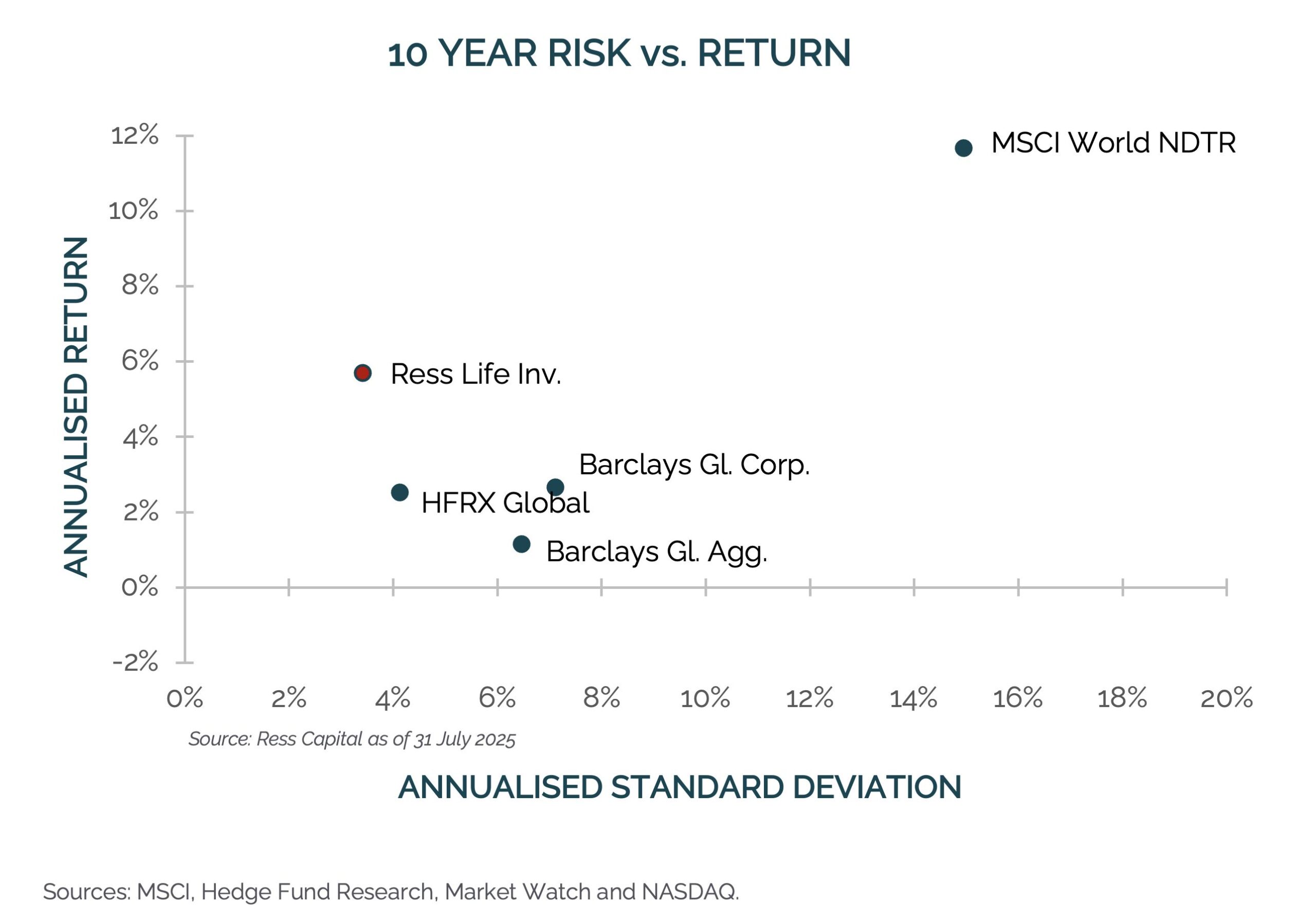

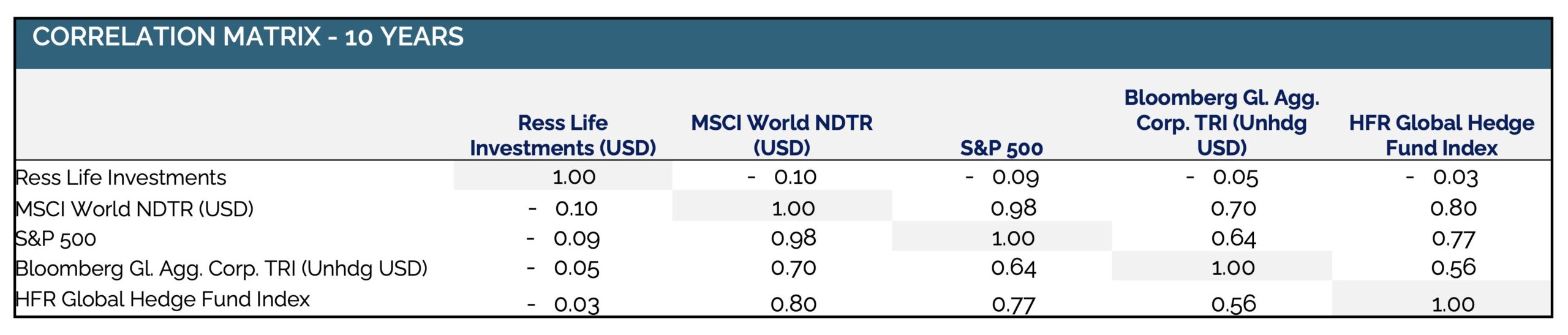

In the decade leading up to 2023, Ress Life Investments generated annualized returns in excess of 6 percent in a persistently low interest rate environment by investing in U.S. life insurance policies, also known as life settlements. The strategy effectively served as a fixed-income substitute, offering income with low correlation to traditional asset classes and limited downside risk. The subsequent rise in interest rates has altered the return dynamics, improving the forward-looking opportunity set despite near-term valuation headwinds. In response to growing European demand, Ress Capital, which recently merged with Finserve Nordic, is now launching a euro-denominated feeder structure.

The existing listed fund, Ress Life Investments, acquires life insurance policies from policyholders in the U.S. secondary market at a discount to their expected payout. In doing so, the manager assumes responsibility for ongoing premium payments and receives the full death benefit when the insured event occurs. During the low-rate era, Ress Life Investments typically acquired policies with internal rates of return between 10 and 12 percent, translating into a stable, uncorrelated return stream of around 6 percent annually after fees and costs.

The opportunity set improved markedly in the environment of higher interest rates. “We are now buying policies with IRRs between 15 and 25 percent,” says Andreas Julin, Head of Sales and Marketing after the merger between Ress and Finserve. “The main reason is the increase in U.S. interest rates following Covid and the energy crisis after Russia’s invasion of Ukraine.”

Dislocation Drives a Stronger Opportunity Set

