Partner Content from CME Group – Today’s European money managers must be on the lookout for new ways to generate alpha in low-return environments, while nimbly navigating hairpin market turns from a 24-hour world news cycle. Uncleared Margin Rules have many institutions looking for ways to negate higher costs, such as switching to listed FX options. Portfolio managers must manage a slew of risks and new technologies while seeking greater cost efficiencies in ever-more-regulated, capital-constrained markets. To be successful requires a deep and comprehensive toolbox of the right tools, innovative strategies and a forward-thinking mind ready to learn.

This workshop provides a deep dive into how you can achieve just that using CME Group’s benchmark interest rate, equity index and FX derivatives products. Discover new ways to reduce existing and new margin requirements from Uncleared Margin Rules while freeing up credit lines, increasing cost efficiencies and maximizing your risk/return.

Who should attend?

Portfolio managers, research, trading and client facing professionals from pensions, asset management, and insurance firms as well as sell-side professionals from banks, broker-dealers and futures brokerage firms.

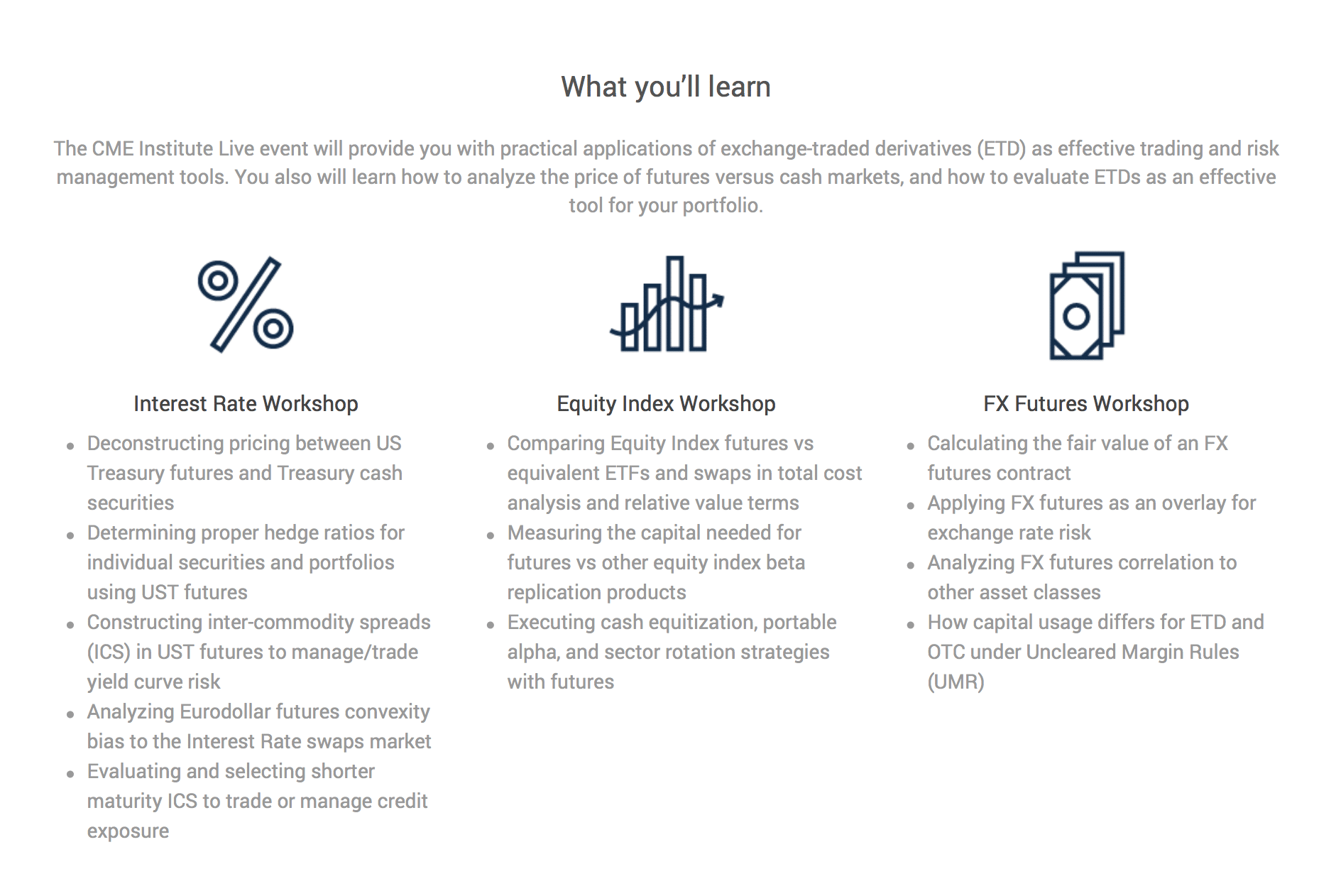

The CME Institute Live event will provide you with practical applications of exchange-traded derivatives (ETD) as effective trading and risk management tools. You also will learn how to analyze the price of futures versus cash markets, and how to evaluate ETDs as an effective tool for your portfolio.

Agenda

Day 1 │ Interest Rate Workshop |

|

9:00 – 9:30 |

Welcome

|

9:30 – 10:30 |

US Treasury Futures Foundations

|

11:00 – 12:30 |

US Treasury Futures Applications

|

12:30 – 13:30 |

Break, lunch provided |

13:30 – 14:30 |

STIRs Basics

|

14:30 – 15:00 |

Break |

15:00 – 16:30 |

STIRs Applications

|

Day 2 │ FX & Equity Index Workshop |

|

9:00 – 9:30 |

Welcome

|

9:30 – 11:15 |

FX Futures

|

11:15 – 11:30 |

Break |

11:30 – 12:30 |

Equity Index 1.0

|

12:30 – 13:30 |

Break, lunch provided |

13:30 – 15:00 |

Equity Index 2.0

|

15:00 – 15:15 |

Break |

15:15 – 16:45 |

Equity Index 3.0

|