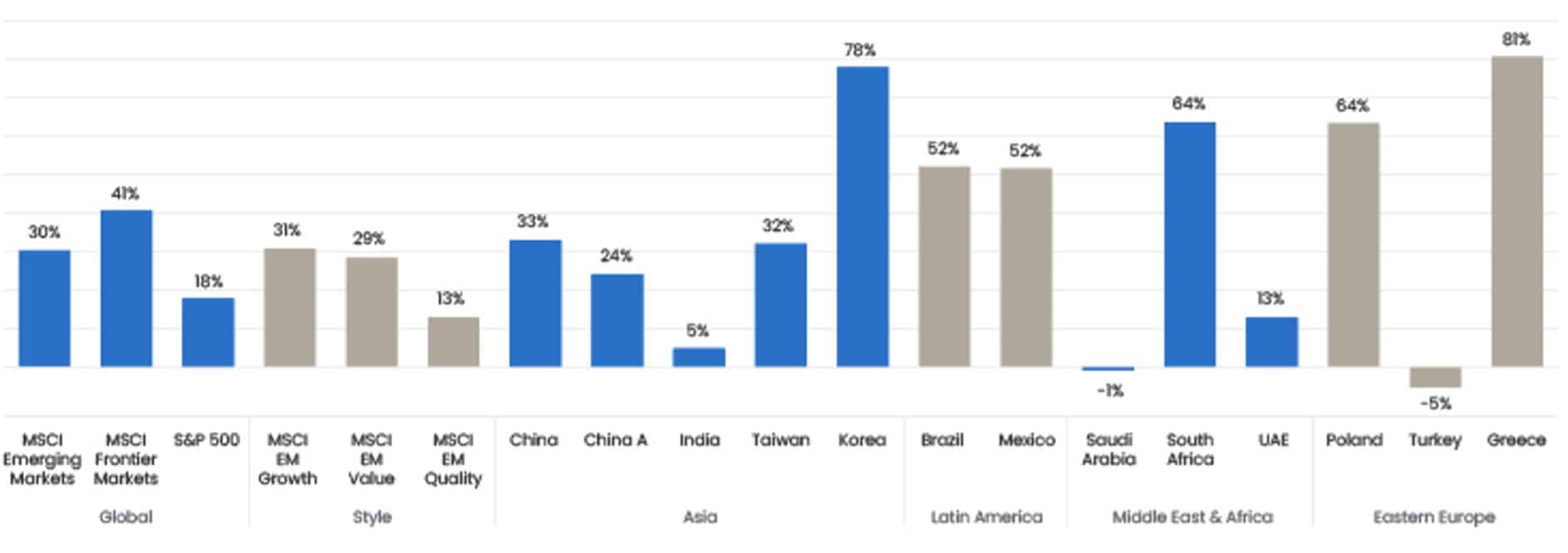

By Jacob Grapengiesser, David Nicholls and Peter Elam Håkansson at East Capital: 2025 was a fantastic year for emerging and frontier markets, which shrugged off trade tensions and geopolitics to deliver returns of 30% and 41% in USD terms respectively over the first 11 months (see Figure 1). We believe that 2026 will likely be another good year, thanks to a relatively benign macro backdrop characterised by falling rates globally and strong idiosyncratic stories across these markets, from reasonably priced AI enablers in Taiwan and Korea to underappreciated tech leaders in China to fast-growing structural growth stories in India and beyond.

Figure 1. Total return YTD in USD (%)

The great rotation begins?

