The U.S. high yield market has long been regarded as the global benchmark: deeper, more liquid, and broader in sector composition. For many allocators, U.S. high yield has traditionally been the default source of carry. However, the relative case is becoming more nuanced. In an environment where currency dynamics, political risk and downside mitigation matter as much as headline spreads, European high yield is increasingly viewed not merely as a complement to U.S. exposure, but as a strategic allocation in its own right.

“The European high yield bond market is big enough to allow, in particular European investors, to diversify away from the U.S. and the U.S. dollar,” says Charles Watford, lead portfolio manager of PIMCO’s European High Yield strategy. On a currency-hedged basis, Watford sees little difference in absolute yield between the two markets. “If you look at euro-hedged yields, they’re broadly identical. U.S. high yield hedged back into euros is around 4.5 to 4.8 percent[1], depending on the day. European high yield is in a very similar range,” he explains.

“If you look at euro-hedged yields, they’re broadly identical. U.S. high yield hedged back into euros is around 4.5 to 4.8 percent, depending on the day. European high yield is in a very similar range.”

While some allocators remain hesitant to scale back U.S. equity exposure, the calculus in fixed income is fundamentally different. “When you come to fixed income, it’s more about downside mitigation,” Watford emphasizes. “It’s about capturing that carry and seeking to avoid the downside.” In that context, he argues, the relative case for Europe strengthens. “This is a higher-quality market offering the same potential yield on a hedged basis with sufficient diversification,” he says. “If you’re a European investor, why would you necessarily want the additional U.S. political and currency exposure, when you can achieve similar returns domestically?”

Quality Advantage and Market Depth

The European high yield market has grown to roughly €400 billion in outstanding issuance, spanning around 400 issuers[2]. That represents approximately one quarter of the global high-yield market by size. According to Watford, this scale is sufficient to construct diversified portfolios across sectors, ratings buckets and maturities. “It’s large enough to build a genuinely diversified portfolio across different sectors and companies. You’re not constrained in terms of breadth,” he says.

