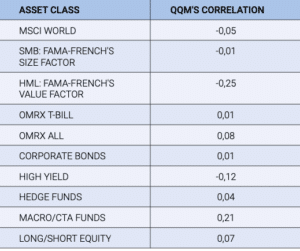

Stockholm (HedgeNordic) – With minimal correlation to equities, corporate and high-yield bonds and other asset classes, systematic market-neutral fund QQM Equity Hedge represents an interesting alternative to fixed-income investments, particularly in the current low-interest-rate environment. Since Ola Björkmo and Jonas Sandefeldt (pictured) started managing the fund in July of 2010, QQM Equity Hedge has on average returned 4.6 percent per year net of fees with near zero correlation to both local and global equities, as well as other asset classes.

“The low correlation is the main reason our strategy represents a good alternative to fixed income,” argues Jonas Sandefeldt. “Although our returns exhibited higher volatility than a typical bond fund, adding our fund to a mixed-asset portfolio, in fact, lowers the volatility of the entire portfolio since our correlation with equities and bonds is so low.” More importantly, QQM Equity Hedge does generate higher returns than a typical bond fund. “In short, our fund can increase the expected return of the overall portfolio and simultaneously lower the volatility of the portfolio,” adds Sandefeldt.

“Zero less fees is not a very attractive investment proposition.”

Ola Björkmo further points out that investors most likely cannot expect attractive or even positive returns in the fixed-income space in the near to medium term. “If you look at yields in the fixed-income market, the returns investors can achieve are very close to zero,” says Björkmo. “Zero less fees is not a very attractive investment proposition.” QQM Equity Hedge, meanwhile, aims to achieve an annual absolute return between six and eight percent over the long-term. “Given that we are targeting a volatility of eight percent, we aim to achieve a Sharpe ratio of between 0.75 and 1,” explains Sandefeldt.

However, Björkmo cautions that investors should not expect QQM Equity Hedge to outperform long-only or long-biased funds in sustained equity bull markets. “Being market-neutral by shorting the same amount we go long, we expect to lag behind the returns generated by long-only or long-biased equity funds in bull markets. On the other hand, our track record extending back more than 9 years, evidences the strategy being profitable two months out of three, regardless of the direction of the equity market.”

The Magic Sauce

QQM Equity Hedge employs a purely systematic strategy to build a well-diversified market-neutral portfolio that aims to capture fundamental momentum in listed European companies. As Björkmo explains, “we seek to capitalize on fundamental momentum by looking at earnings development, revenue growth and analyst earnings revisions for the companies in all the ten countries we trade.” QQM Equity Hedge builds a market-neutral portfolio for each of the ten countries, which, after screening for ESG criteria and internal requirements, represent a current investment universe of about 1,000 stocks. The Fund holds on average 300 single name long and 300 single name short positions.

“We seek to capitalize on fundamental momentum by looking at earnings development, revenue growth and analyst earnings revisions for the companies in all the ten countries we trade.”

“We examine the last six months of data and use fundamental information to select a group of companies with strong momentum within their fundamental data for the long portfolio and, conversely, a group of companies with weak momentum in their fundamentals for the short portfolio,” explains Björkmo. The team’s proprietary systematic model puts more weight on fresher information with the model recalibrating as new data is released. “After studying all the academic research we could find, studying large data sets and drawing conclusions from those data sets, we have built a systematic model that incorporates how the market reacts to information,” says Björkmo.

“Even if all our companies perform badly in terms of fundamental performance, we engage in a relative play by selecting the better companies in the market and selling short the weaker ones,” explains Björkmo. As for the fundamental data that goes into QQM’s systematic model, “the most important element is earnings but we combine that with analyst revision trends, revenue development and to some extent price momentum.” In essence, QQM Equity Hedge relies on various fundamental data points, complemented by a price momentum overlay.

As for the portfolio of short positions, “our model identifies companies with weak earnings prospects, companies that running out of cash and seek equity issuances and companies likely to issue profit warnings,” explains Sandefeldt. “If a business has been doing poorly, it takes a long time to restructure its business by closing down factories, reducing the workforce or changing products or business models.” Weak businesses typically perform poorly for a long time before evidence of a turnaround is visible, if at all.

Since investors do not always pay sufficient attention to fundamentals, business fundamentals and stock prices can and do diverge on some occasions. “Big shifts in investor sentiment in the market represent the biggest challenge to our approach,” acknowledges Sandefeldt. Over the long term, however, “the market is always right,” argues his colleague. As Benjamin Graham once said, “in the short run, the market is a voting machine, but in the long run it is a weighting machine.”

“Fundamental information will drive the stock market sooner or later,” says Sandefeldt, who adds that “there might be times when there are discrepancies for a while.” Mean reversion is the one thing investors can rely on over time. “We have suffered drawdowns of 11 percent three times in the fund’s history and each time it has taken us eight months at the most to recover,” points out Sandefeldt. “The fundamentals drive stock market prices in the long term.”

“Fundamental information will drive the stock market sooner or later.”

True Diversification Always Pays Off

Given the low-return environment in the fixed-income space, Björkmo reckons that institutional investors will gradually move some portion of their portfolios away from fixed income to other asset classes. “Most of the mid-level institutional investors, certainly not the largest institutions, are underweight hedge funds and they would benefit a lot if they were to add sources of alpha,” argues Björkmo. “If one looks at investors such as the AP Funds or the Yale University endowment, they maintain much more diversified portfolios and have generated similar or better returns compared to their peers with much lower volatility.”

Whereas hedge funds may pursue different objectives, “hedge funds designed to protect capital or generate absolute returns should not lose money when things turn sour,” reckons Björkmo. “Then investors are losing money across almost all of the portfolio.” According to Sandefeldt, “investors should always maintain a diversified portfolio”, and some institutional investors will move out of long-only fixed-income product to something else, including high-yield products. Yet, investors should be aware of the relatively high correlation between corporate bonds or high-yield bonds and equity markets.

“Investors add a lot of equity-like exposure to a portfolio by investing in high-yield products,” reckons Björkmo. “We are not very fond of hidden beta and there is a lot of hidden beta in high-yield products,” he adds. “All of a sudden this hidden beta will show up when equity markets perform poorly.”

“Most people do not sleep very well with 100 percent exposure to equities because the volatility is so high.”

Although Sandefeldt believes in diversification, “if investors can handle 100 percent exposure to equities, they should go for 100 percent in equities.” But “most people do not sleep very well with 100 percent exposure to equities because the volatility is so high,” so investors should have other things in their portfolios. Given the low correlation with equities, bonds and other assets, an equity market-neutral strategy such as QQM can indeed pass the test of being the better fixed-income play.