The finance industry is filled with terms that lack universally agreed definitions, and “alternative fixed income” is one such term. What does this term actually mean, and what falls under its scope? For Aegon Asset Management, which oversees an €80 billion alternative fixed-income platform that includes a lot, but also strategies tailored to Solvency II regulations, the definition is just one part of the conversation.

“Alternative fixed income represents a segment of the fixed-income market that investors cannot access directly – an area where managers like us to originate, secure, or guarantee loans that are packaged into various solutions,” explains Frank van den Berk, Head of Marketing Continental Europe at Aegon Asset Management. “Dogmatically, what exactly falls under this term?” asks Frank Drukker, Executive Director of Institutional Business Development at Aegon Asset Management. “Our perspective on the alternative fixed income universe is more comprehensive, encompassing both liquid and illiquid components, rated and unrated securities, spread-generating products, yield-generating products, IG and sub-investment grade instruments, and more,” Drukker elaborates. “There are so many different dimensions to alternative fixed income.”

“Alternative fixed income represents a segment of the fixed-income market that investors cannot access directly – an area where managers like us to originate, secure, or guarantee loans that are packaged into various solutions.”

Frank van den Berk, Head of Marketing Continental Europe at Aegon Asset Management.

As the asset management arm of originally Dutch insurer Aegon, Aegon Asset Management offers a wide range of alternative fixed-income strategies tailored to comply with the Solvency II regime, which is particularly relevant for insurance and reinsurance companies operating in Europe. “Being part of a global insurance group like Aegon, which operates under the Solvency II framework, means many of the strategies we manage are designed with this angle, with what we call a Solvency II tweak,” explains Peter Slob, who also focuses on Institutional Business Development in the Nordics at Aegon Asset Management. “Both external investors and our insurance group rely on the majority of our alternative fixed-income strategies, always ensuring an alignment of interests with our investors, this since “we” invest in every each of the strategies before bringing it to the market, ourselves.”

“Both external investors and our insurance group rely on the majority of our alternative fixed-income strategies, always ensuring an alignment of interests with our investors, this since “we” invest in every each of the strategies before bringing it to the market, ourselves.”

Peter Slob, Institutional Business Development in the Nordics at Aegon Asset Management.

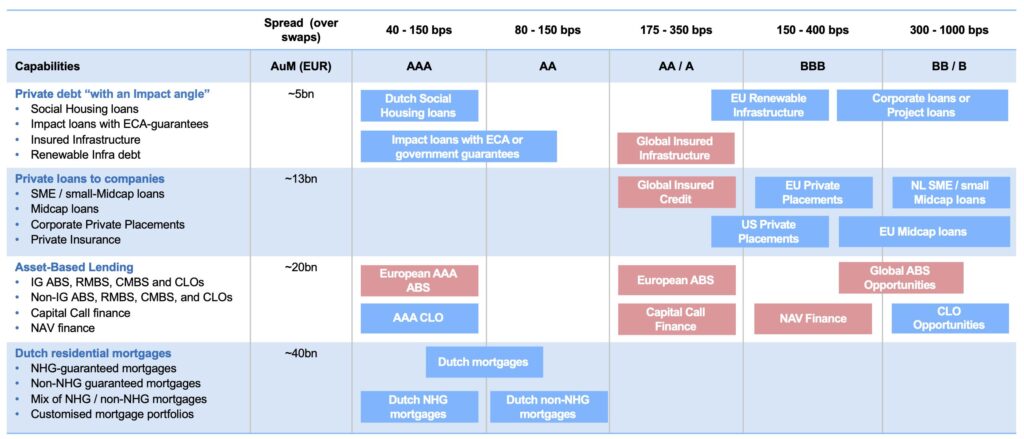

Different Flavors of Alternative Fixed Income

Aegon Asset Management’s alternative fixed-income platform manages over €80 billion across a wide range of strategies led by approximately 60 portfolio managers worldwide. The platform is structured into four broad categories: private debt, private loans, asset-based lending, and Dutch residential mortgages. Within these categories, the team offers a variety of sub-strategies, each with distinct objectives and risk-return profiles. Examples include Collateralized Loan Obligations (CLOs) or Capital Call financing within asset-based lending, Insured Credit under the “private loans” category, or Insured Infrastructure investments with an impact focus under “private debt.”

