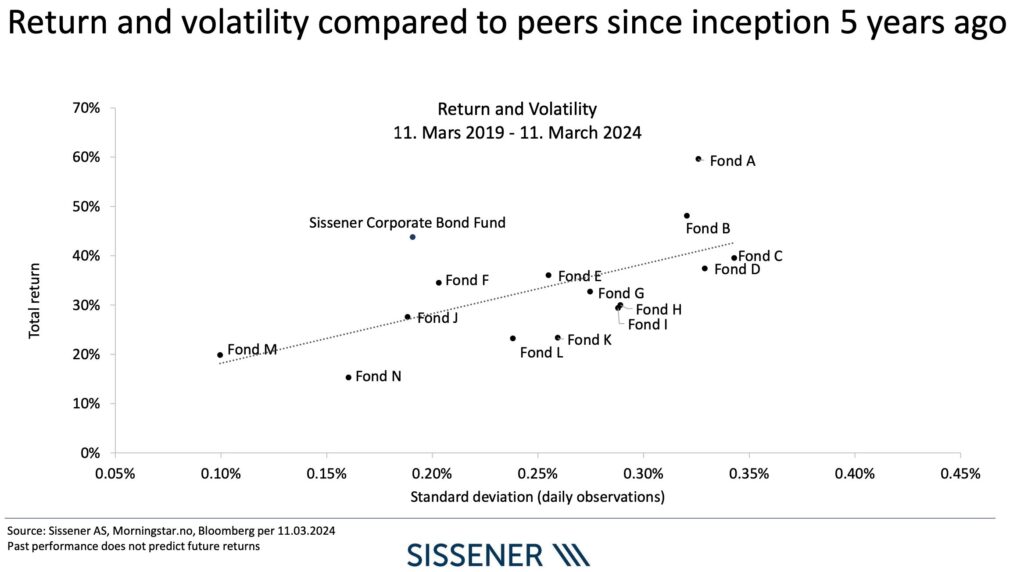

Stockholm (HedgeNordic) – Nordic high-yield-focused Sissener Corporate Bond Fund marked its five-year anniversary in March of this year under the guidance of Philippe Sissener. Following a decade of relatively tranquil markets, the fund entered the scene just as a series of unforeseen events began to unfold, including a pandemic, unprecedented fiscal stimulus, a war on European soil, sharply rising inflation, and consequent interest rate hikes, alongside a banking crisis and related repercussions. Despite the resurgence of uncertainty and volatility in the markets, Sissener Corporate Bond Fund managed to deliver an annualized return close to the top of its peer group, reaching 7.6 percent per annum during this five-year journey, while maintaining below-average volatility in returns.