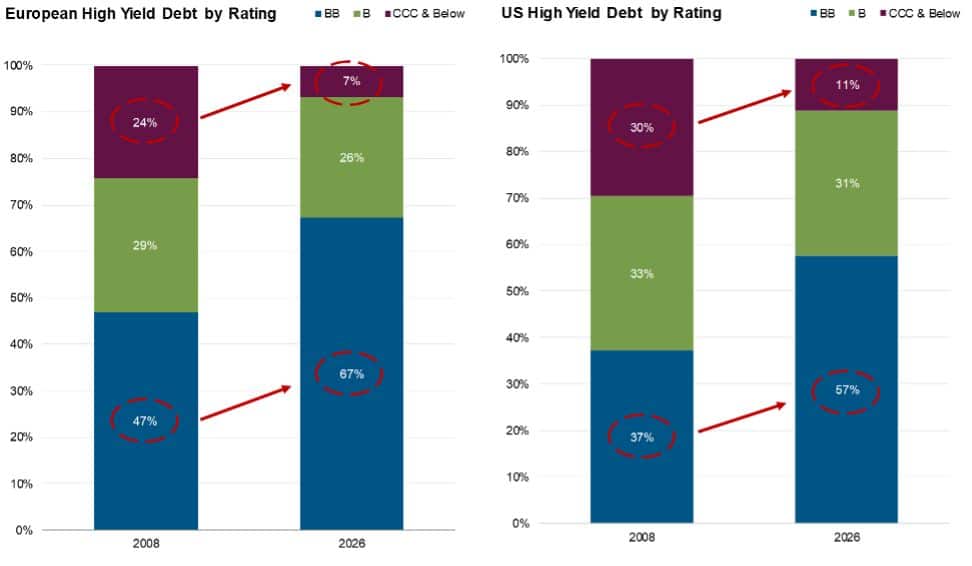

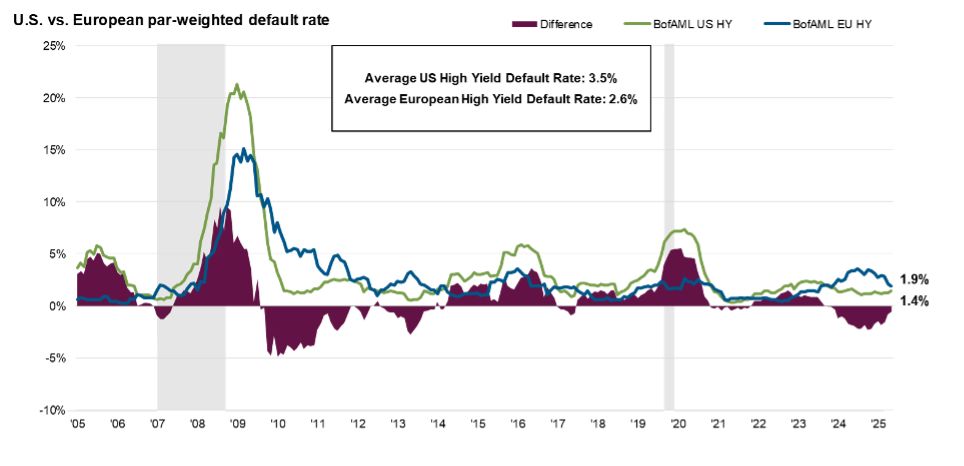

More importantly, the European market screens better on average credit quality. “Only about 7 percent of the European high-yield index is triple-C rated, compared to roughly 11 percent in the U.S.,” Watford notes. “Historically, European high yield has had average default rates about one percentage point lower than the U.S. market.”[3] That structural difference matters, particularly in late-cycle conditions. “Over time, lower default rates should translate into outperformance, all else equal. And in a recessionary scenario, you would expect European high yield to hold up relatively better,” he argues.

Fundamentals Supportive, Spreads Tight

Watford breaks down the investment case across three dimensions: fundamentals, yields and spreads. On fundamentals, he sees resilience. “Leverage in European high yield is at the lowest levels we’ve seen in five to ten years,” he says. “The higher-rate environment has forced companies to be more disciplined in terms of borrowing.” He does not observe signs of excessive risk-taking or late-cycle overconfidence. Typically, such behavior would manifest in surging issuance volumes, elevated M&A activity, or aggressive capital expenditure plans. The more subdued level of public market issuance, he adds, may in part reflect the rapid growth of the private credit and broadly syndicated loan markets, which have absorbed a meaningful share of financing activity.

Yields remain attractive in absolute terms, largely because of the higher starting point in risk-free rates. Duration in the European high-yield index remains relatively short, typically between 2.5 and 3 years, limiting sensitivity to interest rate movements. Spreads, however, are undeniably tight. “Across credit markets, investment grade and high yield, both in the U.S. and Europe, spreads are in the tightest quartile of the last decade,” Watford observes.

“In a downturn, you could see 150 to 200 basis points of spread widening. But with two and a half to three years of duration, that kind of widening would likely leave you with roughly flat total returns over a 12-month horizon rather than with deep losses.”

Still, he believes fundamentals provide some justification for current levels. “There is support for these spreads from fundamentals.” The main risk remains a recessionary shock. “In a downturn, you could see 150 to 200 basis points of spread widening,” he says. “But with two and a half to three years of duration, that kind of widening would likely leave you with roughly flat total returns over a 12-month horizon rather than with deep losses.” In that sense, carry may provide a meaningful cushion.

Dispersion and the Case for Active Management

While average spreads are tight, dispersion within the market has increased, creating opportunities for active managers. “There’s a meaningful portion of the market trading at 150 to 200 basis points, but there’s also a sizable segment trading at 400 to 1,000 basis points,” Watford explains. “In euros, that’s roughly 7 to 12 percent yields.”

Default avoidance, he emphasizes, is central to generating excess returns in high yield. “If you’re getting 5 percent carry on average, you need a lot of winners to offset one default. Default avoidance is one of the largest sources of excess return potential.” He frames it quantitatively: “If defaults run at 2 to 3 percent and we can avoid half of them, that alone could translate into 50 to 100 basis points of outperformance versus the index.”

“If defaults run at 2 to 3 percent and we can avoid half of them, that alone could translate into 50 to 100 basis points of outperformance versus the index.”

Active managers can also add value through new issue premiums, covenant analysis and capital structure positioning. “There’s usually a new issue premium,” Watford notes, adding that rigorous analysis of covenants and security packages can also position managers in more attractive parts of the capital structure. In addition, index-related inefficiencies create opportunities around rating migrations. “When bonds move from investment grade into high yield or vice versa, there’s often the ability to capture better risk-adjusted returns,” he explains, referring to forced buying and selling dynamics among benchmark-constrained investors.

“When bonds move from investment grade into high yield or vice versa, there’s often the ability to capture better risk-adjusted returns.”

Beyond the benchmark universe, Europe also offers select off-index opportunities. Some issuers remain unrated and therefore excluded from major indices, yet may present compelling fundamentals and attractive compensation for risk. For active managers with the resources to conduct bottom-up credit work, these segments can represent a differentiated source of outperformance.

Portfolio Construction and the Role in Asset Allocation

Backed by a global team of more than 80 credit analysts, almost 20 of whom are based in Europe, the PIMCO European High Yield strategy is structured around three alpha levers: structural, thematic and opportunistic. “The structural bucket focuses on areas with historically better Sharpe ratios, such as the front end of the curve, rising stars and fallen angels,”[4] Watford explains. Thematic positioning reflects broader macro and sector developments. “In an environment of rate cuts and improving credit quality, sectors like real estate and financials can benefit. Artificial intelligence is another theme, supportive for utilities, potentially more challenging for certain software names.”

