By Linus Nilsson, NilssonHedge: As portfolio managers, we strive to create the most robust portfolio, with the highest efficiency, be it the Sharpe ratio, the Information ratio, or any other metric that we find useful. We pack risk in the most optimal way possible by utilizing heuristics, mathematical formulas, or simply our judgment to solve a difficult multidimensional puzzle.

In Finance, this is done under uncertainty, which typically results in two kinds of solutions: Complex solutions relying on viewing the portfolio as a mathematical problem or practical solutions based on experience such as the 1/N concept. “All models are wrong – but some are useful”.

Heuristics or mental models should not be underestimated when it comes to putting together all the pieces. Even Harry Markowitz, the inventor of Modern Portfolio Theory, applied a much more naïve method than full optimization. He later updated his viewpoint to include a more well-diversified portfolio.

“I should have computed the historical covariances of the asset classes and drawn an efficient frontier. Instead, I visualized my grief if the stock market went way up, and I wasn’t in it—or if it went way down and I was completely in it. My intention was to minimize my future regret. So, I split my contributions fifty- fifty between bonds and equities.” – Harry Markowitz (“Your Money and Your Brain” – Jason Zweig)

We want to introduce another heuristic, the ‘Tipping Stability Index’ (“TSI”). The 50/50 portfolio is not a stable solution when viewed from the TSI viewpoint. In 2022, a bond/equity portfolio was anything but stable.

The Perceived Cost of Diversification

Diversification is a mentally costly problem, especially regarding portfolios managed by human portfolio managers. Homo Sapiens have limited cognitive capacity, the average individual can handle four different items in ‘working memory’.

The number of ideas in a portfolio that needs monitoring is thus limited. The proverb ‘put all your eggs in one basket and then watch that basket’ rings particularly true.

Skilled individuals can handle additional themes, but even those have limits. So, be skeptical about Portfolio Managers, claiming to have hundreds of trades simultaneously. Discretionary portfolio managers operate their ‘concentrated’ / ‘high conviction’ portfolios with great pride.

For a systematic portfolio, diversification is not cognitively costly, a computer does not have the same limitations as a human being. But clients and individual researchers do. Systematic portfolios can contain several thousands of stocks and hundreds of macro markets and those ideas still must be managed, understood, and communicated to the clients.

Most systematic strategies focus on one theme, e.g. Trend Following, Value, Momentum, Statistical Arbitrage, Short Term Trading, etc. Not because it is right, but because it is the path of the least resistance.

Quantitative strategies are structured this way, not because of a lack of creativity, but because it becomes progressively more difficult to explain a complex concept to the end investor or understand it yourself.

The Tipping Stability Index

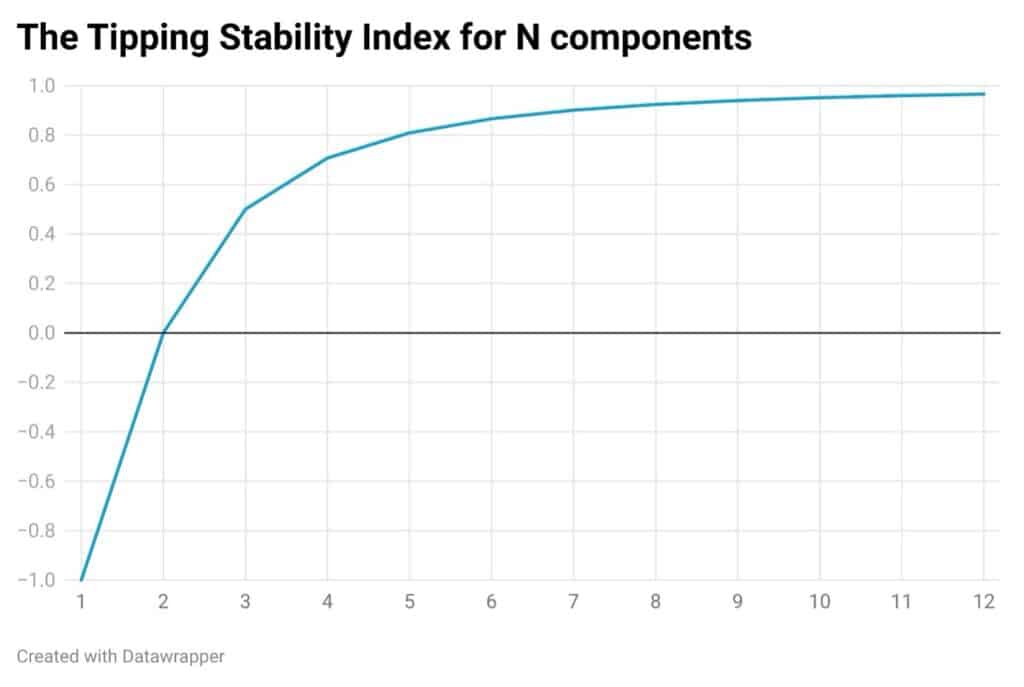

We design a measure that is both easy to understand and tries to answer the question, how many themes/ concepts/strategies should be in a portfolio? What should N be?

The TSI is an observable measure of robustness and borrows from the design of an everyday common item – the chair. A chair with one leg is not stable but cheap to make, a chair with an infinite number of legs would be rock solid, but not economical.

As it turns out, five is a number that balances the incremental stability of an additional leg, combined with production costs. Almost all office chairs have five different legs. An office chair is largely impossible to tip over [do not try this]and would probably remain stable even if one leg broke.

