By Ian Wiese – Barings Portfolio Finance: “Staggering” is the word that comes to mind when looking back at the growth of the private equity (PE) secondary market since its inception. One can only imagine whether Jeremy Coller—the founder of Coller Capital and known by market participants as the ‘godfather of secondaries’—could have fathomed how this industry would grow over three decades to reach $114 billion today.1

Secondaries have now become an integral tool for both GPs and investors in navigating private market exposures. From 2022 to 2023, secondaries fundraising grew by 92%, even amid more challenging market conditions.2 Although starting from a lower base, this growth notably surpassed that seen in infrastructure, direct lending, venture capital and other comparable asset classes over the same period. And, despite this impressive growth, secondaries only represent around 6.5% of the broader PE market—suggesting there is still further room to run.3

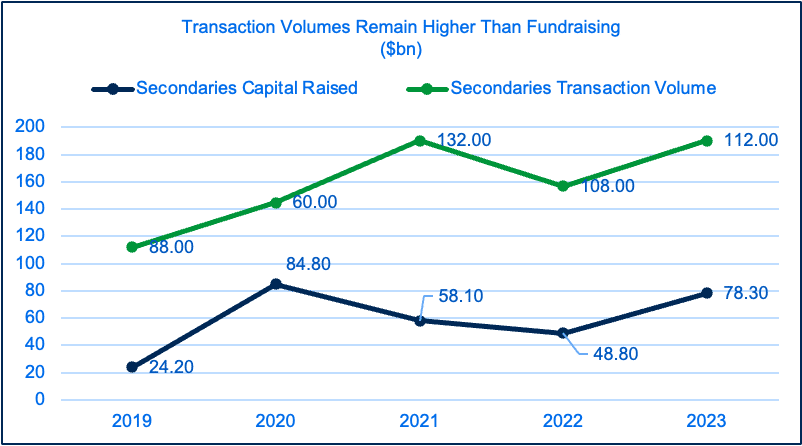

While fundraising has been successful, deal volumes have consistently exceeded fundraising, reaching $132 billion in 2021—and some forecasts are calling for this figure to exceed $140 billion by the end of 2024.4 In fact, with cumulative deal volume over the last five years reaching $500 billion and investor capital representing only $294 billion, a significant capital mismatch exists (Figure 1). This raises key questions for secondary players:

– Going forward, will fundraising sufficiently keep pace with expected transaction volumes?

– Is the secondary market adequately capitalized for the significant growth expected in the years to come?

FIGURE 1: TRANSACTION VOLUMES CONTINUE TO EXCEED FUNDRAISING

One indicator to determine whether an industry is adequately capitalized is the so-called capital overhang ratio:

Capital Overhang Ratio = Available capital (current dry powder + near-term fundraising) [A] + Level of debt available [B] / Secondary deal volume [C].

While the capital overhang ratio should not be viewed in isolation, it is helpful in assessing whether there is sufficient supply of capital to meet the pace of investment (or demand for capital). Simply put, a large overhang ratio may lead to excess competition for new deals, potentially driving higher pricing as discounts shrink and decrease investor returns. On the other hand, a small overhang ratio may curtail further market growth.

Today, the capital overhang ratio in the secondary market has fallen to 1.8x, its lowest level since 2021.5 This suggests that despite a strong growth trajectory, undercapitalization is a potential concern for further growth. Without additional fundraising or use of leverage, some estimates suggest there is only 12-18 months of dry powder available—which is considerably lower relative to other private market segments.

A Deeper Dive: Breaking Down the Capital Overhang Ratio

A breakdown of the capital overhang ratio and the current drivers of each component provide further context:

[A] Fundraising: Secondary managers have allocated significant resources to their fundraising efforts. Dedicated investor relations teams often partner with placement agents, driving the commendable growth of the market. It’s also worth noting the tailwind of increasing interest in the space—as secondaries have become both a legitimate portfolio management tool and often standalone allocation for investors.

[C] Deal volume: Secondary market volume neatly matches NAV growth offset by seven years, implying that the value of secondary transactions could triple from around $114 billion in 2023 to more than $400 billion in 2030.6 This raises the question: How will this growth be sustained?

