By Abdallah Guezour, Head of Emerging Market Debt and Commodities at Schroders: Emerging market debt (EMD) continues to perform well despite the “aggressive Trump” scenario starting to materialise, notably with regards to global trade. The announcement and subsequent implementation of tariffs against China and Mexico had a limited impact on these markets so far. It is particularly worth noting that Mexican local government bonds generated a return of +7.6% in US dollar terms year-to-date, thus outperforming handsomely the strong gains of the GBI EM GD Index (Government Bond Index-Emerging Markets Global Diversified).

This remarkable resilience of Mexican fixed income and currency in the face of the resurgence in the trade war with the US corroborates the view highlighted in the previous editions of this report: technicals (light investors’ positioning) and valuations have become so supportive that it will probably require a significant and unexpected shock for several EM bonds to reverse their recent recovery trends.

We have recently turned more cautious regarding the global growth outlook, including for the US economy. Global growth expectations are already starting to be revised lower (see below). The impact on investment sentiment of the ongoing trade war, more restrictive immigration policies and a significantly less supportive fiscal boost compared to the Biden years represent major headwinds for the US growth trajectory.

This is the reason why we have seen a tactical opportunity since the beginning of the year in US interest rate duration. As covered in our previous monthly report, market technicals were (and remain) very supportive for US rates given that market participants have been short thus making long-dated US Treasuries susceptible to a continued short squeeze. However, there may now be an opportunity to take some profit on US duration given the possibility that the recent surge in European rates could start to contaminate the US.

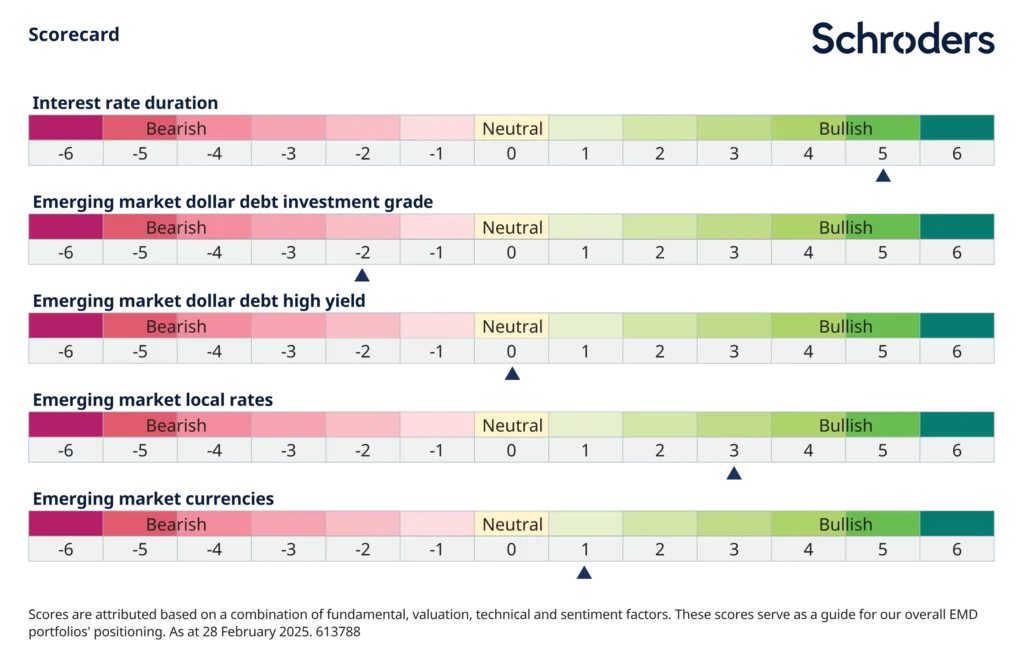

Our investment strategy turned more constructive at the turn of the year on US interest rate duration and on EM local rates and we are also now seeing some encouraging signs in currency markets. In contrast, we continue to see less potential for spread tightening in EM dollar debt, especially given the high correlation between EM growth (with downward revisions to expectations starting to occur) and spreads (still at historically tight levels). The updated sectorial scorecard in figure 1 provides a summary of our current strategy.