As it turns out there is a simple formula for calculating the stability of a chair with equidistant legs: cos(π/N).

For any N, this function is increasing, but at a declining rate. In the chart, we see that a portfolio with one strategy has negative stability, “anything that can go wrong will go wrong”. A chair with three legs has stability but is sensitive to losing a component and ending up in a state with no stability (N=2).

An office chair with five legs is stable and can lose one leg without crashing or coming close to being dangerously unstable. Adding additional legs improves stability, but the marginal benefit is lower.

From a financial perspective, the number of legs is the cross-correlation between different strategies (groups) and an assumption here is that they are perfectly uncorrelated. Otherwise, the legs of a chair will concentrate on one side of the chair. Naturally, this is not a stable chair.

The height can be viewed as an analog to portfolio risk. The higher the chair and lighter the base, the less stable the chair is.

1/N What is N?

Any reasonable portfolio solution should contain at least three independent assets/strategies. This number also comfortably fits into the working memory of most humans. A natural progression is that any theme can consist of sub-themes, which further improves the stability of the solution (ensure that those strategies are also uncorrelated).

Equal Risk ensures that the legs are the same length. The leverage needs to be adjusted for the center of mass of the portfolio. Too much leverage and it does not matter how stable your asset mix is.

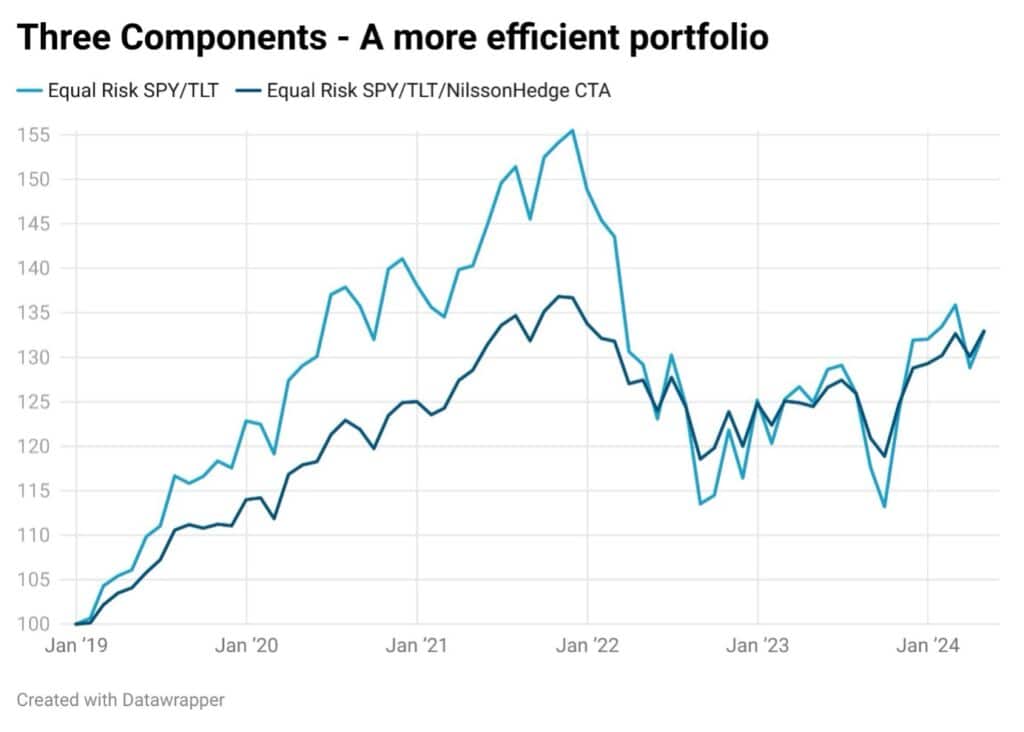

The ‘failure’ of the traditional bond/equity portfolios in 2022 was partly driven by the fact that the market changed. As the correlation shifted positive, the portfolio effectively turned into a one-legged chair. A TSI-based solution consisting of bonds, equities, and for instance, Managed Futures fared much better as seen in the chart. Substitute Managed Futures with your favorite uncorrelated strategy for similar results.

Summary

While the TSI is a simplification of how portfolios are constructed, it offers a minimum threshold to the

number of independent themes in a portfolio. Run a concentrated portfolio of three individual bets, you better have good backup ideas if one of them fails. If you are running a portfolio of three uncorrelated active sub-portfolios, you are likely in a better place.

A systematic strategy consisting of tens of uncorrelated strategies is in a better position to deliver a TSI-stable outcome. If nothing else, we hope that you checked the number of legs on your chair (we are almost certain it is five) but did not stress test the stability of your chair. Perhaps it is time to test the assumption in your ‘broadly’ diversified portfolio?

As with your chair, the key to a stable portfolio is finding truly uncorrelated strategies.

Bio: Linus Nilsson is the founder of NilssonHedge. He has served as the CIO and partner for a hedge fund, founded an emerging hedge fund, and worked as a hedge fund analyst for several international investors, and as a risk specialist for a major bank. He founded NilssonHedge, a database focusing on CTAs and other Liquid Alternatives. Nilsson has lived in six countries, published articles in industry journals, and appeared as a speaker and moderator at industry conferences. In academic terms, he holds two master’s degrees from the Chalmers University of Technology and Gothenburg University.”