(Partner Content by Novus) – Recent industry noise surrounding smart beta suggests such strategies are no mere fad. What exactly do investors hope to achieve with smart beta? Sustained alpha is a given. According to a recent study, smart beta is also considered a way to weather potential storms, with 70% of smart beta ETF users reporting that they’re searching for risk mitigation or volatility control.

While some smart beta strategies boast astounding returns when the market is up, a volatile year like 2018 will show whether an index is simply full of beta-loaded names, or if the factor exposure has truly tapped into something smart. By leveraging our public filings database to conduct in-depth research on the hedge fund industry, Novus has developed and tracked indices based on various hedge fund factors. In this article, we’ll compare two of our proprietary indices—the Novus Conviction Index and the Novus Health Care Index—and subject each to analysis on: (1) sustained alpha generation, and (2) volatility protection. We’ll also reveal a few underlying details related to these indices’ performance.

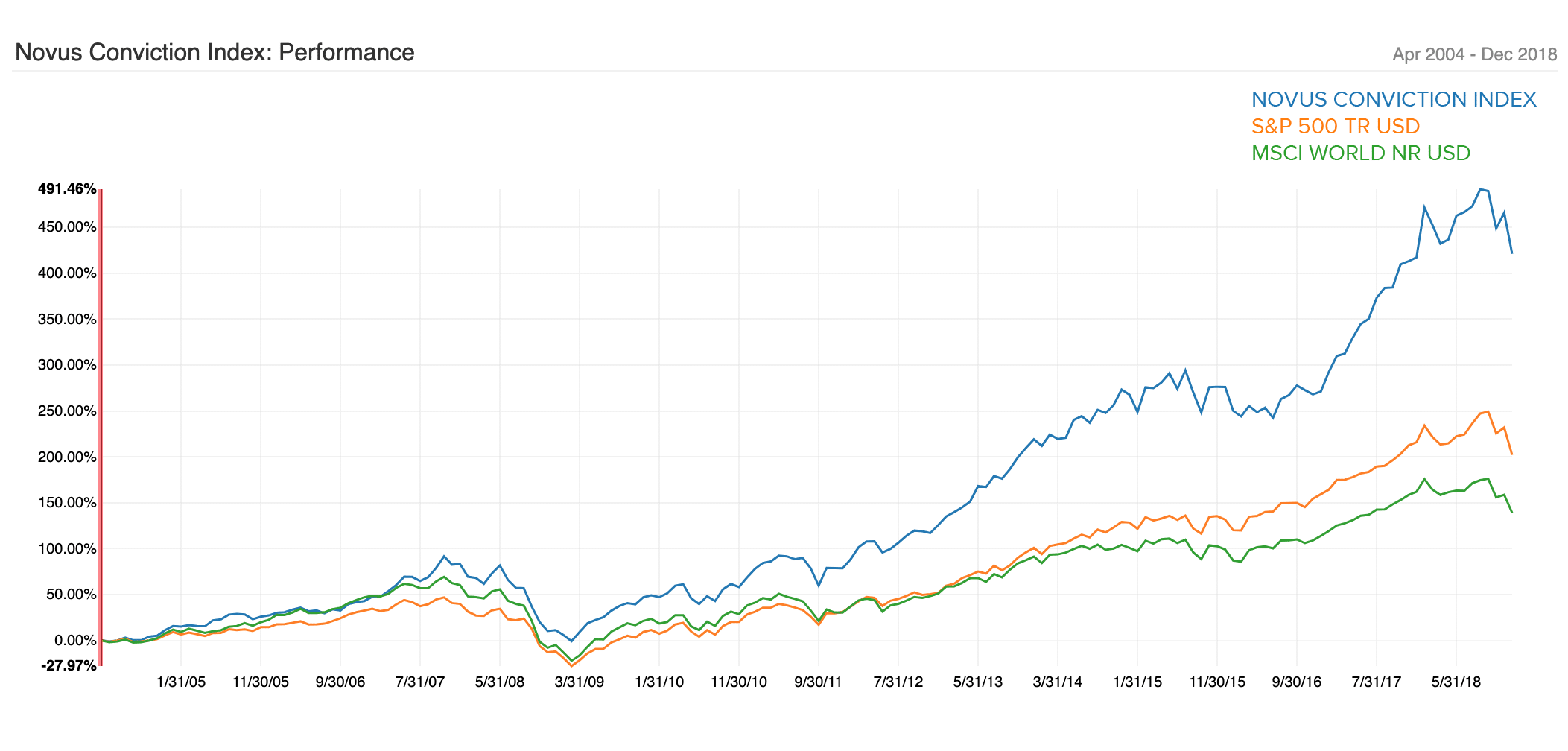

NOVUS CONVICTION INDEX

One of our most closely followed research areas, the Novus 4Cs Indices, tracks important hedge fund factors through public equities. The factors are conviction, consensus, crowdedness, and concentration. Each is constructed from a dataset of public filings from over 1,800 hedge fund managers in the Novus Hedge Fund Universe (HFU). Every quarter after 13F filings, we publish the names and key stats for each index (see last quarter’s report here).

