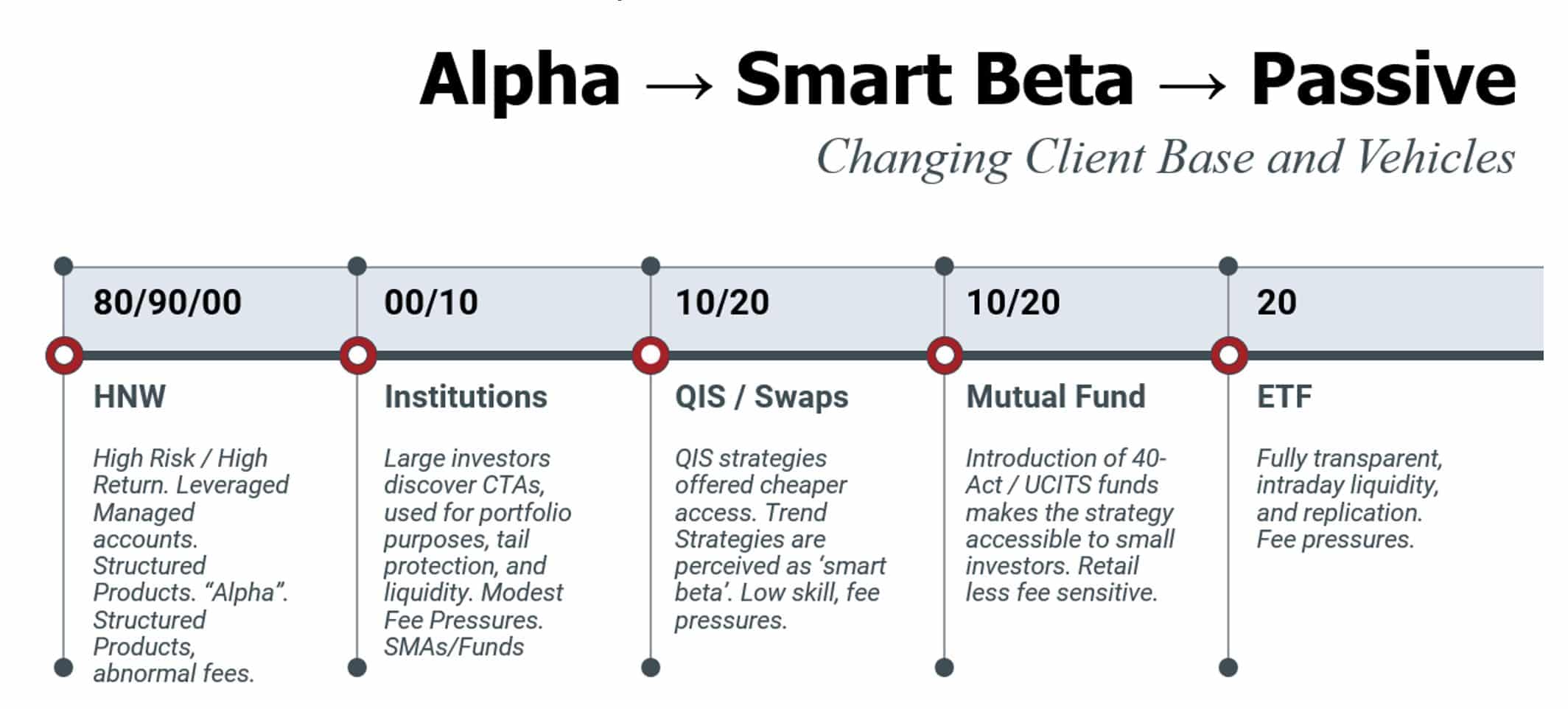

By Linus Nilsson of NilssonHedge: In the beginning, CTAs were a cottage industry, focusing on HNW, seeking outsized returns, and deploying notionally funded managed accounts. The industry gradually became institutionalized, and managers over time shifted their focus from maximum returns to risk-adjusted returns. Regulatory innovations and market conditions both closed and opened up new structures for different client groups. Consequently, Trend Following managers have gone through an evolution in terms of distribution mechanics and investor base. ETFs are one of these latest distribution innovations. ETFs is, in our view, are the first step in creating a passive exposure to the strategy.

In this article, we illustrate that this development has not had a negative impact on the overall investor base. Higher liquidity and equivalent returns, often coupled with lower fees, for instance, have been beneficial to investors. On the flipside, this evolution may also create the downfall of many CTAs and make it impossible to successfully establish another, new Trend strategy. Trend Following Hedge Funds may face the same competitive pressures as Long Only Stock Pickers.

As with the large S&P 500 ETFs, once you have a passive alternative, this evolves to the go-to alternative for allocators. And then it becomes a battle for the extra basis points you can extract. The cheapest product takes it all. Trend-followers may now be approaching a similar inflection point. The very innovations that broaden access and improve efficiency for investors could simultaneously erode the economic viability of launching and sustaining new managers.

Alpha → Smart Beta → Passive

To illustrate these dynamics, we analyze a subset of the NilssonHedge Indices, which provides additional perspective on the broader performance. These indices represent averages, and it is important to note that individual fund performance, whether better or worse, does not invalidate the structural observations presented here.

