By Jacob Grapengiesser and Peter Elam Håkansson at East Capital: 2024 was a solid year for emerging and frontier markets, both returning 12% in USD terms as of 10 December. We expect the positive momentum to continue into 2025, based on decent earnings growth and with much of the bad news largely priced in and reflected in positioning. JP Morgan estimated earlier this year that global funds had around 5.3% allocated to emerging market equities. A return to the 20-year average allocation of 8.4% would result in inflows of USD 910bn, or 58% of current emerging market assets under management. As such, we think emerging and frontier markets are worth a look given the rather demanding valuations and concentration in the US.

The specific path of returns will likely be determined by the key ‘known unknowns’, namely the exact nature of Trump’s tariffs and their impact on US inflation and global monetary policies, as well as whether the Chinese government can revive the country’s flagging economy. However, there will inevitably be many more ‘unknown unknowns’ that will emerge as the year progresses. As a result, we believe that 2025 (like most years) will be a year for dynamic stock pickers who are prepared to adapt quickly to changing conditions and take advantage of any mispricing that occurs.

2024 – a mixed bag

The returns in 2024 illustrate one of our key theses, which is that emerging markets are a very heterogeneous group of countries, all at different points in their cycles and with diverse market drivers. The standout market in 2024 has been Taiwan, which is driven by the AI theme as it produces all the advanced AI chips for Nvidia, which benefits the largest holding in our global emerging markets strategy, TSMC, but also its suppliers. It is likely a surprise to most that the China offshore market outperformed developed markets, returning 23.4%.

It is also important to note that the underperformance relative to the US has not been due to lower earnings growth. In fact, East Capital Global Emerging Markets Sustainable (“GEMS”) portfolio saw earnings growth of around 25% in 2024 and is expecting 18% next year, or a compounded earnings growth of 48% over two years. In comparison, S&P 500 earnings growth over the two year period is expected to be 26%.

On the negative side, clearly Latin America stands out. This was largely due to self-inflicted wounds by the countries’ politicians that hurt the currency and the equity markets. However, coming back to our alpha year argument, our two largest names in Brazil (WEG and Nubank) returned 57% and 41% respectfully, thanks to strong structural growth regardless of the macro backdrop – this is huge outperformance compared to the – 24% of Brazil.

Looking forward – a positive backdrop

Globally, macroeconomic conditions remain relatively benign, with solid economic growth (i.e. neither hard nor soft landing) and falling interest rates in most countries. This has historically been a good backdrop for equity markets.

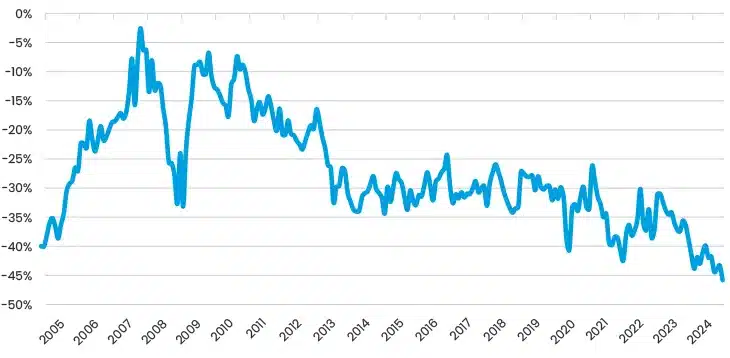

Under Trump 2.0, the US is the most obvious winner, thanks to expected tax cuts, deregulation and a likely strengthening dollar. However, this is priced in, with the US trading at near 10-year highs (Figure 3) and with a record weighting in global benchmarks, e.g. 65% of the MSCI All-World Index versus 50% 10 years ago. As such, it is not surprising to see views such as this recent FT article which refers to the current US market as “the mother of all bubbles”. The main argument is that while US stocks were more expensive during the dotcom bubble in 2000, the US market did not trade at nearly as large a premium to the rest of the world.

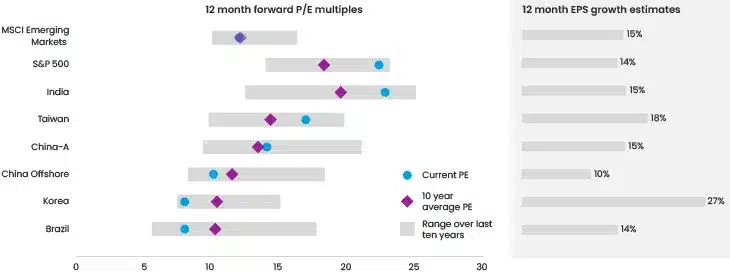

Emerging markets, on the other hand, are trading around average valuations on an aggregate basis and at a 45% discount to the S&P 500, which is a record high discount (Figure 4).

We do not expect emerging and frontier markets to significantly outperform the US, but given the record high valuations and global portfolio investors’ concentration in the US, we think it is worth looking outside Wall Street for a portion of portfolios. And the pickings outside the US are slim: Europe remains on life support, with the “sick man of Europe” Germany posting 0% (not a typo) GDP growth this year and well below 1% in 2025. On the other hand, overall emerging markets’ economic growth looks reasonable at 4.5%, with the second largest market, India, expected to grow 6.5% next year thanks to structural growth that is completely uncorrelated to the US.

The article goes on to explore the primary drivers behind key regions and markets where East Capital invests (read more here).