Of these four ways of determining “the best ideas from hedge funds,” our research has shown that conviction is the most consistent factor for extracting alpha.

The Conviction Index is constructed and rebalanced around the stocks that managers show conviction in, as proven by their willingness to size up a name. If a stock accounts for a significant portion of a manager’s portfolio, it’s considered an investment with conviction. In addition to an average annualized return of 11.48% since 2004, the Conviction Index has a track record of consistently beating the market, having outperformed the S&P 500 in 66% of quarters since inception.

The statistics from the past ten years are notable, with a Batting Average of 65.95% and a Win-Loss ratio of 2.93x. In other words, the alpha generative names outnumbered the alpha detracting names, and the average contribution from a winner was nearly three times higher than the average detraction from a loser.

Let’s now turn to Conviction’s volatility and down-side risk over time. Barring a rough spell in 2016, the Conviction Index limited losses as compared to the S&P 500 and MSCI World in some of the most turbulent phases in global markets in the last decade.

The drawdown in 2018 is particularly noteworthy, with the index outperforming the benchmarks in key months such as February and December. The algorithmic rebalancing as underlying managers tactically moved away from tech stocks accounts for this shift.

In the fourth quarter of 2018, several big players in the communication services sector such as Twenty-First Century Fox (FOXA), T-Mobile (TMUS) and Comcast (CMCSA) were sized up in the index, replacing popular IT names such as Amazon (AMZN), Alibaba (BABA), Alphabet (GOOG) and PayPal (PYPL). At this time share prices at tech companies were taking a hit due to numerous issues ranging from slowing growth to privacy concerns.

The Conviction Index’s performance since inception, coupled with its history of risk mitigation, has made it Novus’ flagship index.

Note: In 2016, Novus entered into a data partnership with Barclays to develop an investable index family based on the Conviction Index. For further information please contact Barclays.