Trend-based strategies do not only face competition from other managers. In the 2010s, post the stellar success of CTA in 2008, banks started offering Quantitative Investment Strategies (QIS), often mimicking trend following. Given the more institutionalized approach and well-established indices, fee compression was a key selling point. QIS strategies certainly offered cheaper headline fees (although the devil was in the details).

At this point, from an institutional perspective, Trend Following was largely a Smart Beta strategy that could be allocated to within a strategic asset allocation. Purchased from a provider, regardless of whether that was a hedge fund or a bank.

As regulatory innovation took place, new distribution channels opened up. Starting with the Rydex Managed Futures Fund in 2007, retail investors could access the strategy through commingled funds. UCITS structures followed in the mid-2010s. This evolution made it possible for banks and asset allocators to allocate trend-based exposure into their products, effectively without any minimum allocation.

Today, trend-following strategies can be accessed in increasingly granular formats, via mutual funds and, more recently, ETFs. In effect, the strategy has become “tokenized”. Liquid, divisible, and easily embedded across portfolios.

Importantly, the fee compression observed in institutional mandates has partially flowed through to the retail segment. As the most egregiously priced products have been competed out (there were plenty of them), retail investors can now access CTA-like exposures at fee levels below 100 basis points.

They Came, They Saw, They Conquered

We focus on a subset of the NilssonHedge CTA-specific indices to better understand which segments of the strategies have ultimately benefited from the industry’s evolution.

Our Daily CTA Index, live since 2019, provides daily estimates of industry performance. The index predominantly consists of mutual funds, primarily 40-Act vehicles. and incorporates multiple share classes to present a more representative and balanced return profile. In 2026, we launched a copycat of the Daily CTA index, exclusively focused on the Managed Futures ETFs.

To study the liquidity effect, we evaluate the Daily CTA Index against the NilssonHedge Systematic Momentum Index and the NilssonHedge Systematic Index. As the names imply, these indices capture different segments of the systematic investment universe, with varying degrees of trend exposure.

Here, we note the slightly surprising fact. The Daily index outperforms the average of the managers that are only offering their strategy through a regular fund structure. The difference is modest, and on a risk-adjusted basis, the picture is somewhat more muddled.

Ex-ante, one might have expected a negative selection bias within the Daily CTA Index. Historically, this dynamic was evident on managed account platforms. They offered superior liquidity, but the manager lineup often skewed weaker. Many top-performing CTAs had little incentive to accept the associated constraints (or fee sharing) when capital was readily available elsewhere.

The above may reflect that it is more difficult to charge performance fees in Mutual Funds (and ETFs). The broader implication is clear: increased liquidity does not appear to be a structural drag on performance. For investors, this is an unambiguously positive outcome.

What About the ETFs?

In Jan 2026, NilssonHedge started tracking the expanding Managed Futures ETFs as a separate composite. Due to a lack of history, we backtracked data for 2025, with the same constituents as in 2026. Any fund launched throughout 2025 will enter at launch. We believe that this is a fair representation of the results.

The intraday liquidity or transparency does not seem to impose a performance drag. The difference is hardly significant, and we would require more data to understand if they are the same or if the indices are statistically different. It is, however, in the general direction that ETFs are cheaper than the funds in the Daily CTA indices.

We expect the performance edge to be variable, but that lower fees are a structural edge and that ETFs will gradually win out, unless fees for the funds in the original index are adjusted downward. Dispersion remains high across the different constituents. There is still a common risk factor that is extracted across the strategies when aggregated across managers. And before you ask, yes, the indices used here are also highly correlated to other industry benchmarks.

Creative Destruction

In equities, it is ‘easy’ to create a passive benchmark. With Trend Following strategies, it has proven more elusive. To fully design a “passive trend following strategy”, you need a benchmark, preferably with a well-defined process. Many have tried, and none have succeeded, largely because they have attempted to write systematic trading rules. This often fails as it is difficult to define signals, risk management, and portfolio construction in a sufficiently generic manner.

ETFs offer a different path. Through position disclosures, they make trend following observable. Importantly, most assets are concentrated in funds that trade slowly and across a limited set of markets. This makes their portfolios sufficiently stable to approximate and aggregate. This effectively commoditizes trend following strategies. The relative slowness makes the aggregated positions suitable for outside aggregation.

An investor could thus aggregate ETF holdings and publish an investable index. This would not be a passive benchmark in the strict sense of the S&P 500, but rather an observable proxy for long-term trend exposure. It would rely on outsourced decision-making rather than a predefined rule set.

ETFs still represent a small share of total CTA assets (less than 5%), but they are becoming an efficient access point for both retail and institutional investors.

For managers, the trade-off is clear. The ETF structure improves distribution but increases transparency, making strategies easier to approximate. This shifts competition toward cost and scale, reducing the scope for undifferentiated offerings.

The outcome favors investors through lower costs and greater access. For managers, it raises the bar for differentiation. As in Equities, the industry may converge to a single dominant provider. Long-term trend exposure is likely to become even more commoditized. Institutional investors may opt for in-house solutions, unless fees offer competitive economics.

While ETF solutions are on winning streak, they may also create a winner’s curse and a race to the bottom. Investors will thank you though.