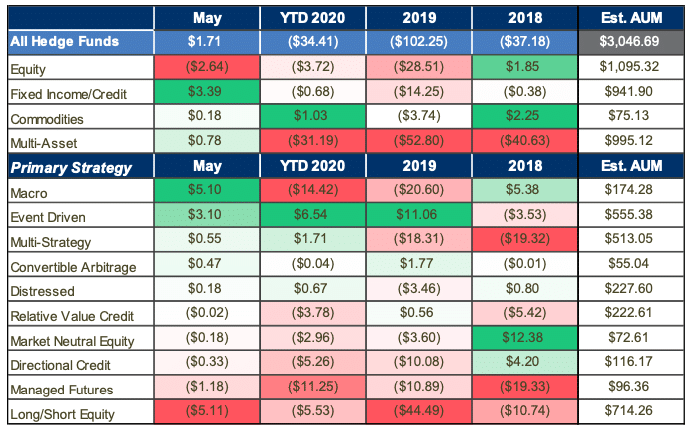

Stockholm (HedgeNordic) – After pulling $32.7 billion out of hedge funds in the first four months of 2020, investors added an estimated $1.7 billion to the global hedge fund industry in May, according to eVestment. The industry’s assets under management increased to $3.05 trillion due to performance gains.

Although last month’s figure of net flows was insignificant relative to the industry’s assets under management, the overall volume of asset movement – the sum of the absolute values of both inflows and outflows divided by the prior month’s reported assets – remained elevated. The average monthly volume of asset movement throughout 2019, for instance, was 2.6 percent of assets under management. The volume of asset movement relative to overall assets increased to 4.9 percent in March this year, which means that a large amount of capital was moving in and out of the hedge fund industry. The asset movement figures for April and May were 3.4 percent and 3.3. percent, respectively.

“The data in May shows flows were near flat and the volume of asset movement was high,” says Peter Laurelli, eVestment’s Global Head of Research. “This is a sign that new allocations are being made while redemptions persist,” he continues. The hedge fund industry’s assets under management have been hovering around $3 trillion since mid-2014. “More than anything else, performance has been the primary reason preventing assets from falling,” points out Laurelli. “This is not how an industry grows and thrives.”

With an estimated $5.1 billion in net outflows, long/short equity funds experienced the largest volume of net redemptions as a group last month. In a report for the month of April, eVestment wrote that “while redemptions continued within this space, they were not nearly as high as other segments, despite some elevated losses within some prominent directional equity funds.” Last month’s net outflows appear to have been a reaction to the March losses incurred by long/short equity funds. The group’s net outflows for the first five months of 2020 amounted to $5.5 billion.

Macro managers, April’s biggest losers in terms of net outflows, received an estimated $5.1 billion in net inflows in May. “After three months of large redemptions, macro funds see some inflows,” writes eVestment. Macro managers experienced $14.4 billion in net outflows as a group in the first five months of the year. “There has been a reprieve in the outflows from some macro managers in May, with some large new allocations indicating there is belief in certain products’ ability to right the proverbial ship,” eVestment continues. “While outflows in prior months were highly targeted, inflows in May were a bit more widespread, a generally positive sign for the group after a difficult few months.”