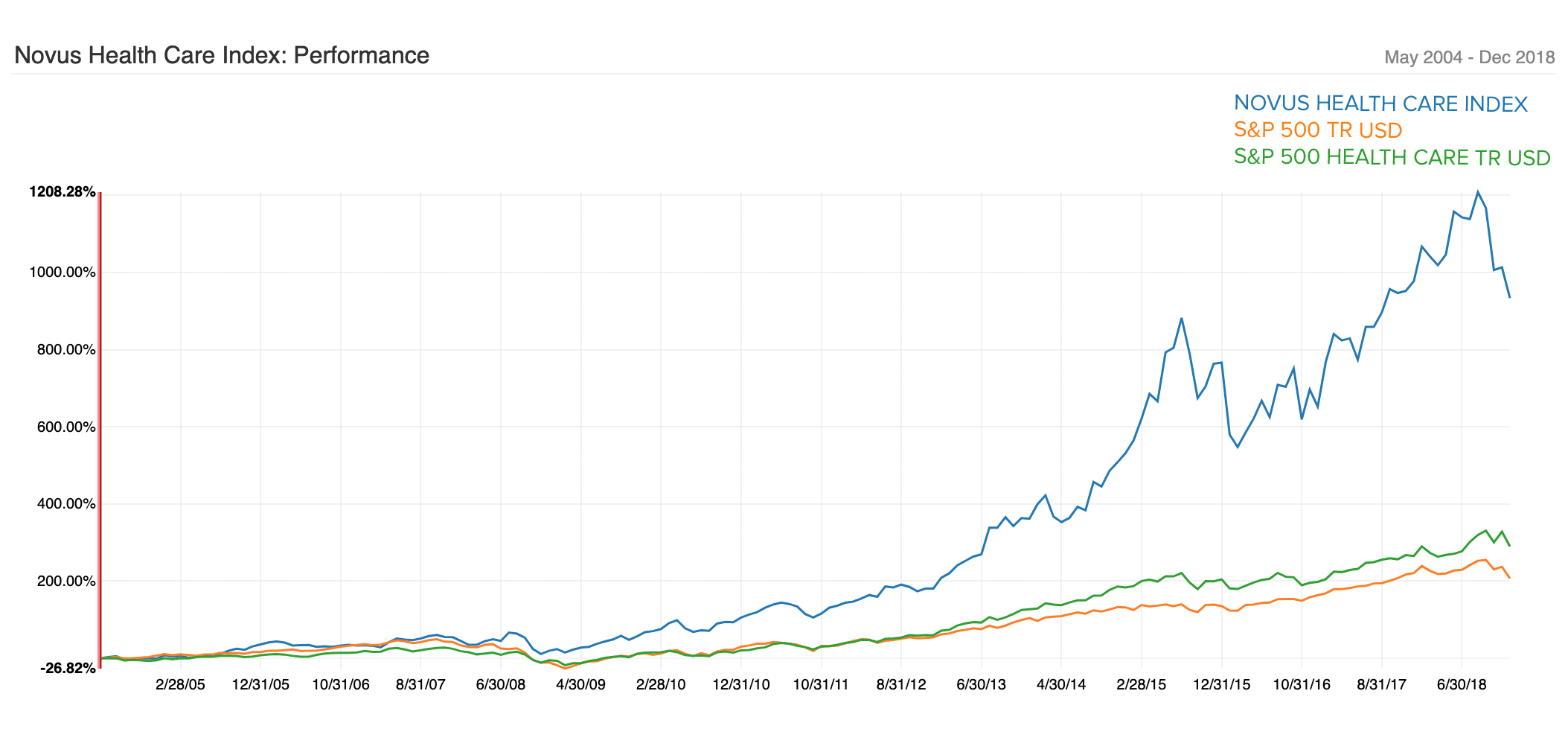

NOVUS HEALTH CARE INDEX

A next step in evaluating the Conviction Index’s success could be to study what sub-factors are driving performance. One approach for this is sector analysis. Tracking sectors is nothing new to the smart beta world, with Forbes reporting last year that single-sector ETFs have attracted more than $300 billion customers worldwide. After watching interest grow, we decided to build upon the Conviction concept, and created the Novus Health Care Index, which tracks “the best ideas among hedge funds in the healthcare space.” The average annualized return is 17.26% inception to date, seen below against the S&P 500 and S&P 500 Health Care indices.

Our healthcare index also has a healthy Batting Average of 56.25% over the last ten years. The Win-Loss ratio, however, sits at 1.22x—much lower than the Conviction Index—meaning the average gain from a winner outweighs the average detraction from a loser by a smaller magnitude.

