By Michael Zbinden of Crypto Fund AG: In 2009 bitcoin came into existence with Satoshi Nakamoto (or someone calling himself that) mining the so-called genesis block of bitcoin, laying the groundwork for cryptocurrencies based on blockchain technology, and later projects with similar technology. Moving ahead to 2017, traditional big players began entering the market, including the CME, the world’s largest futures exchange, as it announced its own cash-settled bitcoin futures contracts.

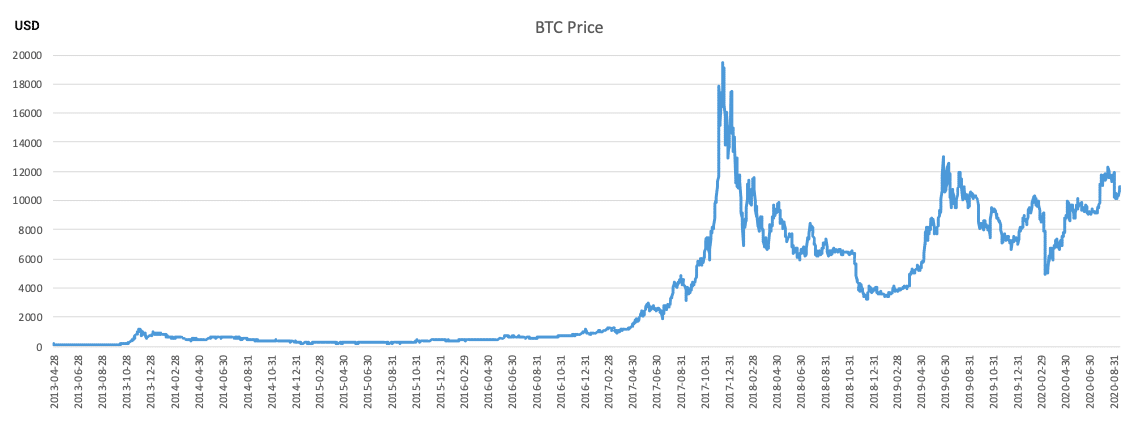

In anticipation of institutional money flowing into the crypto market, bitcoin traded higher and higher and culminated at the level of around 20,000 USD. Many crypto projects profited from the hype, generating massive amounts of money by creating new cryptocurrencies and selling the virtual coins in so-called initial coin offerings (ICOs). Some projects are still in development and are now delivering first results; other projects have completely lost traction.

From there, prices for bitcoin varied greatly. At the end of 2018, bitcoin traded slightly above 3,000 USD, in mid-2019 it traded slightly below 14,000 USD again, one year later it touched 4,000 USD, and the bitcoin price has recovered to 10,500 USD since then. In other words, the volatility of bitcoin – and crypto assets in general – is very high. Looking at the statistics, bitcoin’s long- term correlation with traditional asset classes is low – with periods of high positive correlation and periods of high negative correlations.

Basic Understanding of a Blockchain

In its basic setup, a blockchain can be equated to a distributed database that is continuously shared across a network of computers. The internet, as a base carrier for blockchains, has enabled this technology: for public blockchains, there is no restriction of access and everyone can join or leave the network independently.

A blockchain’s basic operational mechanisms include:

- Participating computers must be in sync with all other computers of the same network to make sure that no malicious records are added to the database and the current state can be verified at all times by the participants.

- Records that the network accepts are collected and aggregated in a data block.

- Each block is appended to the blockchain. The network of computers validates the blocks: computers participating in the network compete against each other and the fastest computer to validate it can append a block.

- The computer that appends the next block receives the so-called block reward, a well- defined amount of newly “minted” coins. To find the next block, the target steering parameter is the time (resulting in a constant generation of blocks, e.g. every 10 minutes).

- The size of the computing network is a function of the price (higher prices increase profitability and the incentive to participate) and not a function of the number or total value of transactions. In other words, the infrastructure providers, the bitcoin miners that validate the blocks, are incentivised by economical elements. This guarantees a continuous operability.

Bitcoin – Currency or Commodity?

The parameters described above vary somewhat for each crypto asset. As an example, the bitcoin blockchain parameters are defined as follows: a limit of 21 million coins that can be produced was defined. This fixed final supply is a characteristic that other crypto assets may not have. The rate of bitcoin block creation is adjusted every 2016 blocks to aim for a constant two-week adjustment period (equivalent to6 blocks per hour). The number of bitcoins generated per block is set to decrease geometrically, with a 50% reduction every 210,000 blocks, or approximately every four years.

With current block rewards, bitcoin’s inflation rate is 1.8% (and will stay at or below this value until all bitcoins are mined and reach the final number of 21 million). Bitcoin’s purchasing power will continue to grow over time if demand continues to increase. This commodity-like feature offers investors the opportunity to diversify both systemic risk that is connected to government-controlled fiat currencies and inflation risk linked to expansive monetary policy. Bitcoin also provides access to an alternative source of performance that is not connected to pure economic output.

The rationale for bitcoin and crypto assets as a hedge against inflation truly strikes at the root of inflationary problems: these are both assets and a store of value outside of any national monetary system. Wealth is dissociated from the core: government or centralised governance actions are not simply symptoms, rather the tip of the inflationary iceberg. In our current phase, political leadership is more centralised and may destabilise as an economic crisis intensifies, bitcoin and crypto assets can act as the ultimate hedge. This destabilisation could include currency debasement, rampant price inflation, central bank and fiscal policies gone wrong, and actions leading to nations or governments seizing, freezing, or grossly taxing citizens’ fiat currency wealth.

Business Case for Crypto Assets

But what about the sheer number of different crypto assets? Are they really needed? The answer might be yes or no. It is a new technology that allows new business models, especially where different participants work together that do not know each other or have minimal trust for each other. It can increase efficiency in transaction speed, lower fees, increase transparency, and it can eliminate many intermediaries that are needed in the traditional world. It goes beyond the features of a currency and transfer of wealth: in so-called smart contracts, it allows payments to be linked directly to events and instantly settled. It allows a machine economy where each robot pays its peers for delivered services.

As an investment case, bitcoin is very early stage and offers big potential, as its long-term correlation is low compared to traditional asset classes. Its supply is fixed and demand is variable, with different, independent, active players with various motivations to participating in crypto trading and investing. These include:

- Long-term investors, who do not really care about correlation and volatility

- Short-term active traders, who are taking long or short positions

- Tech nerds, who are buying or selling crypto assets based on technological expectations

- Investors, who have lost faith in governments

- Investors, who are looking for alternatives to diversify systemic risks

- Market participants, who are looking for long-term inflation protection after years of quantitative easing and recent additional cash injections to fight recession in the real economy

- People who prefer to be their own bank in times of general uncertainty

Opportunity for Hedge Funds

The absence of valuation models for bitcoin – and consequently the absence of a defined fair value – attracts quantitative, systematic investment approaches. The young and inefficient crypto market is still dominated by retail traders that are monitoring pure price action. In combination with the activity of the various market players, this increases the strength of trends, and this situation improves the profitability of trend following long/short approaches and delivers attractive risk/return profiles.

This article featured in HedgeNordic’s report “Technology and Hedge Funds.”