Stockholm (HedgeNordic) – Alejandro Arevalo, fund manager in Jupiter’s emerging market debt team, explains why an understanding of the key differences between corporate and sovereign emerging market debt can help investors better position their portfolios, and with lower volatility.

Emerging market debt is a tricky asset class to navigate because its sub-asset classes have very different characteristics. Two of the most important sub-asset classes of emerging market debt are corporate debt and government debt denominated in hard currency. Understanding the differences between them can help investors better position their portfolios and with lower volatility.

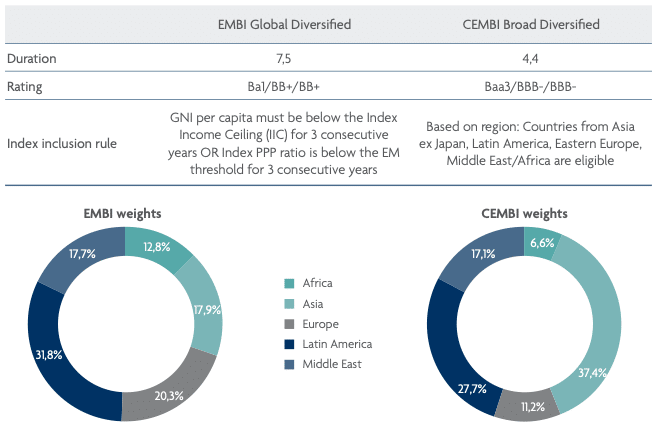

Index Differentials are Key

The indices representing emerging market (“EM”) corporate and sovereign bonds have some key differences which makes a direct comparison between the indices of limited use. The sovereign bond index has a higher overall duration and a lower overall rating than the corporate bond index. This tends to mean that the corporate bond index is less volatile. Moreover, the regional allocation for the sovereign and corporate bond indices is also different due to the index inclusion rules. The sovereign bond index tends to have a bias towards developing countries whereas the corporate bond index also includes countries which one wouldn’t usually refer to as “emerging market” e.g. Singapore. Because of such differences the sovereign bond index has a higher spread than the corporate bond index as it does not compare like for like.

While the differences between the corporate and sovereign emerging market bond indices might seem technical and mundane, they have significant impacts on risk management. Below are some of the key points to consider when choosing to allocate between corporate and sovereign emerging market debt:

- The corporate bond hard currency investable universe is about $2.3tn compared with $1.1tn for sovereign. While the total liquidity is higher for corporates, the investable universe is split into about 700 issuers compared with about 80 for the sovereign bond universe. Each position size in the corporate portfolio, therefore, tends to be smaller.

- The corporate bond universe allows room for better diversification because of the variation in sectors. For example, it is easier to express a bullish or bearish view on the global economy by being invested in cyclical or non-cyclical sectors respectively. Corporates also tend to have higher variation in ratings which offers more flexibility in investment. Therefore, the volatility of the corporate bond portfolio can be lower.

- Corporates typically offer a higher spread to sovereigns. You can therefore lock in higher yield to maturity. Credit risk also tends to be higher for corporates, but this is something that can be analysed through detailed credit research to find attractive opportunities.

- The factors analysed while investing in corporates also tend to different. Through a bottom-up credit analysis of the financial statements of the companies, one’s expectations can be formed on the future liquidity of the company. For government creditworthiness, on the other hand, one must analyse the top-down factors to assess liquidity. However, government creditworthiness is also heavily influenced by politics which often takes unexpected turns.

EM Corporate Bonds Offer Better Risk-Adjusted Returns than Sovereigns, With Lower Volatility

On a like-for-like basis, corporate bonds almost always offer a higher spread over sovereign bonds. For example, Gazprom, the Russian oil and gas producer is one the strongest credits in Russia and has a one notch higher rating according to Moody’s. Despite having a higher rating, Gazprom’s curve offers about 50bps higher yield than the Russian sovereign curve. There are some rare exceptions to this. For example, in Ukraine, MHP, a poultry producer, offers yield about 80bps tighter than the sovereign. Nevertheless, in most cases, by being invested in corporate emerging market bonds, an experienced investor can boost the return potential of the portfolio.

In terms of the long-term historical risk and return attributes, corporates have returned about 7.2% p.a. since 2002 compared with 8.7% p.a. for sovereigns during the same period. However, the volatility of the sovereign index is about 1.6x that of the corporates. Hence, the risk-adjusted return, or the Sharpe ratio, is much higher for the corporate bond index.¹

Credit Analysis is Key to Managing Currency Risk

Despite corporates having better risk-adjusted returns than sovereigns, currency risk is often cited as a reason to not invest in corporates issuing hard currency debt. While this might appear intuitive, digging a bit deeper into the details can provide quite a different picture. To analyse the real impact of EM currency depreciation it is important to first split corporates between international and domestic companies. Examples of international companies are oil and gas or metals and mining industries; in other words, any company which sells its goods and services primarily in US dollars. For such companies, EM currency depreciation is positive because their revenue remains unchanged whereas their cost component, which tends to be in local currency, goes down when measured in US dollars. As a result, currency depreciation can result in deleveraging.

For the domestic companies, or any company which sells primarily in their local currency and has costs in local currency, these typically tend to leverage up when there is currency depreciation. However, the impact of this is usually short term. In the long run, these companies can pass on the impact of currency depreciation onto the consumer through inflation.

By analysing the credit fundamentals of corporates, one can manage currency risk effectively. Moreover, corporates issuing in hard currency typically tend to have low mismatch in currency (difference in currency breakdown of revenue and debt) or have underlying long US dollar exposure e.g. the oil and gas and metals and mining companies mentioned earlier. Consequently, despite EM currency depreciation corporate debt returns have been resilient. Between July 2011 and January 2016 (a period of sharp EM currency depreciation), EM currency depreciated 40%, while the EM corporate bond index was up 22%.²

In Conclusion

To conclude, EM hard currency corporate debt is a larger investable universe offering greater diversification and higher yield relative to EM sovereign debt. By analysing corporate credit fundamentals, the currency risk can be managed effectively: EM corporate bonds have historically outperformed the sovereign bond index on risk-adjusted return, mainly due to their lower volatility.

¹Source: Bloomberg, 2002- end of July 2019, JP Morgan and Bloomberg indices.

² Source: JP Morgan Corporates: CEMBI Broad Diversified; Sovereigns: EMBIGLOBAL Diversified; EM currencies: EMCI Index.

This article featured in HedgeNordic’s Special Report on “Alternative Fixed Income.”