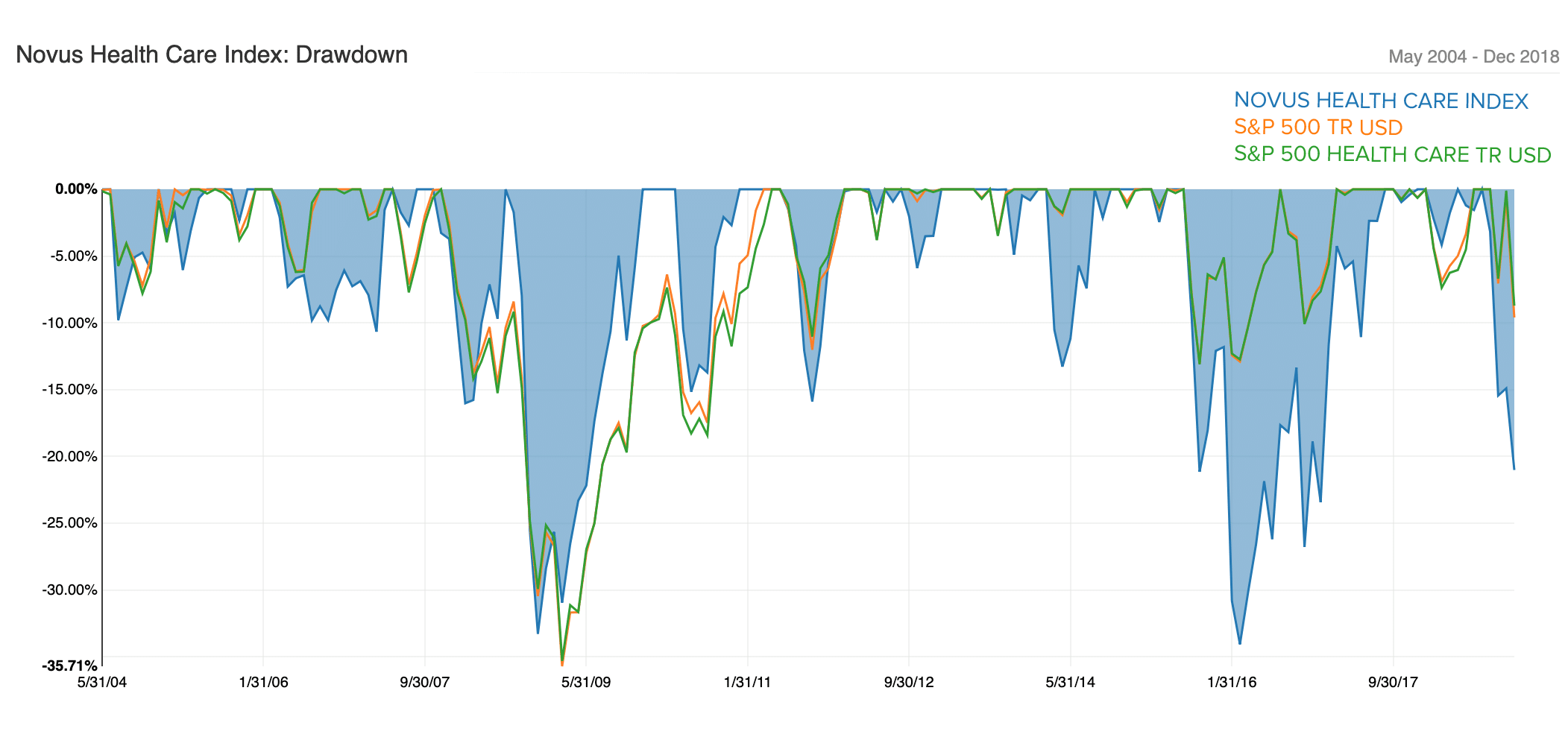

This makes sense when analyzing the drawdown:

We can see that while showing attractive alpha, this index has a much higher volatility profile than the Conviction Index and relevant market benchmarks. Investors looking for the highest-octane stocks in healthcare may still find this index interesting, and perhaps would do well to couple it with a hedging index.

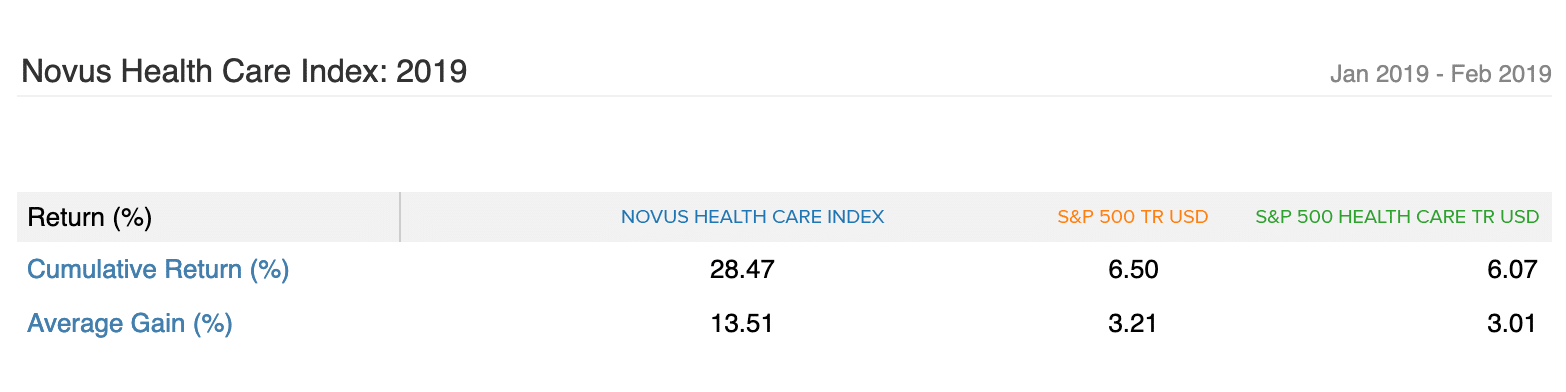

As a side note, we’ve noticed early returns for 2019 are quite encouraging, especially given the index ended the year at a low of -7%. Effective changes at the position level enabled the index to bounce back to over 19% in January and stand over four times higher than the S&P 500 and S&P 1500 Health Care indices at the end of February.

The index is heavily concentrated in biotechnology, with Avexis (AVXS), Loxo Oncology (LOXO), Ascendis Pharma (ASND), Argenx (ARGX) and Tesaro (TSRO) being the top names in Q4 of 2018. Our research piece last year explored this trend further by constructing and analyzing a portfolio of public holdings of over 50 healthcare specialists.

CONCLUSION

Worthy smart beta opportunities exist, but the responsibility will always remain with the investor to evaluate strategies based on her investment objectives and time horizon. Paramount in this analysis is (1) sustained alpha and (2) volatility control. Here, we’ve demonstrated how smart beta approaches can lead to diversified, factor-driven portfolios that outperform the market over consistent periods of time.

At their essence, smart beta can help allocators profit from the aggregate wisdom of the crowd, and help managers find an additional pool of ideas. At Novus, we’re able to help both sides measure the effects of various factors on portfolio performance. We believe that good ideas can come from many sources, which is why we arm investors with tools to analyze and monitor their entire portfolios in a fashion that leads them to true insights, and ultimately, better investment decisions.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security, which may only be made by prospectus or other offering document. Novus is not soliciting any specific action based on this material. It does not constitute a recommendation or take into account the particular investment objectives, financial conditions, or needs of individual clients.