Stockholm (HedgeNordic) – The lending of money has long been one of the most basic functions in finance. But what is direct lending, a term consistently gaining popularity in recent years in the investment arena? Direct lending can simply be defined as old-fashioned bank lending without the bank as the provider of capital. As traditional banks have been cutting back on business lending due to increased regulation following the financial crisis, direct lenders have received a breath of fresh air.

Direct lending is a sizeable yet growing segment of the private debt market, which includes a wider array of illiquid credit products such as distressed debt, mezzanine debt, venture debt, among others. The term private debt is defined as any non-publicly traded debt financing typically offered to small- and middle-market companies. Direct lending deals, meanwhile, represent smaller bank-like loans of between $10 million and $250 million made to companies with up to $100 million in earnings before interest, taxes, depreciation, and amortization. Companies that are too small or too risky to be bank clients, therefore, become clients for cash-rich direct lenders.

The slowdown of bank lending and growth of direct lending

Since the financial crisis of 2008, we have observed banks in the United States and Europe heavily restricting their lending activities to the private sector as a result of heavier regulatory burdens in the form of stricter capital requirements and stronger risk management. According to data provided by the Bank for International Settlements (BIS), both European and U.S. banks have been clamping down on private sector lending since the financial crisis. The role of banks in the European financial system has traditionally been greater compared to the United States, but the bank-driven market on the old continent suffered serious changes in the past decade.