Figure 1:

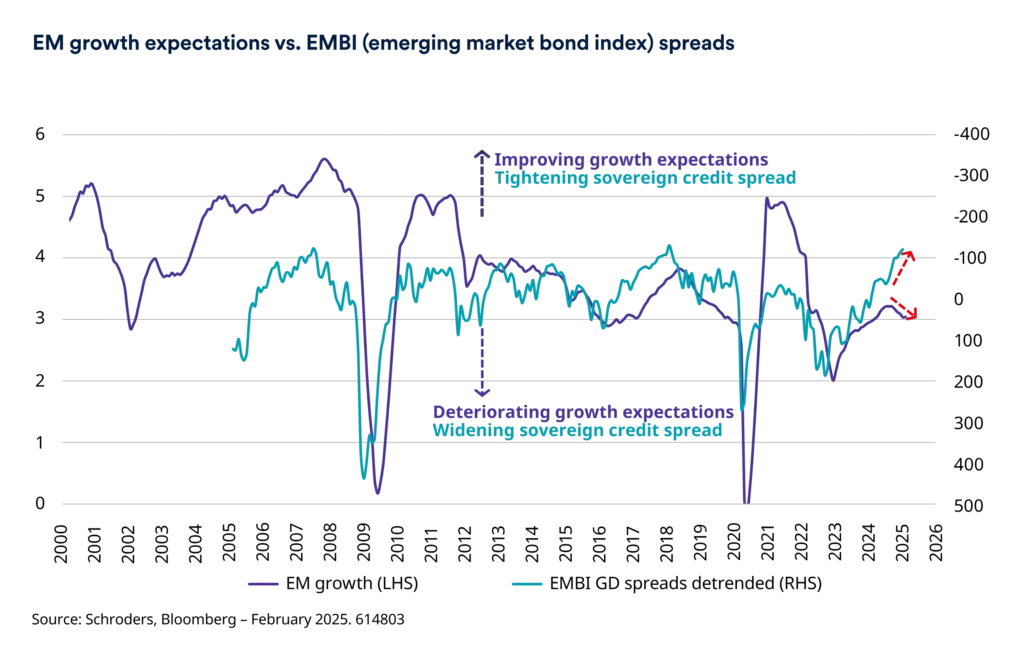

The recent global trade and geo-political uncertainties are likely to lead to a more noticeable deterioration in global growth outlook. Figure 2 shows the recent erosion in EM growth expectations and the lack of a meaningful impact so far on sovereign spreads.

Given the room for manoeuvre for several EM central banks to cut rates, ample global liquidity and the lack of any serious balance of payments vulnerabilities in EM, we do not expect a severe growth slowdown but rather a recalibration lower in expectations. This recalibration has yet to be reflected in sovereign spreads, which we need to see correcting somewhat before we can turn unequivocally bullish again on EM dollar debt.

For now, our constructive outlook on US rates and the pockets of value that we continue to identify in EM high yield still provide us with reasonably attractive expected total returns in this sector.

An example of these opportunities is Egypt, where we conducted a research trip in February and returned with a confirmation of our positive view both on sovereign external and local debt. Below we provide a brief update on Egypt following our meetings with policymakers in Cairo.

Figure 2:

The political situation in Egypt is expected to remain stable and the ongoing attempts to achieve peace in Gaza are likely to improve sentiment. President Sisi will push back on President Trump’s suggestions to relocate Palestinians from Gaza and has arranged an Arab summit to consolidate the regional stance on the peace process and on Gaza reconstruction. The Gulf states are likely to provide financial support to Egypt should a gap emerge from the removal of US aid programmes.

Egyptian authorities have made good progress on macro-economic stabilisation but more needs to be done. Attention will now turn to the second stage of the reform programme: levelling the playing field by reducing the state’s footprint in the economy and attracting private sector involvement. This will be vital for the next IMF reviews.

In this regard, the recent cabinet reshuffle has brought in a new economic team which has injected impetus into the reform process. This new reform drive will continue to support the recent trend of sovereign spread tightening from current levels of 600bps. Local debt appears even more appealing with three-year bonds at around 22.7% and 12-month inflation expectations of 11.5% implying an attractive ex-ante real yield in excess of 11% – a very high level by historical standards (ex ante real yield is the interest rate calculated before the actual rate of inflation is known.

