Stockholm (HedgeNordic) – Staying invested in stock markets over the long term (many, many years) has historically paid off, but occasional bear markets are ugly and painful for many investors. In cooperation with Matti Suominen, Professor of Finance at Aalto University, Finnish insurance firm Mandatum Life has developed a systematic strategy – branded Slim Tail – that provides positive exposure to equities in bull markets and limited or even negative exposure in bear markets.

Mandatum Life Slim Tail US Long/Short Equity is one vehicle powered by the Slim Tail strategy. “We want to have long exposure to equity markets most of the time and maintain low exposure during bear markets, which are often significantly shorter than bull markets,” explains Lauri Vaittinen (pictured), who has developed systematic strategies with Suominen for nearly 20 years. The Slim Tail strategy leans strongly on the academic research they conducted together.

What Does Their Research Preach?

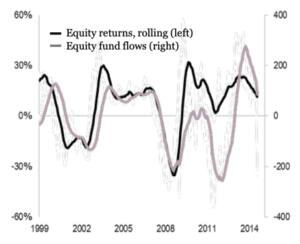

There is quite a refreshing spin to the dull disclaimer lingo “past performance is no guarantee of future results” used prominently in Mandatum’s communication. Citing previous research, Suominen points out that “past six- to-12-month equity and bond returns significantly predict future equity returns,” mainly because past returns “predict investors’ arrival to the market, predict future fund flows and predict investors’ use of leverage.” In short, “past returns from equities and bonds predict future investor behaviour,” summarizes Suominen. Because “past equity and bond returns drive fund flows and vice versa,” Mandatum Life Slim Tail US Long/ Short Equity uses a systematic approach that “alters the exposure to equity markets based on estimates of future capital flows,” according to Vaittinen.

“Equity returns are very correlated with fund flows,” explains Vaittinen, “but flows usually lag behind.” Instead of waiting for lagging data on fund flows to adjust exposure, the systematic Slim Tail strategy “tries to proxy fund flows using cross-asset signals from bonds such as yield curves and time-series data such as equity prices,” says Vaittinen. “The fundamental idea is that we try to be ahead in the decision-making process by estimating a proxy for fund flows.”

“Our systematic model is designed to calibrate normal economic cycles and not just price movements.”

Since “there is a positive carry from equities over the long term,” Mandatum Life Slim Tail US Long/Short Equity will maintain long exposure to equities about 85 percent of the time “with varying degrees of net exposure.” According to Vaittinen, “our systematic model is designed to calibrate normal economic cycles and not just price movements,” which implies the strategy does not seek to capture shorter-term moves in equity markets. “Both bull and bear markets are driven by more longer-term, gradual shifts in share price development, fund flows and leverage levels,” finds Vaittinen, who emphasizes that “we try to focus on much longer time horizons and longer market cycles.”

“Both bull and bear markets are driven by more longer-term, gradual shifts in share price development, fund flows and leverage levels.”

“Our strategy does not go short every time stock prices go down,” highlights Vaittinen. But when markets become more volatile, Mandatum Life Slim Tail US Long/Short Equity reduces the net market exposure and “becomes more tactical by engaging in shorter-term trading.” This shorter-term tactical approach revolves around the so-called turn-of-the-month phenomena, which exhibits strong and highly predictable return patterns around the turn of the month due to monthly flow cycles. These cycles reflect many large flows such as salaries, pensions, dividends, mutual fund distributions, fund redemptions.

The Turn-of-the-Month Phenomena

Research conducted by Suominen and Vaittinen finds “systematic patterns in institutions’ trading” around the turn of the month. According to the research, there is “a large systemic liquidity demand in the economy at the month-end,” which triggers increased liquidity-driven trading. Their research shows that at T-4 (four days before the end of the month) or earlier, “pension funds and other institutions liquidate their stock holdings to guarantee cash at the end of the month.” More interestingly, up to 40 percent of month-end returns between T-3 and T are attributable to reversals from price pressure from mutual fund outflows, which implies that “these returns are predictable and high in bear markets.”

During the Lehman crisis, for example, cumulative returns were exceptional low between T-8 and T-4, amounting to a negative 30 percent. The cumulative returns between T-3 and T, however, were exceptionally high at 40 percent. “During times when there are a lot of outflows and negative market movements, markets are short of liquidity and the turn-of-the-month phenomena is much stronger,” explains Vaittinen.

“If equity markets fall, the net market exposure will be fairly low and most of the trading will likely be concentrated towards the end of the month to capture the turn-of-the-month phenomena.” When the Slim Tail strategy becomes defensive and carries ample cash around, “there are high returns to end-of-month investing.”

“We combine the turn-of-the-month trading with the longer-term Slim Tail strategy. The way we combine the two strategies is unique.”

“We combine the turn-of-the-month trading with the longer-term Slim Tail strategy,” clarifies Vaittinen, who emphasizes that “the way we combine the two strategies is unique.” Although the two strategies can be seen as two distinct pillars of the fund, “they both rely on the large flows of investor capital in or out of the market.” The strategies “work quite well when combined together.”

Ever-Adjusting Net Exposure

By combining Slim Tail and turn-of-the-month strategies, Mandatum Life Slim Tail US Long/Short Equity adjusts its net exposure to the S&P 500 between -50 percent and 100 percent using listed index futures. “Depending on market conditions and fund flows, the systematic approach adjusts the market exposure using futures on a daily basis,” explains Vaittinen. “We aim to create a product that is negatively correlated to traditional asset classes during bear markets.”

“Depending on market conditions and fund flows, the systematic approach adjusts the market exposure using futures on a daily basis.”

Mandatum Life Slim Tail US Long/Short Equity delivered an annualized return of 7.7 percent since launching in February 2016, and recorded positive performance in each of the past four years. The fund achieved an inception-to-date Sharpe ratio of 0.87. “While the fund is not a typical hedge fund that seeks to capture alpha opportunities, the product aims to offer investors exposure to equities in bull markets and protection of capital in bear markets.”

Another Downturn-Protection Vehicle

Towards the end of last year, Mandatum Life launched a trend-following fund powered by machine learning algorithms designed by artificial intelligence firm PROWLER.io. “While the performance of traditional trend-following strategies has declined significantly over time,” argues Vaittinen, “different types of trend-following models performed well during particular periods in time.” Shorter-term-oriented trend-following strategies performed strongly during certain periods of time, whereas medium- or longer-term-oriented strategies performed well in other periods.

“While the performance of traditional trend-following strategies has declined significantly over time, different types of trend-following models performed well during particular periods in time.”

Mandatum Life Managed Futures uses artificial intelligence to “pick and choose the right strategy depending on the market environment,” explains Vaittinen. “The fund changes from running shorter-term trading models to longer-term ones depending on which types of strategies the machine learning algorithms believe are more suitable to the current environment.” Instead of employing a fixed strategy with “returns that are zig-zagging around zero over the years,” Mandatum’s trend-following vehicle relies on machine learning to select the right combination of trading models for a given environment.

“Without sophisticated enough models, one cannot capture the appropriate models for each regime,” argues Vaittinen. “This is very difficult to capture for humans running either qualitative or quant-based strategies.” According to Vaittinen, the core of Mandatum Life Managed Futures is choosing the right trend-following model at a given time and optimizing returns at scale across a wide universe of liquid, exchange-traded futures contracts. Whereas Vaittinen reckons Mandatum Life Managed Futures has a competitive advantage over traditional trend-followers due to its “regime-shifting” properties, “traditional CTAs will likely see better performance ahead compared to the recent past too.”

This article featured in the Nordic Hedge Fund Industry Report 2020.