By Alexander Mende and Per Ivarsson at RPM Risk & Portfolio Management: Traditionally, Managed Futures (MF) strategies have been limited to hedge funds known as CTAs. However, in recent years, Managed Futures ETFs (MF ETFs) have transitioned from a niche alternative strategy to a recognized tool for portfolio diversification and “crisis alpha”. Although MF ETFs have experienced significant and rapid growth, to roughly USD 6 billion as of March 2026, they only hold a very small share of the total ETF market (around 0.05%). The industry is also tiny compared to the overall CTA industry, which exceeds USD 300 billion.

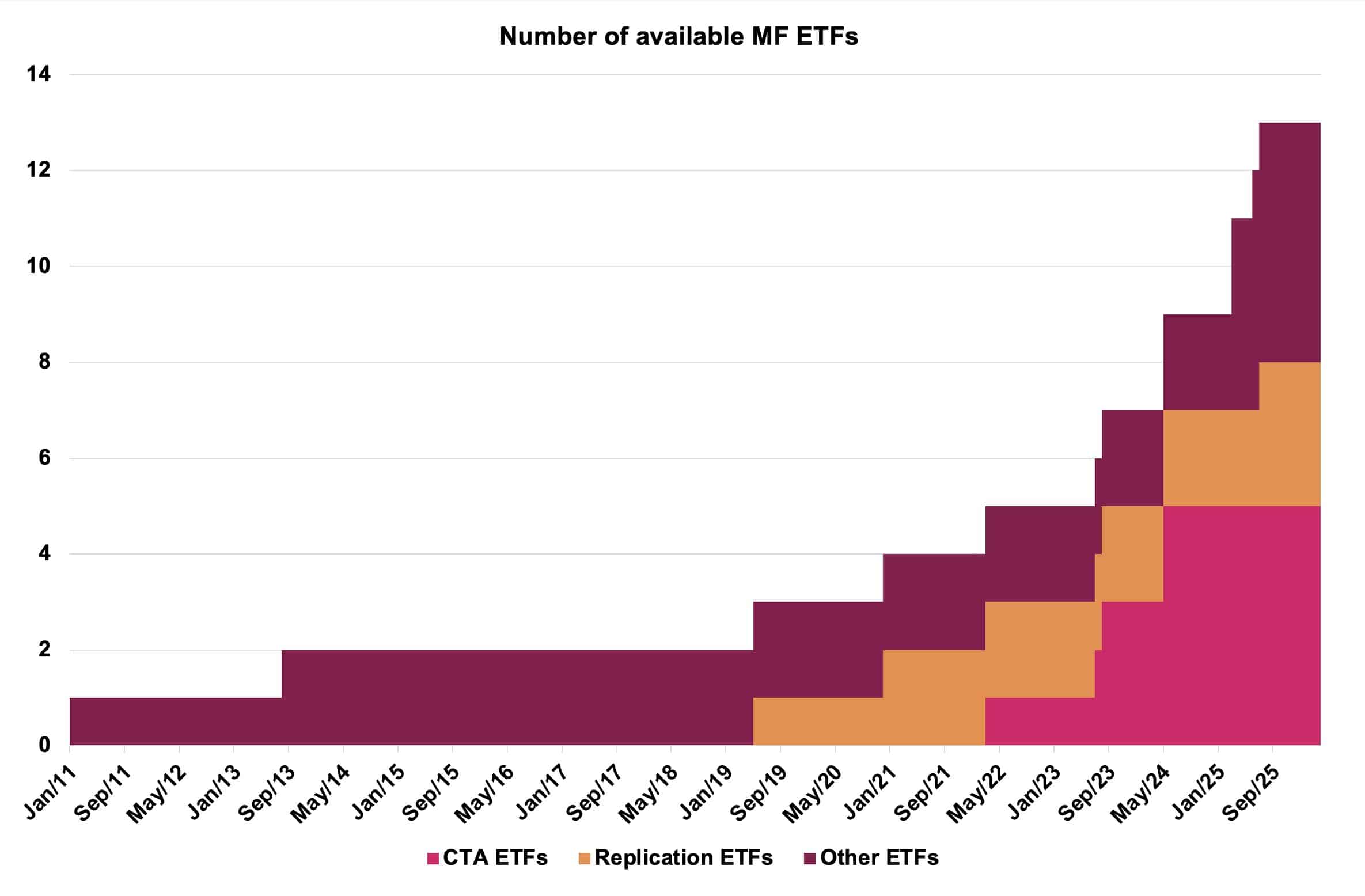

To the best of our knowledge there are currently 13 available MF ETFs, if you avoid double counting (Figure 1). We have roughly categorized them according to provider and underlying investment process, i.e., first, ETFs set up in cooperation with “real” CTA managers who also run their full programs in a fund and/or on a managed account basis. The ETF versions typically trade fewer markets, but the trading and portfolio process is similar to the original program and primarily signal driven, we simply call them CTA. Second, replication strategies, mirroring a trend following index where the trading process is either signal- or regression-based, we call them REPL. Third, other signal-based ETFs set up by (large) financial institutions that – prior to launching an MF ETF – had no business activities in the CTA or trend following space, we call them OTHER.