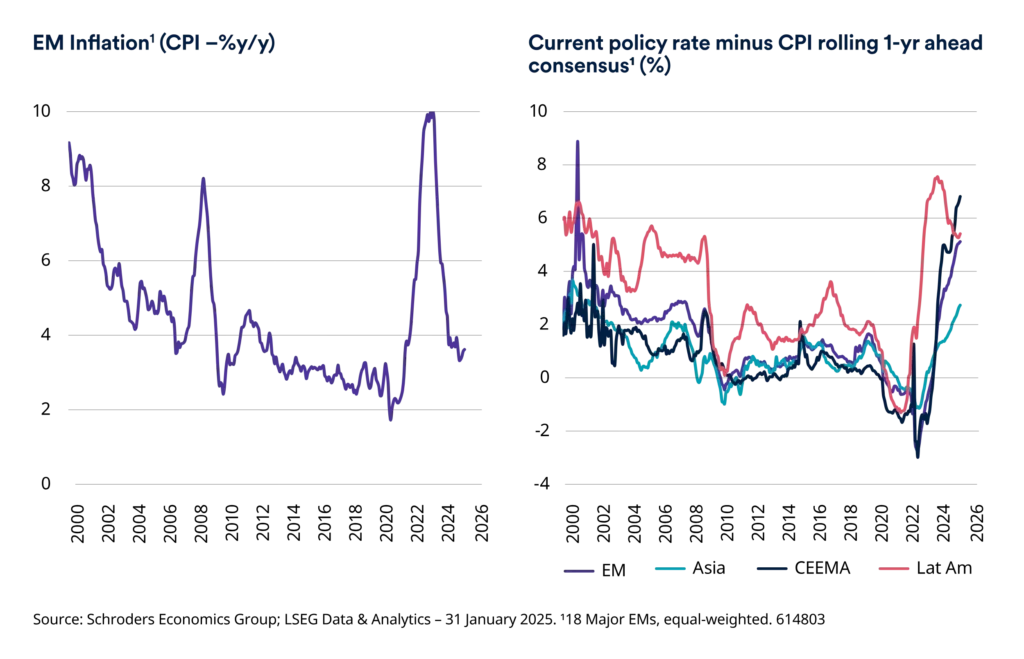

More broadly, we currently consider EM local rates as the most attractive sub-sector in EM. With continued erosion in growth expectations and concerns about external demand exacerbated by the ongoing trade war, several EM central banks have room to ease. Figure 3 shows that despite a possible rebound in inflation expectations and the stagflation nature of current global economic and geo-political trends, the level of ex-ante real rates is already at multi-year levels in all EM regions.

Figure 3:

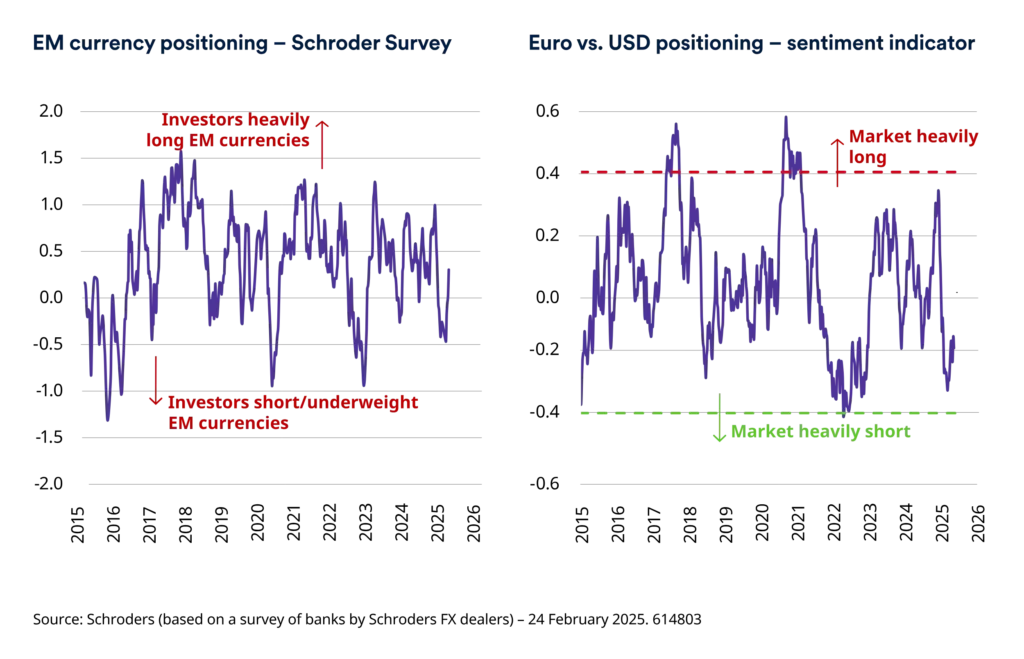

While the outlook for EM rates remains bullish, the picture for currencies is less clear cut in the current context of global dislocations. This justifies maintaining some currency hedges in place. However, the recent strong performance of several currencies versus the US dollar is encouraging. This resilience is supported by last year’s improvements in real effective exchange rates valuations and by a significant washout in investors’ positioning (figure 4).

Market participants in currency markets appear to have already adjusted their positioning lower ahead of the ongoing resurgence in the global trade war. Any positive news tends to trigger sharp rallies as we are seeing at this time of writing for the Euro and for Central European currencies. These have been reacting positively to the prospects of a peace deal in Ukraine and to the announcement of a substantial fiscal easing in Germany.

Figure 4: