By Christian Munafo – Liberty Street Advisors: Many investors have legitimate concerns regarding potential impacts of both recent tariff announcements made by the US and initial responses from other countries. While we cannot be certain of the ultimate outcomes, we continue to believe that private markets can provide investors with numerous benefits including volatility reduction, diversification, enhanced return potential and access to opportunities that have been historically unavailable in public markets. We think this particularly holds true with strategies like ours that focus on investment opportunities in late-stage, high-growth private technology companies that drive innovation and disruption across the economy in sectors such as aerospace/space economy, cybersecurity, artificial intelligence (AI)/machine learning (ML), big-data/cloud, advanced manufacturing, fintech/digital assets, digital health, ecommerce and agricultural technology.

We are closely monitoring how current market dynamics evolve and believe there could be some near-term disruptions to capital formation and exit activity due to increased volatility and macro-uncertainty, but we anticipate a resurgence of activity and improving sentiment in the second half of 2025. In parallel, we believe there will continue to be attractive investment opportunities in high performing companies due to these dislocations which could potentially generate outperformance in the future, but investors must be disciplined and highly selective.

Capital formation

The National Venture Capital Association (NVCA) reported approximately 3,003 US Venture Capital (VC)-backed deals closed in the first quarter of 2025, with an aggregate deal value of USD 91.5 billion. This represents an 11% increase in the number of deals and an 18% increase in deal value compared to the first quarter 2024. Larger deals represented a greater share of activity with 10 transactions exceeding USD 500 million, accounting for over 61% of total VC investments. Excluding OpenAI’s USD 40 billion capital raise that closed in March, the other nine deals represent 27% of the total.

According to various sources, VC dry powder now sits at roughly USD 290 billion, but there remains a significant supply/demand ratio imbalance as more companies seek capital and shareholders seek liquidity, while investors exhibit greater discipline. As a result, this creates greater negotiating leverage for active investors willing to commit capital in both secondary transactions and new financing rounds. That said, high-performing companies demonstrating strong operating metrics will continue to be rewarded with more attractive valuations.

While current macro-uncertainly may impact the velocity of new company financings in the near term, we think it is important to be reminded that these are often attractive periods for capital deployment as investors gain negotiating leverage due to various macro and micro dislocations.

The stars are aligning for deals

We are looking at one of the largest and most compelling initial public offering (IPO) backlogs in recent history, with many high-performing technology and innovation companies generating a healthy balance of strong growth rates and profitability. For example, in January 2025, space and defence solutions company Voyager Technologies filed its confidential paperwork for an IPO and eventually raised $382.8 million in its U.S. initial public offering in June, while Meta signed on as an investor to data analytics software leader Databricks as it reportedly inches towards its widely anticipated IPO. In addition, AI chipmaker Cerebras announced Committee on Foreign Investment in the United States (CFIUS) clearance in March 2025, a key step toward its planned IPO.

In April, the gaming-focused social messaging service Discord announced the hiring of former Activision Blizzard Vice Chairman as its new CEO in advance of its expected IPO. Despite the challenging environment, AI cloud computing firm CoreWeave went public in March, largely driven by increasing demand for compute and inference capabilities required by large language models (LLMs), marking the largest tech IPO in years. Although Coreweave’s IPO priced at the low end of the predicted range, the stock initially surged and has held on fairly well despite subsequent tariff related headwinds.

Additionally, we are seeing increased merger and acquisition (M&A) activity involving VC-backed companies. According to Pitchbook, exit activity for the first quarter of 2025 reached the highest quarterly levels since Q4 2021, generating USD 52.6 billion across 385 deals. While we continue monitoring tariff developments and potential implications, we believe increases in corporate M&A activity and private equity (PE)-led buyouts can continue throughout 2025. In March 2025, Google announced an agreement to acquire cloud security company Wiz for USD 32 billion, marking Google’s largest ever acquisition. Also in March, Elon Musk’s AI company, xAI, acquired X (formerly known as Twitter) in an all-stock transaction valued at UAD 33 billion (net of debt).

Although tariff-related uncertainty may temporarily delay new listings and M&A activity in the near-term, we expect to see a pickup in both public market offerings and deal activity over the coming quarters as volatility subsides and headwinds calm.

Valuation trends

While public company valuations have recently pulled back due to the aforementioned macro-headwinds, we continue to observe a significant gap when comparing the valuations of our private companies with their public market equivalents. Public market comparables are just one of many inputs in our valuation framework for private companies. For instance, movements in public cybersecurity companies can affect our private cybersecurity valuations. Similarly, exit comparables, such as Google’s acquisition of Wiz also serve as new valuation inputs. Other factors include private rounds of financing, secondary transactions and employee stock option issuance.

Despite the resilient operating performance of most of our companies with record levels of revenue and profitability exhibited across the current portfolio, many are still valued below their last round of financing due to various depressed valuation inputs referenced above. We believe this represents significant embedded value potential for harvesting as market conditions and underlying valuation inputs improve.