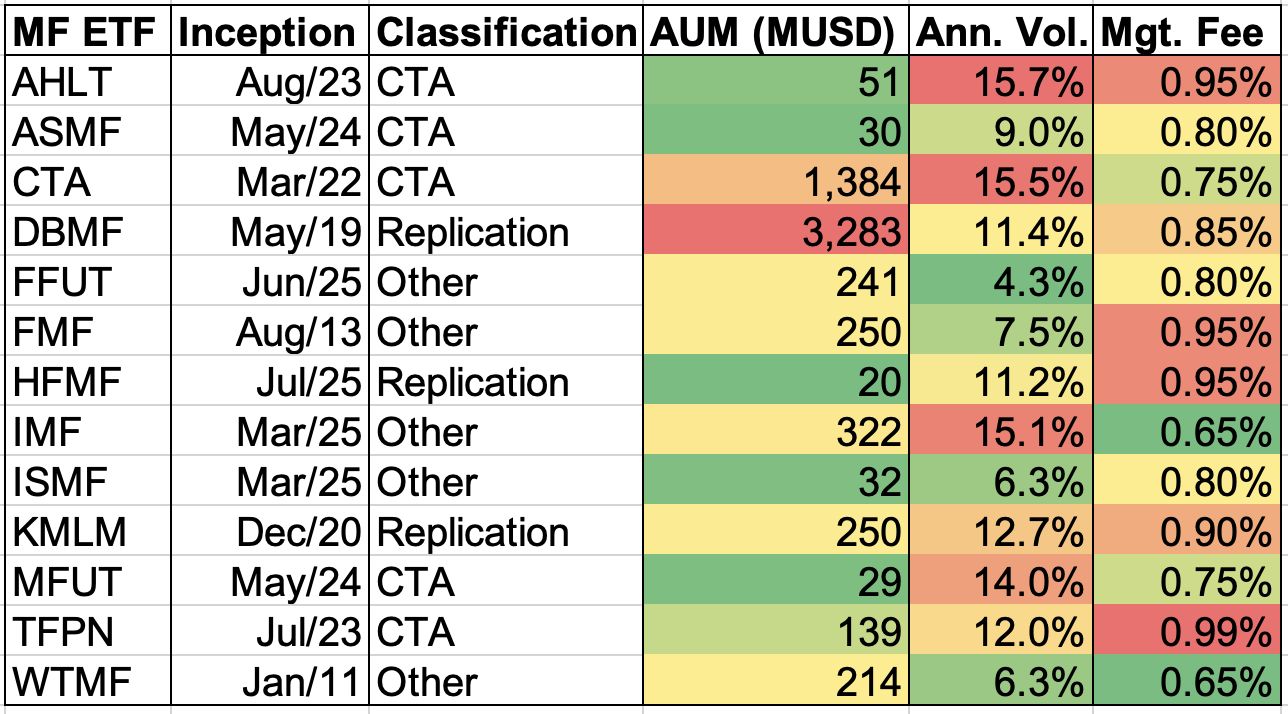

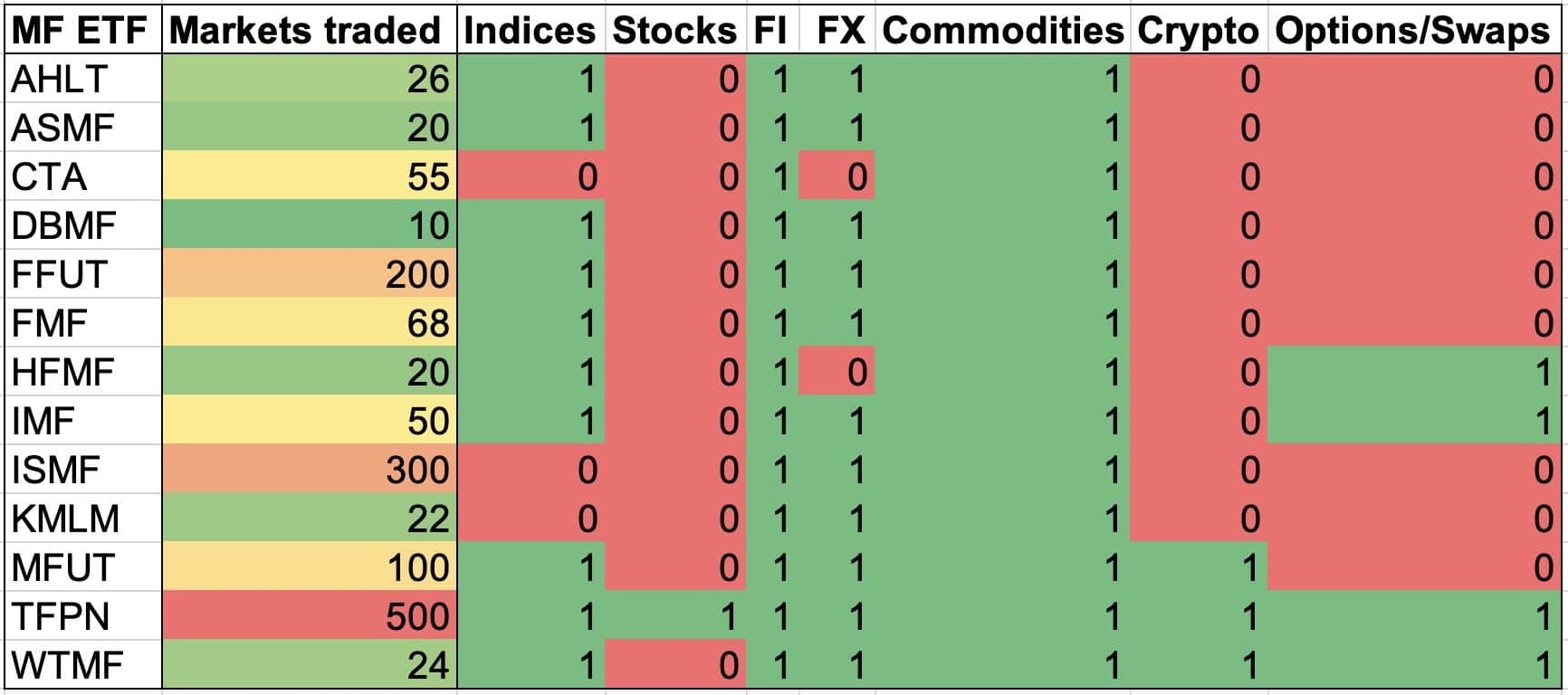

In Table 1 we have summarized basic information regarding available MF ETFs. In Table 2 we provide an overview over ETFs’ sector exposure. It’s a jungle out there! It’s actually more of a thicket, because while the number of available ETFs has increased exponentially, as of today, there are still only 13 distinct ETFs available and they are all very different from each other. Asset-wise, two ETFs totally dominate the market, i.e. a REPL strategy and CTA strategy, where an actual CTA manager is generating trading signals.

Most MF ETFs were launched less than three years ago. Thus, any statistical analysis will be limited and all results shown below will have to be taken with a pinch of salt. Variations of realized volatilities and applied management fees are striking. While CTA managers themselves are latecomers to the ETF-party, other financial institutions were the MF ETF pioneers, one of the OTHER was launched as early as January 2011. A lot of MF ETFs are still provided by other institutions, but asset-wise, these players have fallen behind. Regarding markets and sectors traded, very few MF ETFs are similar. Some trade rather non-traditional markets such as swaps, single stocks, and cryptocurrencies, whereas others have completely excluded any equity (and FX) exposure.