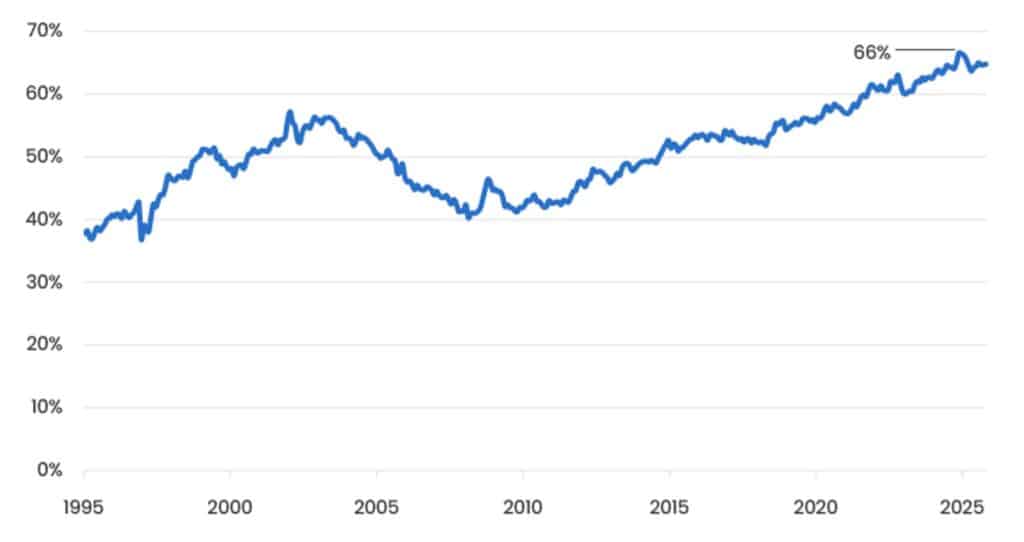

A major topic in 2025 was whether the “US exceptionalism” narrative had gone too far, with the US reaching 66% of global equity market capitalisation (see Figure 2) despite contributing just 26% of the global GDP. By contrast, emerging markets (EMs) comprise just 11% of the MSCI ACWI, yet they represent approximately 40% of global GDP and 70% of global real growth.

Figure 2. Weight of US in MSCI All-World (ACWI) Index

Fears of US exceptionalism are stoked by concerns about both the valuations and market concentration of US AI stocks as well as of USD exposure, particularly for non-US investors. Looking ahead, these issues are likely to persist. US stocks remain much pricier than those in other markets, particularly emerging and frontier markets. There are also real questions about whether recent US AI investments will pay off, and the US dollar is not expected to strengthen as the Fed continues to cut rates.

Indeed, over the next two years (see Figure 3), EMs offer slightly better growth (14.9% earnings CAGR over the two years vs 14.5% for the S&P 500) at considerably lower valuations. Consequently, the PEG ratio for EMs is just 0.9x, compared to 1.5x for the US and 1.3x for Europe. Our global EM strategy is cheaper than the benchmark, trading at 0.6x PEG, in line with our approach of finding underappreciated, fast-growing companies at reasonable valuations. Valuations in frontier markets (FMs) are even more appealing: our Global Frontier Markets fund trades at 0.4x PEG.

Figure 3. Key metrics for global indices and East Capital global strategies in 2026 and 2027

Despite the positive narrative, fund flows have not kept pace. Emerging market equities attracted only USD 21.5 billion in net inflows in 20251, leaving EMs at just 5.2% of global equity fund assets under management compared to their weight of over 11% in the MSCI ACWI. While this is a slight increase from the 4.9% recorded at the end of 2024, it remains below the 5.5% seen in 2023. This global data is consistent with our recent client discussions. The vast majority are “doing their homework” on EMs but generally remain underweight. For the long-term investors we speak to, the key question is not short-term upside, but whether EMs can deliver sustainable returns over time.

The macro backdrop looks benign

In general, on the macro side there have been three common concerns about emerging and frontier markets, namely that when compared to investors’ home markets in developed economies they have (1) more volatile and inefficient politics, (2) weaker and more reckless fiscal management and (3) depreciating currencies, which erode hard currency returns.