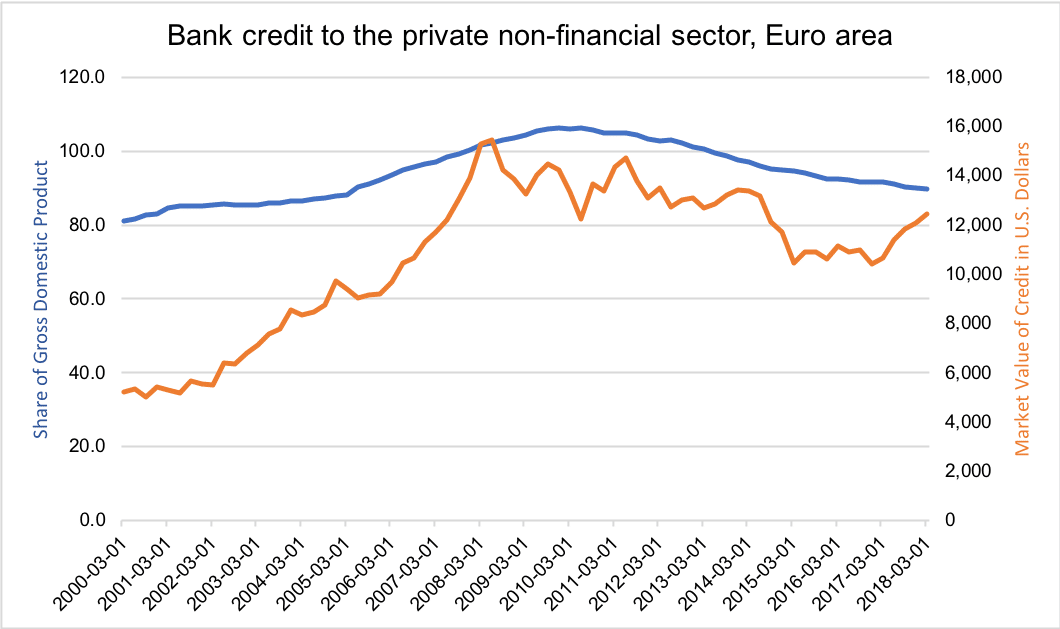

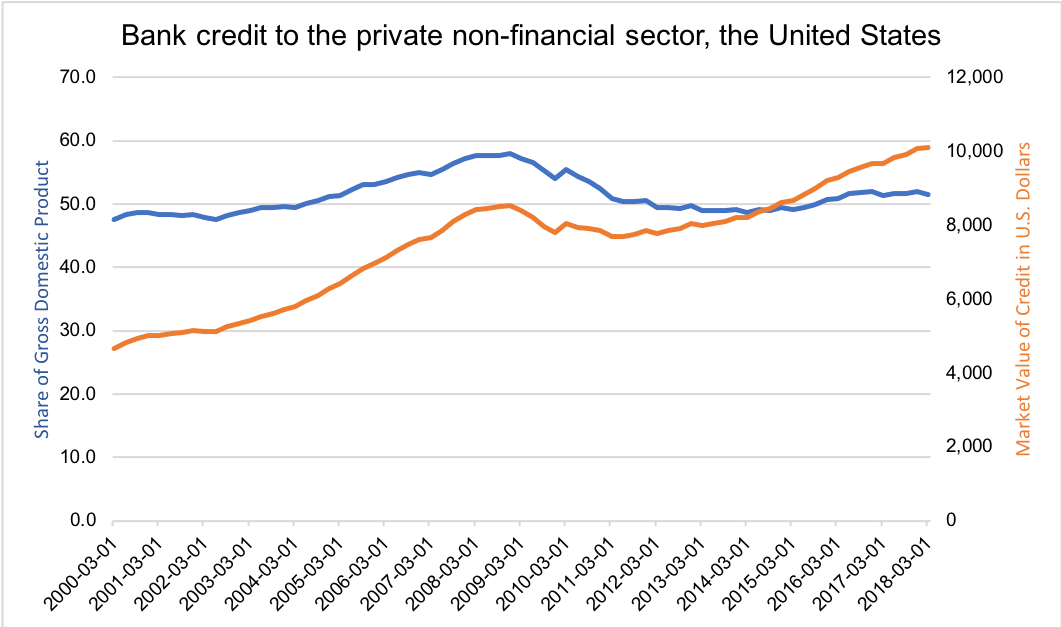

The volume of bank credit to private non-financial firms in the Euro area as a percentage of the region’s gross domestic product (GDP) declined from 106.2 percent at the end of 2009 to only 89.7 percent at the end of the first quarter of 2018. In the United States, bank lending to private firms in the non-financial sector accounted for 89.7 percent of the country’s GDP at the end of 2008, with this proportion declining to 51.5 percent at the end of the first quarter of this year. Therefore, the strong growth in direct lending in recent years has been a story of banks reducing the supply of credit to the private sector.