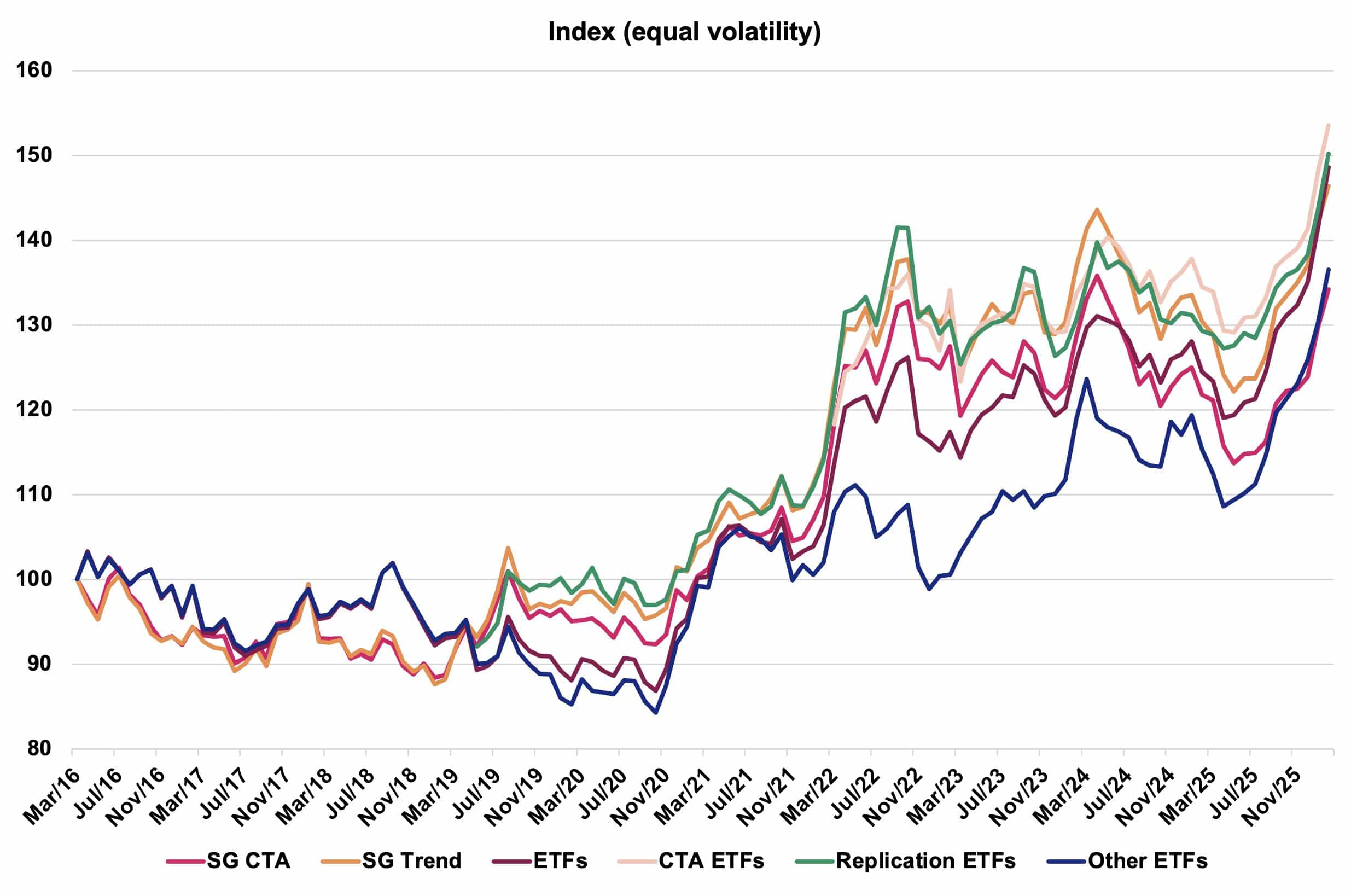

Now, let us address the elephant in the room: Regarding performance, can the apparently simpler MF ETFs hold a candle to their presumably more sophisticated counterparts? Figure 2 shows the most prominent industry benchmark, the SocGen CTA Index, compared to MF ETFs (divided into abovementioned groups). We have also added the SocGen Trend Index. (Most) MF ETFs claim that they deliver “trend beta” and use the SG CTA Index as their benchmark. However, out of the 20 SocGen CTA constituents, in 2025, five were applying non-trend following strategies such as global macro or short-term trading. Thus, a better benchmark for measuring trend beta would be the SocGen Trend Index which currently includes eleven “pure” trend following programs. On average and on a vol- and interest rate-adjusted basis, MF ETFs have outperformed the SocGen CTA but performed in line with SocGen Trend (despite the higher fees for the CTA programs in the index).

