By Anant Bhatnagar, Yalin Zhang, Yihai Yu, Yao Zhang – MSCI: The global interest-rate rise since 2022 has suppressed mortgage-prepayment speeds across markets globally. Consequently, mortgage bonds’ durations have extended drastically — what is commonly known as lock-in effect. The unique delivery option in Danish mortgages benefits borrowers and may add even more lock-in effect for investors, compared to U.S. mortgages. This creates unique duration-extension risk for Danish bonds, requiring extra attention for modeling and managing rate risk.

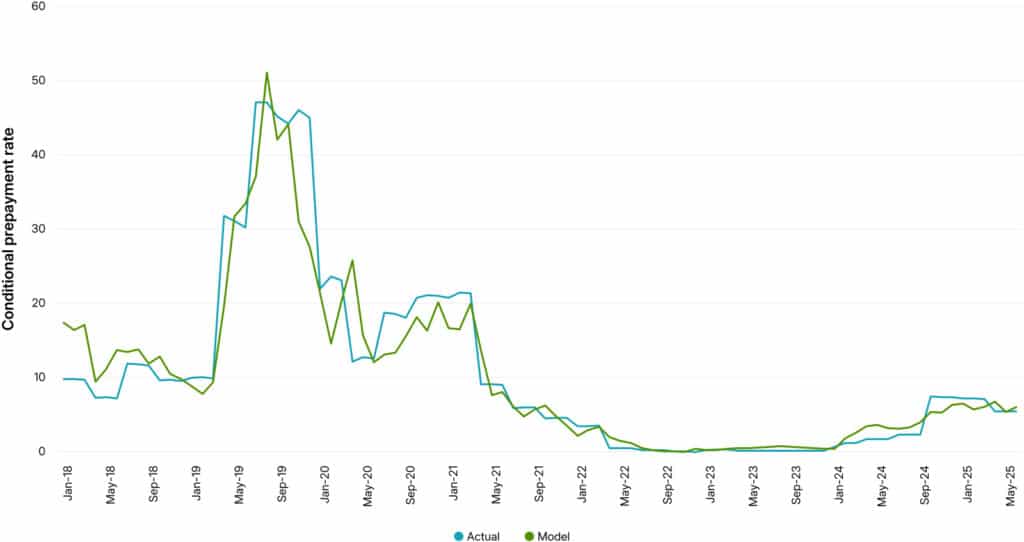

Danish mortgage bonds’ prepayment dropped to near 0 amid rising rates, but is higher again

One unique feature of the Danish mortgage market is the delivery option, which allows borrowers to buy back the bond from the market to cancel their mortgage. Under the scenario of a rates sell-off, homeowners may still want to sell their home for various reasons. This delivery option can conveniently enable borrowers to buy back their loans at the market price, instead of the traditional prepayment option at par. (A rates sell-off means these bonds will be traded at a discount.) Then, this financial benefit can be used to offset the higher borrowing cost for the mortgage of the new home.

In the U.S. housing market, many borrowers face a significant lock-in effect, which discourages them from selling their current homes and purchasing new ones, as doing so would require taking on a new mortgage at a much higher prevailing interest rate. This lock-in effect restricts housing mobility and slows broader economic activity. As U.S. policymakers and market participants work on solutions like making mortgages portable, Danish borrowers have long benefited from the flexibility of the delivery option, experiencing minimal lock-in effects.

Importantly, the delivery option doesn’t directly reduce investor returns, unlike traditional prepayments. Instead, it introduces bond-repurchase demand, which helps support the pricing of lower-coupon bonds.

As some Danish borrowers exercise the delivery option and move, those who remain in the bond pool tend to be longer-tenured homeowners. This self-selection dynamic resembles the refinance-burnout effect, where remaining borrowers are less likely to prepay. As a result, the effective duration of the bond can significantly extend.

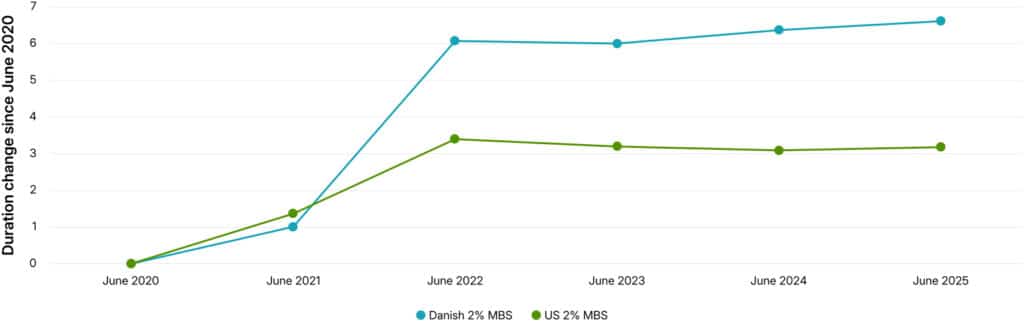

Danish mortgage bonds’ duration extended more than that of US mortgage-backed securities, due to delivery option