Valuing a life settlements portfolio is fundamentally a discounted cash flow exercise under uncertain timing. Life expectancy determines duration, discount rates drive valuation, and policy payoffs define terminal value. While higher rates reduce the present value of future payoffs, they have also reshaped market dynamics in ways that have improved entry points for managers such as Ress Life Investments.

This shift has been driven in part by structural pressures across the market. “Many US-based managers used leverage in this asset class when rates were low. When rates increased, they faced higher financing costs and liquidity pressure,” explains Julin. At the same time, these managers needed liquidity to continue paying premiums. “As a result, many managers stopped buying policies and started selling them, creating a supply-demand imbalance that pushed IRRs higher,” he adds.

“Last year was a transition year with moderate returns, but this was done to improve long-term performance.”

Jonas Mårtenson

Private equity investors, previously active in the space, “have also been less active due to capital constraints,” while demographic trends, combined with inflation and rising living costs, have increased policyholders’ willingness to sell, further expanding the supply of policies. “All of this has created attractive opportunities,” summarizes Julin. Against this backdrop, the team behind Ress Life Investments made the strategic decision to exit its legacy portfolio at net asset value and redeploy capital into policies with materially higher implied yields.

Following a return of just under 2 percent in 2025, founder Jonas Mårtenson describes the period as transitional. “Last year was a transition year with moderate returns, but this was done to improve long-term performance.” The expected return over the coming five-year period is now around 10 percent annually. The portfolio rotation is expected to be completed later in 2026, with returns expected to reach the new target from 2027 onwards. “We are still deploying capital and expect to be fully invested by the third quarter,” he adds.