Drukker highlights that the “risk-return” perspective differs significantly for firms operating under Solvency II regulations compared to other players such as a family office. “A company subject to Solvency II or a bank evaluates the risk-return profile very differently than a family office, particularly after factoring in cost of capital calculations using the Solvency Capital Requirement (SCR),” he explains. Insurers prioritize fixed-income investments that offer the best risk-adjusted returns relative to their SCR impact. For example, an insured credit strategy offering a spread of 250 basis points may appeal less to a family office compared to a global ABS (Asset-Backed Securities) opportunities strategy, which could deliver an absolute return yield in the low teens. “The high capital charges under Solvency II make ABS strategies less attractive, as the potential returns are outweighed by the regulatory costs,” Drukker notes.

“A company subject to Solvency II or a bank evaluates the risk-return profile very differently than a family office, particularly after factoring in cost of capital calculations using the Solvency Capital Requirement (SCR).”

Frank Drukker, Executive Director of Institutional Business Development at Aegon Asset Management.

“ABS is heavily penalized for insurance companies under the Solvency II framework due to the high capital charges, which can reach up to 38 percent under the standard formula,” explains Drukker. “This makes it nearly impossible for insurers to generate a return on capital within their regulatory constraints,” he adds. In contrast, an insured credit product structured around providing a loan to a sub-investment grade issuer – such as a B or BB-rated loan – can be transformed into an AA or A-rated loan using a 100 percent unconditional insurance guarantee. This enhanced credit profile, combined with a spread of 250 basis points and full insurance coverage, makes such products far more attractive to insurance companies seeking capital-efficient investments.

Another compelling and timely segment within the alternative fixed-income space is fund finance, encompassing both Capital Call Financing and NAV Financing. These tailored financing solutions are designed for investment funds, such as private equity and private debt funds, among others, to help manage cash flows, optimize returns, and address liquidity needs. Drukker and Slob note a growing interest in these strategies: “We are observing increasing momentum in this area of the market, and as a result, we are having numerous discussions with large institutional investors. Part of the appeal lies in the potential spread pickup, which is driven by what we term a ‘novelty premium.’”

Frank van den Berk highlights that Aegon’s team is actively working to introduce innovative alternative fixed-income strategies into the Nordic region, drawing on solutions already established in the portfolios of Continental European investors. “By examining market trends and developments, we are bringing strategies to the Nordics that have proven successful elsewhere in Europe but have yet to gain traction here,” says van den Berk. “Nordic investors are eager to understand why their counterparts across Europe are incorporating these strategies into their portfolios.”

Leveraging Scale and Expertise

In the alternative fixed-income space, size plays a critical role in how managers source, structure, and manage investments. Whether dealing with private credit, asset-backed securities (ABS), infrastructure debt, or other non-traditional fixed-income assets, the scale of an organization can significantly impact its ability to access deals, negotiate favorable terms, and realize efficiencies. As Peter Slob explains, “Being consistently active in the market is key.” Taking ABS solutions as an example, Slob says that “all brokers and ABS houses know how to reach us and understand that we are always present and engaged.”

As an €80 billion alternative fixed-income platform, Aegon’s fixed-income team enjoys two key advantages over its peers in this space. “A crucial advantage is alignment of interest. All of the strategies we develop, we do so not only for third-party investors but also for ourselves, for our insurance group Aegon,” explains Frank Drukker. A prime example is the Dutch subordinated SME structure. The first vintage was exclusively funded by capital from Aegon’s own general accounts. Vintages 2 and 3, however, are open to third-party investors. “We test these strategies first, ensuring they work and making adjustments, if necessary, before introducing them to the market,” says Drukker. “This is a true alignment of interest. When the product performs well, it benefits both us and our clients. That’s the way we operate, and we feel very comfortable with this approach.”

“Ultimately, this platform is integrated into a much larger institution…there’s a much larger team working behind the scenes – on the research, structuring, and legal sides – along with other key partners who are essential in developing new, client-focused products.”

Frank Drukker, Executive Director of Institutional Business Development at Aegon Asset Management.

“The other key advantage is that we are a powerhouse in the alternative fixed-income space,” Drukker continues. “We possess deep expertise in the Solvency II treatment, and we know exactly how it works.” This strength extends beyond the fixed-income sector, as Aegon’s alternative fixed-income platform is just one part of the broader organization. “Ultimately, this platform is integrated into a much larger institution,” he emphasizes. “We have 21 people in our global ESG team, who are also available to support our fixed-income platform. Additionally, there’s a much larger team working behind the scenes – on the research, structuring, and legal sides – along with other key partners who are essential in developing new, client-focused products.”

Aegon Asset Management’s Nordic team has focused on the Nordics for a long time now and will continue to actively engage with partners to identify and deliver alternative fixed-income solutions that fit their portfolios.