Replication and CTA-based MF ETFs both perform in line with the SocGen Trend Index and significantly outperform the SocGen CTA. Our research indicates that this outperformance is due to three factors, i.e., first, trend following has outperformed other MF substrategies in recent years; second, longer-term trading horizons have been the better choice in the difficult trading environment since President Donald Trump has taken office and, finally, market selection has played a role. Other MF ETFs underperform which makes us conclude that industry experience matters!

Overall, MF ETFs are doing a good job in delivering CTA-like performance. Due to the current market environment and the current prevailing trends, MF ETFs have slightly outperformed the broader CTA industry but performed in line with trend following substrategies. If the market environment changes or if trends occur outside MF ETFs’ investment scope, the broader CTA benchmark is expected to outperform again.

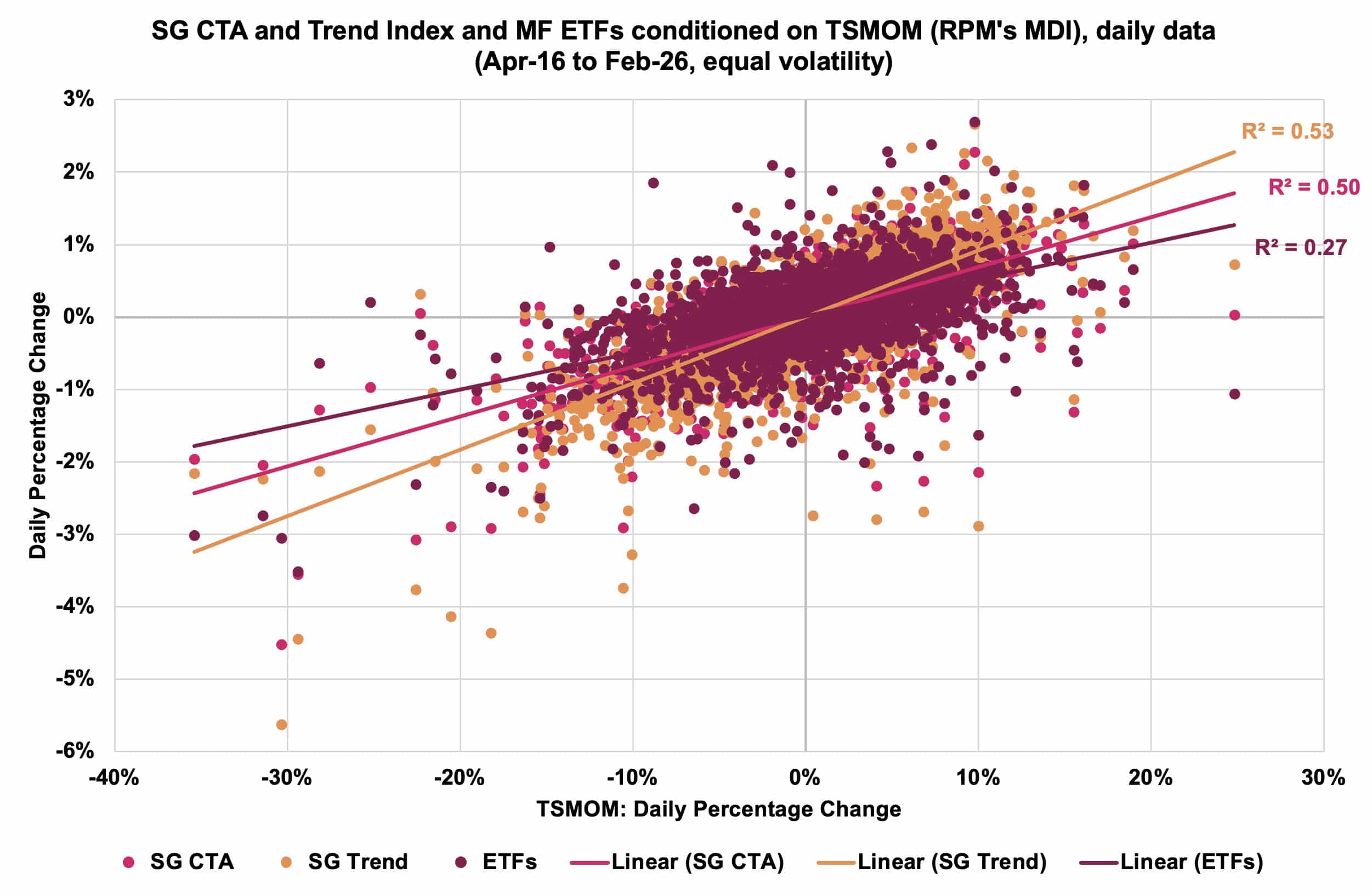

Next, we look at correlations of returns. How close do MF ETFs mirror CTA benchmarks? General correlation analyses show that MF ETFs exhibit significant positive correlations with CTA benchmarks. Furthermore, correlations are roughly the same vs. the SocGen CTA and the SocGen Trend index. Check! However, REPL ETFs are slightly higher correlated with benchmarks whereas OTHER ETFs show significantly weaker connections with the CTA space. As self-proclaimed, MF ETFs are supposed to deliver trend beta. Trend following strategies exploit so-called Time Series Momentum (TSMOM) generating profits in trending market environments, i.e., when asset prices move substantially and sustainably in different markets at the same time.

Figure 3 shows scatterplots for daily percentage changes of the Market Divergence Index (MDI), RPM’s measure of TSMOM, compared to daily percentage changes of the SocGen CTA, the SocGen Trend, and the MF ETF index between Apr-16 and Feb-26. Whereas both SocGen indices capture TSMOM fairly well with an R2 of 50% or above, MF ETFs capture roughly only a quarter of the MDIs’ daily moves. So, despite their slightly better performance, MF ETFs are not as good at capturing trends, again probably due to their slower systems and/or selective market exposure.