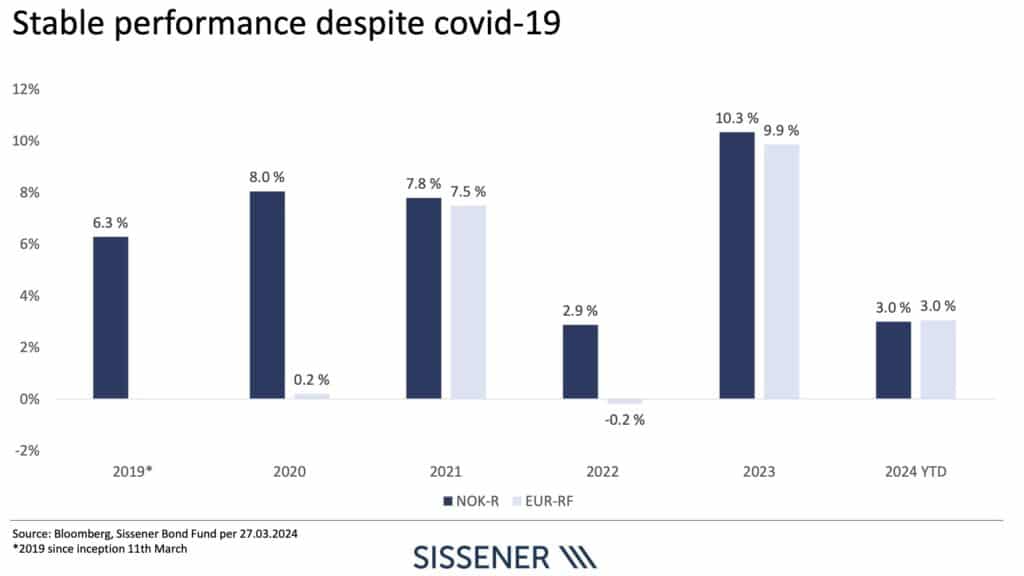

“It has been five interesting years,” states Philippe Sissener, who oversees the management of Sissener Corporate Bond Fund alongside a broader team at Sissener. “There have been five extremely different and challenging years in their own way,” he emphasizes. Sissener Corporate Bond Fund was launched on March 11 in 2019, which meant missing out on the rally during the first months of the year following the drawdown in the final quarter of 2018. “We missed the flying start of the year, but we still managed well in 2019,” reflects Sissener. After achieving a 6.3 percent gain through the end of the year, the fund encountered the “V-shaped” drawdown and recovery of 2020 triggered by the pandemic.

“It has been five interesting years. There have been five extremely different and challenging years in their own way.”

Philippe Sissener

“As things were running smoothly and spreads tightened going into 2020, we reduced our risk by shifting towards shorter-dated issues, along with maintaining a fair amount of cash and short-dated government bonds,” recalls Sissener. While the Sissener team could not have anticipated the onset of the Covid-19 pandemic and its repercussions on financial markets, the cautiousness reflected in its portfolio positioned the fund to “not only endure a fall of half the market decline, but also to recover faster than many peers.” The fund concluded 2020 in positive territory at 8.0 percent.

“2021 was also a weird year,” recalls Sissener, with “all this liquidity pouring in from different sources, including direct payments into people’s pockets in the United States.” This flood of liquidity fueled a recovery that “looked almost fake,” with the fund recording a gain of 7.8 percent. Subsequently, in 2022, Russia’s full-scale invasion of Ukraine, coupled with looming recession and inflation concerns, compounded challenges across most asset classes. Nonetheless, Sissener Corporate Bond Fund closed the year with a modest 2.9 percent gain, followed by a notable recovery of 10.3 percent last year. “During these two years, we experienced less decline than broader markets and recovered faster,” notes Sissener.

Despite navigating through various market environments and events, the high-yield-focused fund managed by Sissener has delivered an annualized return of 7.6 percent over its five-year journey with below-average volatility. This risk-return profile partly stems from the conservative approach reflected across Sissener’s product range, which also includes a long/short equity hedge fund overseen by Jan Petter Sissener.

The Origins of ‘Conservatism’ and Coupons as a Source of Returns

Jan Petter Sissener attributes the ‘conservatism’ style of Sissener Canopus to his aversion to risk and losing capital at his stage of life. On the other hand, Philippe Sissener draws inspiration from Howard Marks of Oak Tree, who previously stated, “if we avoid the losers, the winners take care of themselves.” Philippe Sissener applies this philosophy to the high-yield bond fund, acknowledging that while their caution may sometimes seem excessive, adhering to quality investments proves invaluable during market downturns.

“Maybe we are a bit too careful at times, but our focus on quality greatly benefits us in drawdown periods,” explains the portfolio manager. According to Sissener, outperformance in the high-yield bond market does not stem from “taking excess risk during bull markets.” Instead, “it’s more about avoiding major mistakes and significant drawdowns during bearish phases, as the bulk of our returns, around 90 percent, are derived from the coupons, with only ten percent attributed to price appreciation.”

“Maybe we are a bit too careful at times, but our focus on quality greatly benefits us in drawdown periods.”