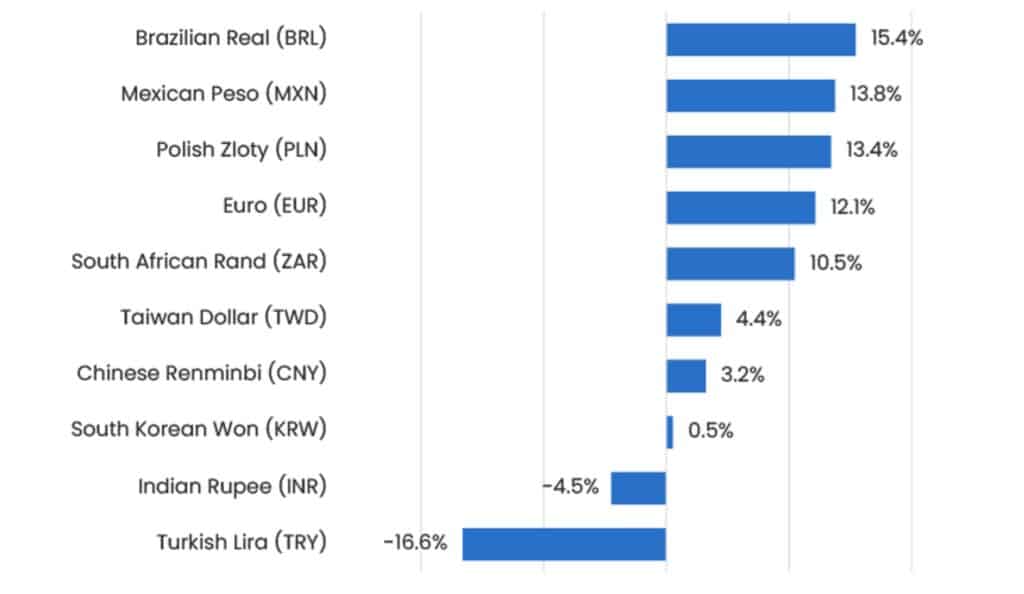

However, the last few years have started to dispel these concerns. The third concern is the easiest to disprove, as most currencies have appreciated against the USD in 2025 (see Figure 4). As Fed rates continue to fall going forward, the consensus is that the USD will continue to weaken, albeit perhaps at a slower pace than in 2025. Some market participants are even more optimistic: one well-regarded strategist has forecast that the renminbi could appreciate from 7 to 5 against the USD (i.e. strengthen by 40%!) over the next few years, driven by strong trade surpluses and broader adoption of the renminbi as a reserve and trade currency.

From a political perspective, the chaos in the US and the divisions within Europe suggest that the political environment in emerging and frontier markets may not be that bad on a relative basis. Investors in developed markets have a particularly negative perception of Chinese politics. While this is not entirely unjustified, China’s focus on cutting-edge technologies and their supply chains – such as rare earths mining and processing is underpinned by stability and long-term thinking, and this does appear to be a winning formula that other countries are now seeking to emulate, albeit belatedly. Furthermore, China’s “innovate first, regulate later” approach contrasts starkly with that of the EU and, to some extent, the US. This gives China a clear advantage in technologies such as self-driving cars, AI, robotics, biotech and medicine (such as stem cell therapy).

In fiscal terms, with the US running deficits above 8% of GDP, it is not a big leap to suggest that emerging and frontier markets don’t look so bad. Indeed, successive crises have prompted many EM and FM countries to improve fiscal discipline, with the aggregate fiscal deficit for EMs forecast at around 4.2% of GDP in 2026. This deficit appears manageable, especially given lower debt levels of 72% of GDP for EMs versus 110% for developed markets, according to the IMF.

Risks

After nearly three decades of investing in emerging and frontier markets, we have learned to “expect the unexpected”. Current conditions resemble a classic late-cycle environment, which has been extended by the AI boom. Stretched valuations and significant retail participation are driving markets higher across the world. Naturally, this increases the risk of something going wrong.

However, the most significant risk for emerging and frontier markets is the possibility that the US economy surprises and picks up again in 2026. This could revive the “US exceptionalism” narrative and take the expected Fed interest rate cuts off the table.

Geopolitical risks are likely to persist, but after a year of intense geopolitical unrest, it is quite difficult to see how things could deteriorate much further, particularly relative to events such as Trump’s “Liberation Day” in April.

Conclusion

We believe that 2026 has the potential to be another good year for EMs and FMs. This is supported by favourable valuations, light positioning, a strong macro backdrop and a wide and diverse range of growth drivers. In many ways, we believe the main appeal of EMs lies in their diversity. On a simplistic level, you can split the market into:

- 1/3 AI “picks and shovels” in Taiwan and Korea.

- 1/3 China: the vast majority of companies would be Chinese or global technology leaders, spanning everything from EVs and batteries to electricity meters and dental implants.

- 1/3 uncorrelated company-specific growth stories, such as those in India or Brazil.

Unlike investing in the US, investing in EMs does not require you to put all your eggs in the AI basket. However, a shift has taken place and EMs are no longer just about economic convergence and consumption growth stories.

Frontier markets are in a category of their own and remain totally overlooked by the vast majority of investors. However, for the more adventurous of us, there are extremely appealing valuations, strong opportunities and lower volatility, particularly when blended within a broader portfolio.

The full East Capital Outlook 2026: Why invest in emerging and frontier markets in 2026? can be accessed here.