of the secondaries market. Historically these types of deals had a ‘winner’ and a ‘loser’ and this stigma lives on as often the stake was sold by an LP in distress, making the discount the driver of the return.

Zurita further explained that the smaller, targeted alpha-driven transactions with a focus on proprietary or directly negotiated transactions are also attractive as returns are not dependent on leverage. “The risk-return profile is compelling for GP-led liquidity solutions with no leverage as they typically outperform traditional secondary portfolios with leverage”, Zurita said.

“Returns remain attractive throughout the cycle with strong cash-flow dynamics and j-curve mitigation. Other positive attributes include faster visibility on de-risking through liquidity as well as existing GP relationship and information advantage,” he said, adding while uncertainties remain, the higher visibility in the small to mid-sized secondaries market, offers advantages.

Zurita also said that of course things can still go wrong as these deals typically involve fewer assets i.e. portfolios are more concentrated and volatile. The volatility and dispersion of returns, however, is also the source for alpha, he added.

Zurita said that the beauty with the liquidity solutions is that global trends and risks such as trade wars, political instability or indeed a global pandemic already priced in and you know what you are buying as it is the secondary market rather than a black pool.

He also said that while there is a slow-down in new commitments, investors are seeing opportunities in existing commitments, Altamar is agnostic as to which regions it looks at and takes an opportunistic approach. Altamar sees specific industries doing particularly well going forward such as telecoms, software, gaming as well as selected healthcare assets which have continued to boom during COVID-19.

Furthermore, current market dislocation has created greater opportunities in secondaries and according to a survey by Evercore some 44% of sponsors may consider liquidity solutions transactions to allow more time to create value in their portfolio. “GPs are in a stronger-than-ever position to maximise their assets and buy time as well as get additional capital,” Zurita said.

“In a post-Covid-19 environment there are buyer tailwinds and an enormous potential for revaluation, that should rationalise entry points and allow buyers to catch the upswing”, he said. He explained that there are also opportunities for offensive plays and the environment for executing buy-and-build strategies for quality platforms is also favourable, noting that Altamar is well positioned to take advantage of the growth because of the depth and breath of its platform.

Zurita also said that GP motivations are shifting as the uncertainties of post-Covid 19 continue which is also pushing up transaction volumes. For instance, managers nearing the end of fund terms which were planned for liquidity in 2020/2021 will need to explore and consider other options. In addition, it is expected that fund raising in the traditional primary space will continue to be challenging in the near future.

Zurita also warned that not all liquidity solutions are alike which is why making sure that there is true alignment of interest among the parties is key.

’You have to examine the motivations of the GPs in order to avoid ‘zombies’ as well as acquire quality assets at a discount to intrinsic value. The complexity of the deals requires sophisticated and knowledgeable buyers therefore relationships are vital for finding the best opportunities,” he said. Altamar only closed less than 10% of the liquidity solutions it evaluated in 2019, proving that being picky is a must.

At Altamar, its executive partners, shareholders and team have committed over €230m in Altamar’s programmes. Zurita believes that another advantage Altamar has over its competitors, in addition to its longstanding primary relationships, access to quality managers and seasoned private equity professionals with a multidisciplinary approach to investment, is the firm’s infrastructure such as the proprietary database tracking 400+ GPs and 5000+ private equity investments.

An area which private equity firms have been criticised for is their tardiness in getting on board the ESG train. Zurita said: “We have a strong team in charge of improving our ESG policies alongside three lines; responsible investment (we are signatories of UNPRI with A+ score in all sections reported), management of our own company (diversity, low carbon impact among other factors) as well as in philanthropy as we set up the Altamar foundation some years ago.”

“In practical terms the review of our ESG policies is part of our due diligence and in the past we have rejected investments for ESG reasons (such as plastics manufacturers or gambling ) and in fact one of the recent steps we have taken is to prepare a list of excluded sectors such as pornography, weapons among others. This is a continuous project and will be extended over time. A very positive side effect of this for a firm like ours with a strong culture and where talent is our most important asset, is that having a strong focus on ESG with full engagement from our team members allows us to recruit and retain great professionals,” he concluded.