Lastly, the opportunistic allocation seeks to exploit market dispersion. “We look at segments trading at 6 to 12 percent yields and ask whether we are being compensated for the risk,” says Watford. The emphasis is not on stretching for yield, but on identifying situations where spreads imply a more negative outcome than fundamentals suggest. As bond investors with a strong focus on default avoidance, diversification and risk control remain central to portfolio construction. The strategy typically holds between 150 and 250 names, with position sizing driven by conviction, liquidity and downside risk. “Higher-quality, more liquid positions might be 75 to 100 basis points overweight compared to the benchmark, while more event-driven names might be closer to 25 basis points,” he says.

“Historically, high yield has offered comparable returns to equities with roughly two-thirds of the volatility. For an allocator, having part of your European equity exposure expressed through European high yield can make sense.”

From a broader asset allocation perspective, Watford argues that European high yield offers three clear potential benefits: attractive carry with limited duration risk, reduced exposure to U.S. political and currency dynamics, and historically equity-like returns with lower volatility[5]. “Historically, high yield has offered comparable returns to equities with roughly two-thirds of the volatility,” he notes. “For an allocator, having part of your European equity exposure expressed through European high yield can make sense.”

The PIMCO European High Yield strategy has pursued strong performance across different market environments both on an absolute and risk-adjusted basis. According to Watford, this has been driven primarily by disciplined credit selection and a strong emphasis on downside mitigation. “It’s been achieved by credit selection, including avoidance of some of the weaker names and a significant focus on risk management.”

[1] Yield-to-maturity level of the Merrill Lynch US High Yield, BB-B Rated (EUR-H) Index

[2] Source: PIMCO internal calculations

[3] Source: PIMCO internal calculations

[4] ‘Rising stars’ refer to issuers that have increased in credit rating and gone from being classified as high yield to investment grade. Fallen angels refer to issuers that have gone from investment grade to high yield.

[5] Source: PIMCO internal calculations

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

Capital at risk.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Swaps are a type of derivative; swaps are increasingly subject to central clearing and exchange-trading. Swaps that are not centrally cleared and exchange-traded may be less liquid than exchange-traded instruments. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Certain U.S. government securities are backed by the full faith of the government. Obligations of U.S. government agencies and authorities are supported by varying degrees but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value.

Disclaimer

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. This is not an offer to any person in any jurisdiction where unlawful or unauthorized.| PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. Since PIMCO Europe Ltd services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. | PIMCO Europe GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany) is authorized and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 15 of the German Securities Institutions Act (WpIG). PIMCO Europe GmbH Italian Branch (Company No. 10005170963, Via Turati nn. 25/27 (angolo via Cavalieri n. 4) 20121 Milano, Italy), PIMCO Europe GmbH Irish Branch (Company No. 909462, 57B Harcourt Street Dublin D02 F721, Ireland), PIMCO Europe GmbH UK Branch (Company No. FC037712, 11 Baker Street, London W1U 3AH, UK), PIMCO Europe GmbH Spanish Branch (N.I.F. W2765338E, Paseo de la Castellana 43, Oficina 05-111, 28046 Madrid, Spain), PIMCO Europe GmbH French Branch (Company No. 918745621 R.C.S. Paris, 50–52 Boulevard Haussmann, 75009 Paris, France) and PIMCO Europe GmbH (DIFC Branch) (Company No. 9613, Index Tower Floor 10, unit 1001 Dubai International Financial Centre, Dubai, United Arab Emirates) are additionally supervised by: (1) Italian Branch: the Commissione Nazionale per le Società e la Borsa (CONSOB) (Giovanni Battista Martini, 3 – 00198 Rome) in accordance with Article 27 of the Italian Consolidated Financial Act; (2) Irish Branch: the Central Bank of Ireland (New Wapping Street, North Wall Quay, Dublin 1 D01 F7X3) in accordance with Regulation 43 of the European Union (Markets in Financial Instruments) Regulations 2017, as amended; (3) UK Branch: the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN); (4) Spanish Branch: the Comisión Nacional del Mercado de Valores (CNMV) (Edison, 4, 28006 Madrid) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Title V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively, (5) French Branch: ACPR/Banque de France (4 Place de Budapest, CS 92459, 75436 Paris Cedex 09) in accordance with Art. 35 of Directive 2014/65/EU on markets in financial instruments and under the surveillance of ACPR and AMF and (6) DIFC Branch: Regulated by the Dubai Financial Services Authority (“DFSA”) (Level 13, West Wing, The Gate, DIFC) in accordance with Art. 48 of the Regulatory Law 2004. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication. According to Art. 56 of Regulation (EU) 565/2017, an investment company is entitled to assume that professional clients possess the necessary knowledge and experience to understand the risks associated with the relevant investment services or transactions. Since PIMCO Europe GMBH services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2026, PIMCO.

For professional investor use only

CMR2026-0225-5242572