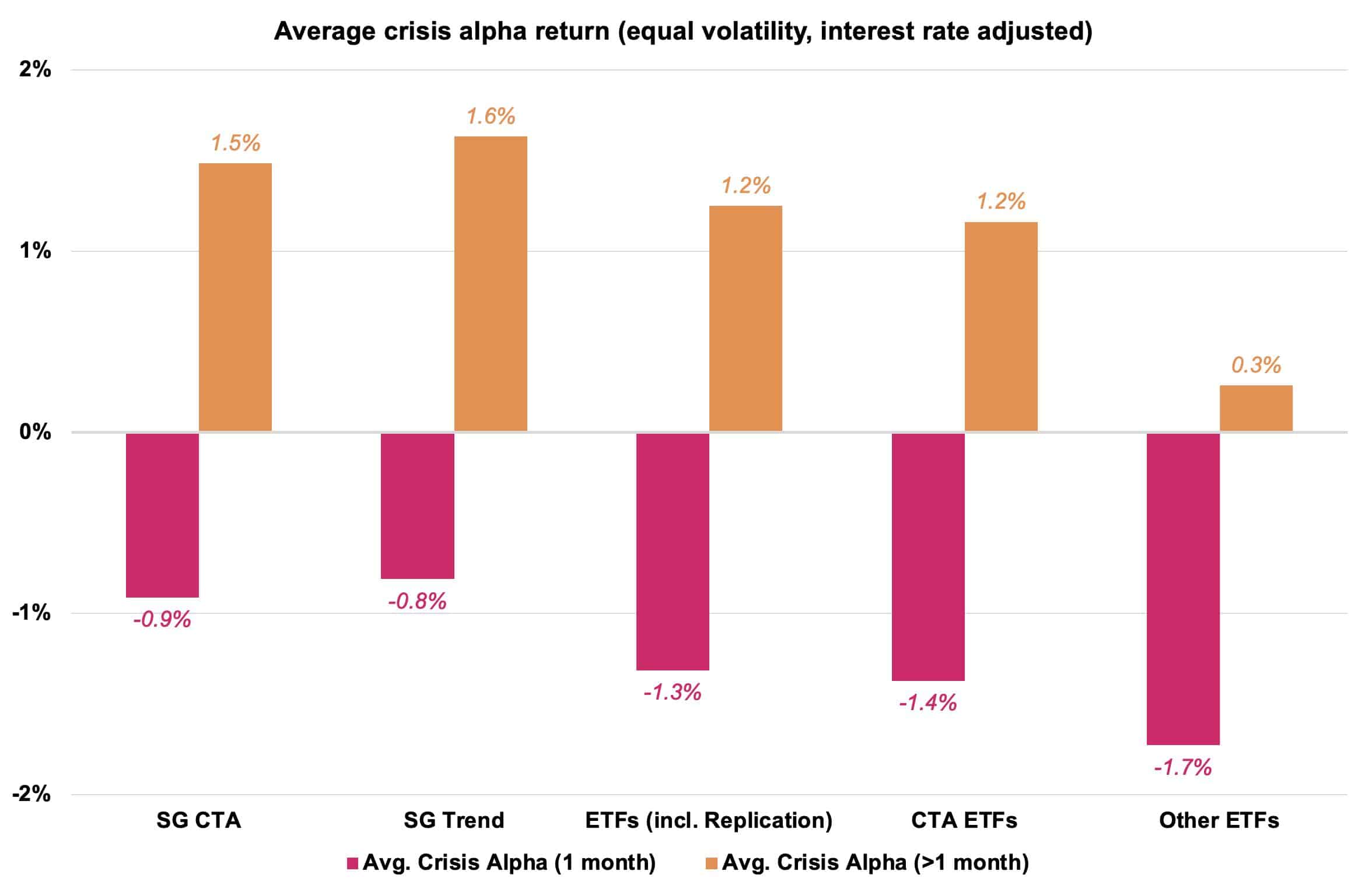

Finally, the holy grail of MF investing is getting protection during major market downturns as in 2022, the so-called “crisis alpha effect”. Thus, the question is whether MF ETFs are able to provide a similar crisis alpha like original CTAs. Figure 4 shows average crisis alpha for SocGen benchmarks and MF ETFs. As most MF strategies rely on sustained market moves (abrupt dislocations often reverse too quickly for programs to adjust), we need to separate crises into those lasting less than one month (corrections) versus longer-lasting events (crises) in order for clear differences in performance to emerge. We see that all MF strategies – MF ETF or CTA – serve as an effective hedge over medium- to long-term crises, but investors should not expect consistent positive returns during short-lived corrections. However, with regards to both corrections and crisis, MF ETFs underperform CTAs. OTHER ETFs, set up by institutions from outside the industry, significantly underperform, hardly providing any protection at all. The SocGen Trend Index is the best crisis alpha provider as should be expected.

Summing up, Managed Futures have finally made their full debut into the ETF world. Since last year, investors can choose between more than ten (very) different MF ETFs. Today, even retail and smaller institutional investors can easily, and inexpensively, access Managed Futures’ trend beta and crisis alpha protection. Now, the superior diversification benefits of CTAs can be part of basically every investment portfolio out there as they rightfully should and as we have been preaching for the last 20+ years. The good news is that, on average, all MF ETFs provide some degree of trend beta serving as an effective hedge over medium- to long-term crises. The bad news is that, as always in finance, there are no free lunches! Overall, MF ETFs capture less trend beta (TSMOM), and also provide less crisis alpha, than their more sophisticated peers. So, if you are a professional investor who has the capability to invest directly in original CTA managers, our advice is to take the time and make the effort to do so. Or hire help…

Beware the hype! MF ETFs seem to have outperformed the CTA industry, but this is mainly due to MF ETF providers using a less applicable benchmark. Instead of the SG CTA, the SG Trend Index should be used. Nevertheless, on average, MS ETFs have performed in line with this index and have achieved this at a lower cost. Kudos. That being said, we believe that if and when the market environment changes, original CTA managers will gain the upper hand again (as they did in 2022). Furthermore, investors need to take a close look under the hood. Not all MF ETFs deliver trend beta as promised. MF ETFs introduced by CTA “outsiders” underperform, capture less TSMOM, and provide significantly less crisis protection.