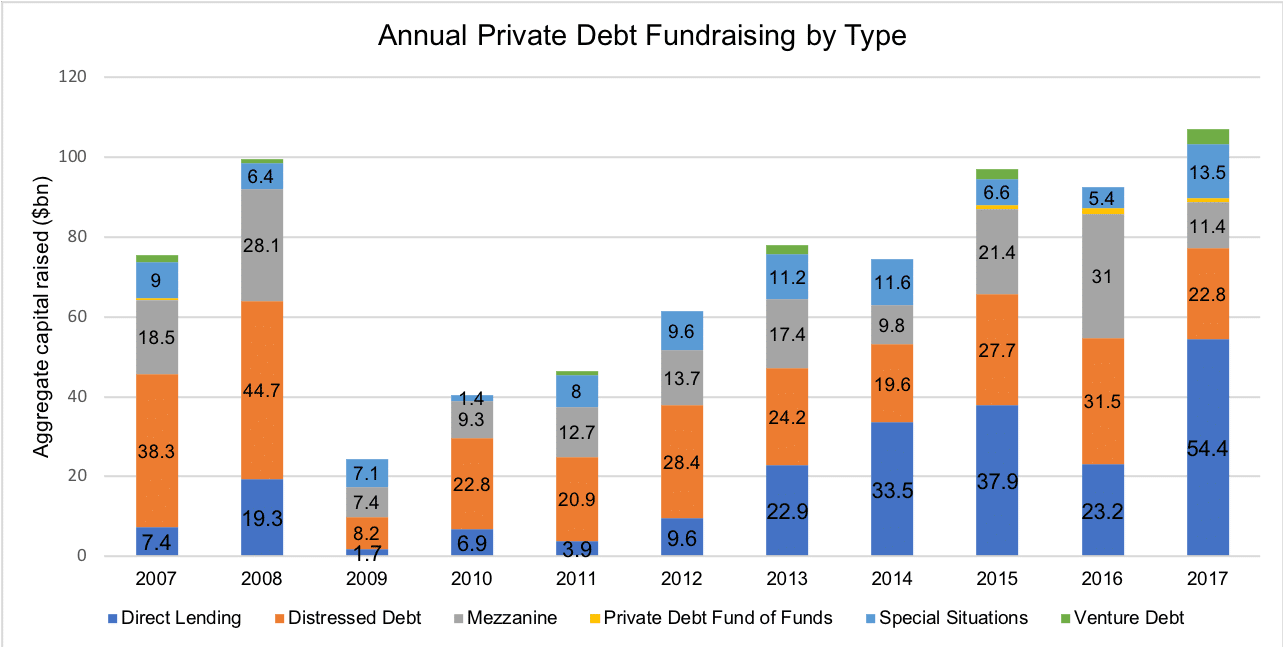

Investors have been increasingly channeling more capital into direct lending funds since the financial crisis, with these funds raising $54.4 billion in capital last year according to data provided by Preqin. Capital commitments declined meaningfully in 2016 compared to the previous year, falling to $23.2 billion in 2016 from $37.9 billion recorded in the prior year. Despite worries over too much capital in the hands of direct lenders chasing too few opportunities, which led to relaxed lending standards, yield compression and weaker covenant protections, direct lending funds raised last year nearly twice the capital raised during 2016. Preqin reports that a total of 389 direct lending funds were in the market at the beginning of the third quarter of 2018 targeting to raise a collective $180 billion in capital. This compares with a total of 350 funds at the start of the second quarter which collectively were seeking to raise $160 billion in capital.

European versus U.S. direct lending market

Because of the relatively heavier reliance on bank lending in Europe, the European direct lending market is less mature compared to the one in the United States. But as European banks are stepping back from providing credit to the private sector, more alternative lenders have begun to emerge on the European continent in the aftermath of the financial crisis.

According to a white paper released by Ares Management in the April of this year, bank supply of leveraged credit to the middle-market in Europe decreased significantly in the past several years, with banks estimated to account for around half of the total European market. Regulatory pressures are anticipated to continue to impact the European banking sector’s appetite for supplying credit to the middle-market segment, whereas institutional lenders are expected to serve as an alternative source of funding for middle-market companies following the example of the United States. U.S. banks are found to account for only nine percent of the country’s middle-market segment.

According to data provided by Preqin, North America-focused direct lending funds raised $32 billion during 2017, compared to a figure of $22 billion raised by Europe-focused funds. European direct lending funds raised more than their North American counterparts during 2016. Recent data shows that 201 direct lending funds in the North American market were targeting to raise $93.8 billion in capital at the beginning of the third quarter of 2018. A group of 96 funds in the European market, meanwhile, was targeting to raise capital amounting to $59.6 billion at the start of the same quarter. This compares with 80 direct lending funds which targeted a capital raise of $39.1 billion in the same period of the previous year.

Types of loan structures in direct lending

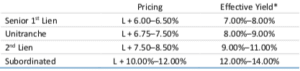

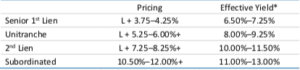

There are a number of loan types in the direct lending market, with the most common ones including: first lien loans, or senior secured loans; second lien loans; mezzanine debt or subordinated debt, and unitranche loans. The most common type of loans in this market is the senior secured loan, which pays a floating rate coupon and matures within a time span of five to seven years. Borrowing middle-market firms tend to pay upfront fees or issue loans at a discount to par, which boosts returns for investors, with these senior secured loans usually containing covenant protections.

The fees, pricing, and covenants of the second lien loan product are found in the gap between lower-cost senior secured loans and higher-cost mezzanine debt financing. Both mezzanine debt and second lien loans are issued with significantly higher coupon rates compared to senior loans. The unitranche debt product, a loan structured to combine senior and junior debt into a single loan at a blended cost of capital, has become an increasingly popular source of financing for middle-market companies in recent years. The lower administrative burden associated with the issue of just one loan and the speed of finalizing such transactions are two important advantages of unitranche loans, which tend to offer higher coupons relative to senior loans because of higher leverage multiples. The two tables display the common pricing of each of the four debt products mentioned above, as well as show the anticipated effective yield offered by each product.

Conclusion

Investors faced years of falling or ultra-low interest rates and equity markets have been enjoying one of the longest-ever bull runs, which likely resulted in moderating expectations for future equity returns. As a result, investors have been forced to hunt for yield, leading to increased demand for direct lending products. Some market participants worry that the hunt for yield damaged the attractiveness of the risk-return profile of direct lending as credit agreements and lending standards weakened and yields compressed. As interest rates are slowing picking up, enthusiasm for direct lending products may endure as direct loans carry floating rates.

Direct lenders are gradually displacing banks as a source of funding for middle-market companies because of increased regulation on the banking sector and innovation in the form of new products such as unitranche loans. Given the increasingly large number of companies requiring capital to expand operations and execute on their business initiatives and the steep downfall in bank lending in recent years, the pool of opportunities for direct lenders may not be drying up as quickly as some anticipate.

Picture © Richard A McMillin—shutterstock