[B] Level of debt: This brings us to one of the most overlooked variables in the capital overhang equation—the level of debt available to a secondary manager. As we noted in a recent paper, private market growth is set to outpace bank balance sheet growth, resulting in a significant and growing funding gap in the coming years. In the context of the secondary market, where growth has generally outpaced other areas of the private market, this funding gap is exacerbated.

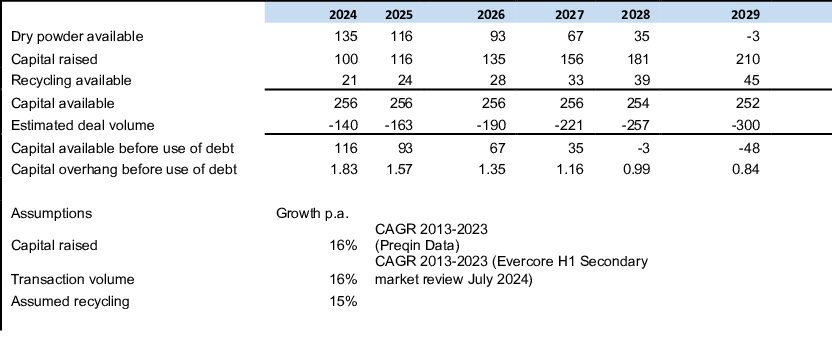

Looking ahead, our calculations suggest the capital available (before the use of debt) in the secondary market could turn negative in the next four years (Figure 2). With banks alone unable to provide the required capital, there is a growing need to fill the shortfall.

FIGURE 2: FINANCING IS KEY TO SOLVING FOR THE CAPITAL OVERHANG

Against this backdrop, many (but not all) secondary managers have realized the importance of building out a capital markets team to manage funding needs with different sources of financing. This can include managing:

- The secondary funds’ liquidity needs as part of the managers’ own respective capital overhang;

- Its internal asset-liability matching strategy as longer-duration debt financing is required to mitigate the asset-liability mismatch risk for investors;

- Its lender base, by diversifying lender groups and types to guarantee a stable and reliable funding base as the need for financing increases.

Given how the secondary market continues to expand—from its origins of traditional LP-led opportunities to seek early liquidity to today’s non-traditional GP-led transactions, credit secondaries and collateralized fund obligations—we believe liquidity management and access to alternative sources of financing will be key to further growth.

Rise of the Non-bank Lenders

With banks unable to the meet secondary sponsors’ financing needs alone, many non-bank lenders, such as asset managers, have stepped in to fill the gap—essentially gaining exposure to the asset class by investing in loans underpinned by secondary investments. For these managers, and by extension their investors—often large insurance companies—the inherent underlying diversification and steady cash flow characteristics of secondaries are some of the key benefits on offer. In addition, these investments are typically rated investment grade.

While the trend toward secondaries has accelerated, it is not new. And in the next few years, we expect the opportunity to amount to more than $24 billion annually. The Barings Portfolio Finance platform has deployed significant amounts of capital into secondary financings on behalf of our clients. We have increasingly been seeing secondary sponsors seek financing options as an active portfolio management tool, often to differentiate themselves from their peers. Our platform can facilitate a range of financing solutions ranging from hybrid financing, acquisition financing of LP portfolios, as well as other liquidity solutions.

Key Takeaway

The secondary market continues to grow in leaps and bounds. Raising capital remains the primary consideration for managers, positioning them to benefit from the expected increase in deal volume. However, it is important for managers to also keep in mind that managing their own access to alternative sources of financing (and investors) is an important, and sometimes overlooked, variable in the capital overhang equation.

For Professional Investors / Institutional only. This document should not be distributed to or relied on by Retail / Individual Investors. Any forecasts in this material are based upon Barings opinion of the market at the date of preparation and are subject to change without notice, dependent upon many factors. Any prediction, projection or forecast is not necessarily indicative of the future or likely performance. Investment involves risk. The value of any investments and any income generated may go down as well as up and is not guaranteed by Barings or any other person. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. 24/ 3930277