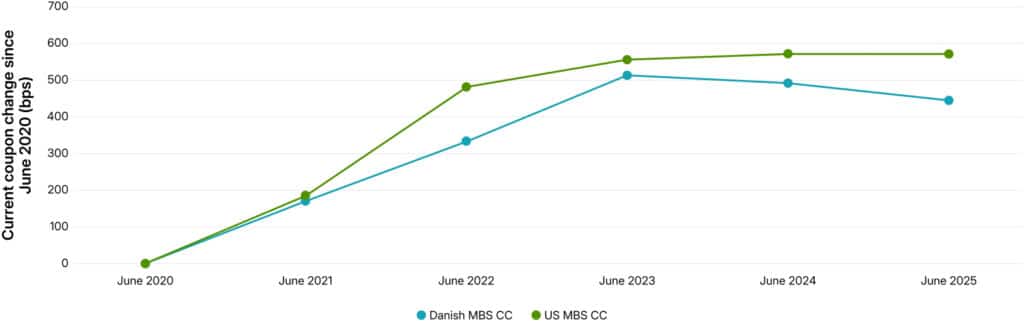

Historically, Danish mortgage bonds have exhibited greater duration extension compared to U.S. agency mortgage-backed securities (MBS). This observation aligns with actual prepayment behavior across the two markets. As illustrated in the chart below, U.S. mortgages continue to prepay at an average rate of approximately 4% conditional prepayment rate (CPR), even for deeply out-of-the-money coupons, whereas discount Danish mortgage bonds currently prepay at rates close to 0% CPR.

This stark contrast is further amplified by the more efficient refinancing mechanisms in the Danish system. Together, these factors contribute to a significantly more pronounced duration extension in Danish mortgage bonds, particularly during periods of rising interest rates.

Fannie Mae 30-year shows a prepayment floor even for deeply out-of-the-money coupons

While nominal prepayment speeds for discount Danish mortgages are currently near 0, the delivery option continues to play a key role in sustaining the issuance of new Danish mortgage bonds at prevailing market rates. In addition, many borrowers have taken advantage of low bond prices by repurchasing their mortgages on the open market at deep discounts — effectively using this opportunity to build equity. For instance, a typical discount mortgage with a 2% coupon is now trading around DKK 85, meaning that exercising the delivery option immediately reduces the borrower’s outstanding balance by approximately 15%.

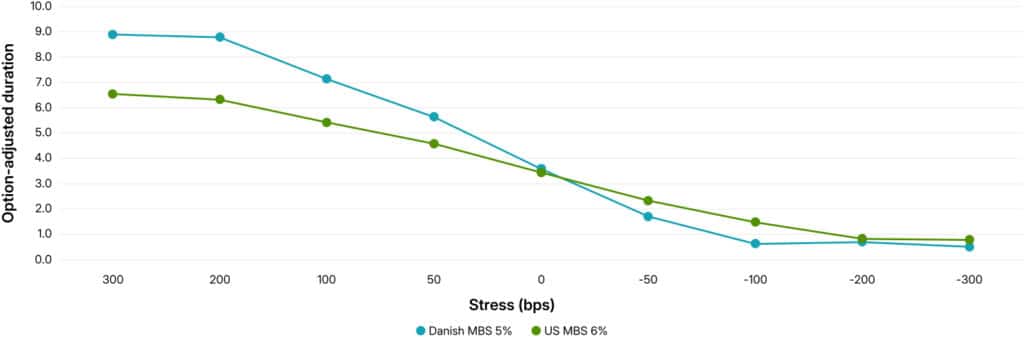

These current-coupon Danish mortgage bonds are exposed to both extension and contraction risks. Using the MSCI suite of models for analyzing U.S. agency MBS and Danish mortgage bonds, we compare their duration profiles. In line with historical prepayment trends, Danish bonds demonstrate the potential to extend significantly more than their U.S. counterparts during rising-rate environments, while also contracting more rapidly when rates decline. Portfolio managers therefore need to take a more active role in monitoring hedging effectiveness.

Danish mortgage bonds show steeper duration profile than US mortgages

In summary, the Danish mortgage-finance system — characterized by its unique structure and high refinancing efficiency — has enabled homeowners to largely avoid the lock-in effect that constrains borrowers in other markets. These same features also present challenges for investors, however, particularly in managing portfolio duration risk and implementing effective hedging strategies.

Danish Mortgage Market: Flexibility for Borrowers, Complexity for Investors | MSCI