Evolving Portfolio Construction

When Ress Life Investments launched in 2011, the strategy focused primarily on acquiring individual policies, with the initially built portfolio taking two to three years before generating payouts and delivering returns to investors. With a significantly larger asset base today, the asset manager has been rotating the portfolio by acquiring both individual policies in the secondary market and existing portfolios, or pools of policies, in the tertiary market.

“We use a combination of individual policies and portfolios of policies,” says Julin. “Individual policies have longer life expectancies, which helps mitigate longevity risk.” Portfolio acquisitions, by contrast, consist of more seasoned policies with shorter durations, typically maturing within five to ten years. “This allows us to balance long-term returns with nearer-term cash flows. Our goal is for performance to be driven by payouts rather than valuation.”

“Previously the return differential was limited. Now, if we achieve a 10 percent return and rates are around 3.5 percent, the return differential is approximately 650 basis points, which is very attractive, especially given the uncorrelated nature of the strategy.”

Andreas Julin

Over its 15-year history, including both ramp-up and transition periods, Ress Life Investments has delivered returns more than four percent, with low correlation and limited downside. Still, in absolute terms, “our main competitor for the strategy is U.S. interest rates,” notes Julin. “Previously when rates were 5.25 percent and our return target was 7 percent, the return differential was limited,” he adds. “Now, if we achieve a 10 percent return and rates are around 3.5 percent, the return differential is approximately 650 basis points, which is very attractive, especially given the uncorrelated nature of the strategy.”

Broadening Access Through a Euro Feeder

The improved return profile, combined with investor demand and increasing caution toward U.S. dollar exposure, has prompted the launch of a euro-hedged feeder, Longevity Strategy Fund. “The simple answer is that many European investors have been quite bearish on the US dollar,” explains Mårtenson. “We have many European investors who like the life insurance strategy because it is uncorrelated and not exposed to geopolitical risks. However, the strategy has so far been in U.S. dollars. That is the main reason for setting up this euro-hedged feeder.”

“We have many European investors who like the life insurance strategy because it is uncorrelated and not exposed to geopolitical risks. However, the strategy has so far been in U.S. dollars. That is the main reason for setting up this euro-hedged feeder.”

Jonas Mårtenson

The new vehicle has been seeded with approximately €25 million from a European multi-family office. While returns will be modestly lower due to the interest rate differential between the euro and the U.S. dollar, the structure incorporates fee adjustments for initial investors to offset hedging costs. “Euro interest rates are currently around 2 percent, while U.S. policy rates are approximately 3.5 percent, implying a differential of roughly 150 basis points, which effectively represents the hedging cost,” explains Julin. “However, the fixed management fee in the Longevity Strategy Fund is slightly lower for initial investors, which compensates for that difference.”

From an asset allocation perspective, Ress Capital frames the strategy as a defensive growth component within a broader portfolio. “It offers equity-like returns with no correlation to other asset classes,” says Julin. Unlike other uncorrelated strategies such as catastrophe bonds, which carry downside risk, “this strategy offers upside volatility driven by payments,” he adds. “This return profile is very, very rare.”

Credit risk, meanwhile, is limited. “We invest only in policies issued by investment-grade U.S. life insurance companies, with at least an A-minus rating. These are very solid institutions,” explains Mårtenson. As a result, the primary risk factor is longevity risk, which also underpins the strategy’s lack of correlation to broader markets.

“We invest only in policies issued by investment-grade U.S. life insurance companies, with at least an A-minus rating. These are very solid institutions.”

Jonas Mårtenson

With the portfolio rotation nearing completion, Ress Capital is set to return to a more normalized return profile while maintaining its long-standing buy-and-hold approach. “The strategy has been buy-and-hold for many years, and we expect to continue with that approach,” says Mårtenson. “We may sell policies opportunistically, but generally it will remain buy-and-hold.” At the same time, the introduction of the euro-denominated feeder broadens the strategy’s accessibility to a wider investor base. “The euro feeder allows us to reconnect with investors who liked the strategy but did not want exposure to the U.S. dollar,” Mårtenson concludes.