Philippe Sissener

Philippe Sissener highlights that aside from being the primary source of returns for Sissener’s high-yield bond fund, coupons also provide a substantial buffer for potential mistakes. “Coupons also provide a cushion for mistakes, should mistakes happen,” notes Sissener. “While we work on avoiding mistakes altogether, it’s inevitable that some will happen in this asset class,” he acknowledges. Therefore, “investments yielding eight to nine percent provide managers like us with a great ability to absorb losses if errors do arise.”

Concentration and Focus on Public Issuers

The initial step taken by Philippe Sissener and his team to mitigate errors is to maintain a more concentrated portfolio, typically comprising 30 to 40 investments. “This level of concentration allows us to have relatively strict control of the risk, and at the same time, offers sufficient diversification that if we make a mistake, it will not hurt too much,” explains Philippe Sissener. More importantly, Sissener Corporate Bond Fund has a strong preference for bonds where the issuer is publicly listed. “We have often been following these companies for many years, and we find that they tend to have lower default rates and higher recovery rates given defaults,” notes the portfolio manager. Additionally, he highlights that publicly listed companies have an advantage in raising equity also in more challenging times.

“This level of concentration allows us to have relatively strict control of the risk, and at the same time, offers sufficient diversification that if we make a mistake, it will not hurt too much.”

Philippe Sissener

“Worst come to worst, should bonds need to be converted into equity, it’s reassuring to have a liquid instrument readily available,” emphasizes Philippe Sissener. Alongside the lower default rates and higher recovery rates associated with public issuers, the segment of issues from public companies also exhibits greater liquidity and transparency compared to those from private entities. “When investing in bonds from a private company, often only those investors participating in the capital raise monitor these bonds in the secondary market,” argues Sissener.

Accordingly, “liquidity is significantly better in the secondary market for public issuers, particularly as there’s broader interest in publicly listed companies.” Equally significant is the reduced information asymmetry between companies and investors among publicly listed issuers. “Lower default rates, higher recovery rates, better information transparency, liquidity in the secondary market, and access to fresh equity are the primary factors driving our preference for issues by public companies,” says Sissener.

Attractive Hunting Ground and Local Advantage

In addition to offering higher spreads versus other markets, the Nordic high-yield market offers several advantages over its European counterpart, for instance. Specifically, three characteristics contribute to its lower volatility: the absence of ETFs, shorter tenure, and the prevalence of floating structures. Philippe Sissener elaborates on the absence of ETFs, highlighting its positive impact on the Nordic high-yield market. “The lack of ETFs is beneficial for the Nordic high-yield markets because ETFs are often more liquid than the underlying securities,” he explains. “Large inflows or outflows from ETFs can excessively influence prices, resulting in unnecessary volatility.”

“This requires more local knowledge from investors, which is an advantage for players like us. It demands more thorough research on every loan. Therefore, we believe that having local knowledge is a significant advantage.”

Philippe Sissener

Furthermore, the shorter tenure of Nordic high-yield bonds, typically ranging from three to five years, contrasts with the longer durations prevalent in international markets, contributing to reduced volatility. “These shorter tenures imply shorter duration and consequently lower volatility,” notes Sissener. Additionally, the Nordic high-yield market is distinguished by the prevalence of floating-rate structures, further diminishing market volatility and providing an advantage in times of rising interest rates. “Floating rate notes resemble the loan market,” explains Sissener. “Every quarter, the coupon is reset based on benchmarks like EURIBOR or LIBOR, which effectively means that the issuers are carrying the interest rate risk, not the other way around.”

Another advantage for the Sissener Corporate Bond Fund and other active managers in the Nordic high-yield market is the absence of credit ratings, with less than one-fourth of the market having ratings. “This requires more local knowledge from investors, which is an advantage for players like us,” notes Sissener. “It demands more thorough research on every loan. Therefore, we believe that having local knowledge is a significant advantage.” Philippe Sissener concludes by saying that high-yield bonds can play an important role in an investor’s portfolio due to their potential for equity-like returns with a profile that can “diversify and limit duration in a fixed-income portfolio.”