Measuring potential tariff-related impacts

Since the inception of our strategy over a decade ago, the overwhelming majority of our holdings have involved US-domiciled companies where the underlying technology, operations and revenue primarily (if not exclusively) reside in the US.

While several of our holdings have asset-heavy business models including those in aerospace/space economy, most involve asset-lite business models with very little (if any) debt on their balance sheets. By default, these companies are typically not engaged in the traditional importing and exporting of hard assets.

Although we believe the capital structures and business models of many of our holdings provide a layer of protection from the newly proposed tariffs, there will likely be some degree of both direct and indirect impacts at a macro and micro level. For example, an extended period of increased volatility and uncertainty may hit growth rates as customers pull back on consumption and spend. Furthermore, companies with less flexible supply chains may face cost increases that cannot be fully passed on to their customers, which would hurt margins and profitability.

In addition, potential disruptions to capital formation and exit activity will likely force companies to manage their balance sheets and expenditures more efficiently while further delaying realisations for shareholders and investors. Related to this, US companies may see less demand from foreign investors as the demand for dollar-denominated assets could decline.

AI: The rise of DeepSeek

A major development this year was the introduction of the DeepSeek model from China, which received significant global attention with initial data indicating far greater efficiency compared to major LLMs. While the initial data is impressive, it is important to note that DeepSeek’s R1 model was trained by leading LLMs and offers narrower, distilled modelling capabilities. What may not be widely known is that DeepSeek leveraged Cerebras’ technology to achieve processing speeds 57 times faster than the most advanced graphics processing units (GPUs) currently available with greater energy efficiency. We believe these efficiencies will accelerate AI adoption across sectors.

This development shows that AI does not always require expensive, comprehensive models. Distilled versions can accomplish specific tasks effectively. While we believe differentiated LLMs like xAI are well positioned to continue benefiting from the often referred to Fourth Industrial Revolution or Industry 4.0, this shift allows us to move from AI enablement to companies facilitating and more broadly adopting AI, which should also bode well for companies such as Databricks for increased data warehousing and analytics, Nanotronics for defect-free chip manufacturing with AI driven inspection and process control, and Cerebras for more powerful and energy efficient computing solutions.

We already see a progression from companies enabling AI to those adopting it at more attractive price points. This shift is likely to foster sustainable business models around AI adoption. However, we advocate patience and discipline when it comes to investing in this area as certain aspects remain nascent and vulnerable to disruption. We continue to believe in the tremendous demand for AI compute, datacentres/infrastructure, and energy solutions, and are exploring these areas with great interest.

Broadening accessibility to private markets

More asset managers are launching strategies like ours that broaden investor accessibility, something that we have been strongly advocating and offering for the past decade. We believe this is largely driven by a combination of increased demand from non-institutional channels seeking better diversification and an interesting dynamic in which institutional investors are increasingly overexposed to illiquid assets due to a lack of exit/distribution activity. The former provides an exciting opportunity to engage with retail and wholesale investors that have historically been unable to access these types of strategies, while the latter creates an attractive investment opportunity for groups like us to purchase securities in high performing assets from fatigued investors and shareholders often at dislocated prices.

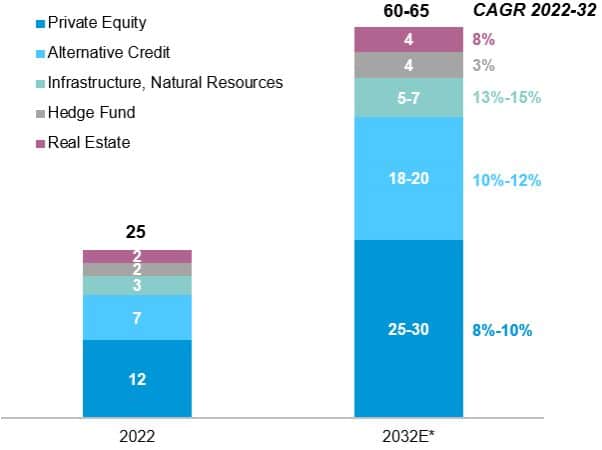

Setting the current macroeconomic environment aside, significant global growth across various alternative asset categories is expected for the foreseeable future (with PE accounting for lion’s share) as both institutional and non-institutional investors continue seeking strategies outside of traditional public equity and fixed income.

Chart 1: Global alternative assets under management (AUM), USD trillions

While recent tariff announcements are certainly raising new questions, challenges and concerns for the broader economy and both public and private market investors alike, we think it is important to be reminded that these are often attractive periods for capital deployment as investors gain negotiating leverage due to various macro and micro dislocations. As long-term investors focused on private innovation companies that improve efficiency, productivity and ultimately profitability for end customers across many sectors of the economy, we continue to believe that our underlying portfolio is well-positioned to benefit as capital formation, valuation and exit activity improve.

Everything we mentioned requires a lot of education, and that is what we are also aiming to do – educate the market.

This article features in the “2025 Private Markets” publication.