By Amadeo Alentorn – Jupiter Asset Management: Having evolved from arboreal primates who relied on their senses and instincts to survive, most humans now occupy a highly sophisticated artificial environment that is at least as much data as nature. Data is everywhere: in phones, cars, homes, workplaces, and media. Data shapes our decisions, beliefs, behaviours, emotions, and identities. According to some estimates, several quintillion bytes of data are created daily1. A quintillion is 1 with 18 zeros after it. A DVD holds about 5 Gb, and a Gigabyte is a 1 with 9 zeros, so every day humans create of the order of 1,000,000,000 DVDs-worth of data.

Information overload is the difficulty the human mind has in understanding an issue when swamped by too much data. According to a 2023 paper published by the US Federal Reserve, information overload can increase both information risk and estimation risk2. Its authors argue that “information overload [may be]increasing information and estimation risk and deteriorating investors’ decision accuracy because of their limited attention.”

Behavioural Biases

How can we cope with so much data? Our brains are not computers, they work differently. We simplify. We tell stories. We fall in love with a narrative.

Trusting stories may be hard wired into our genes, because humans evolved the ability to create and comprehend stories as a survival strategy. Storytelling helped our ancestors to communicate vital information, to cooperate and coordinate with others, to enhance social bonding and group identity, and to simulate and plan future scenarios. Stories provided meaning and purpose, emotional regulation and coping skills.

Believing in stories may have conferred an adaptive advantage to early humans. While this worked well in the wild, it can disadvantage us when it comes to investing in the modern world. Stories often confirm group beliefs, are memorable, and convincing, but they can lead us into making mistakes. Our love of narrative can make us susceptible to behavioural biases, such as the following:

Firstly, it can make us prone to confirmation bias, the tendency to seek out and interpret information that confirms our existing beliefs, while ignoring or discounting evidence that contradicts them. Confirmation bias can lead us to overestimate the validity and reliability of our own opinions, and disregard alternative explanations or perspectives.

Second, it can make us susceptible to the availability heuristic, the tendency to judge the likelihood or frequency of an event based on how easily we can recall examples of it from memory. The availability heuristic can cause us to overestimate the probability of rare or dramatic events and underestimate the probability of common or mundane events.

Third, it can make us vulnerable to the framing effect, the tendency to be influenced by the way information is presented, rather than by the information itself. The framing effect can affect our decisions and preferences depending on how the options are worded, ordered, or emphasised. For example, we may be more willing to accept a gamble if it is framed as a potential gain rather than a potential loss, even if the expected value is the same.

These and other behavioural biases affect many investors, and, in our view, their effects can be detected in markets. For example, herding occurs when investors mimic the behaviour of others, which they may do especially when faced by highly uncertain outcomes. Herding behaviour may part of the reason for boom-and-bust cycles.

Are Markets Herding?

Are behavioural biases present in current markets? Global equity markets have generally been very strong over the past few months, as investors have become more optimistic about the US economy and about the technology sector in particular. The promise of Artificial Intelligence (AI) has grabbed the headlines. Chat GPT has not only been the world’s faster-ever growing application but has spurred people’s imaginations about what may lie ahead.

The first powered aircraft was built in 1903. Before that kites and balloons were in use, but it might have seemed crazy that objects with metal wings and a gasoline engine could fly. Until recently, it might have seemed crazy that other objects made of metal and silicon – computers – could think intelligently. But now many believe that to be possible in the near future.

ChatGPT was released in 2022, almost 120 years after the Wright brothers first flew their plane. ChatGPT, and other Large Language Models, do not exhibit artificial general intelligence (AGI). In essence, they make predictions of, and can generate, words that probabilistically follow next in a sentence. Large Language Models are essentially brilliant mimics of human language and lack the ability to perceive or reason about the world. They certainly are not conscious, although their skill in language generation can sometimes give the illusion that they are.

Excitement over AI is partly why the technology sector has dominated stockmarkets over recent months. The price of shares in Nvidia, whose chips are widely used in AI, has quadrupled since early 2023. The Magnificent Seven (Apple, Nvidia, Microsoft, Amazon, Google, Meta, Tesla) now account for 28% of the S&P 500 by market cap. An example of herding behaviour?

Investing in a passive fund tracking a market cap weighted index (such as the S&P 500) is not allocating an equal amount of money to each stock in that index but allocating more to the large cap stocks in the index. This is fine if they maintain their leadership, but historically this has not always been the case. The largest cap stocks in the S&P 500 in 1990 were Exxon, IBM, Loews, Raytheon, and Bristol- Myers Squibb. Which will they be in 2035? Perhaps not the same as they are today.

The recent divergence of the Magnificent Seven shows the need to analyse each company individually in depth, and not be caught up in the herd.

We would suggest caution. The economic outlook still remains very uncertain. As data from the US Federal Reserve shows, the Global Economic Policy Uncertainty Index is well above its 20-year average.

There is great uncertainty over the number and timing of rate cuts. The US Federal Reserve is looking for greater confidence that inflation is on a sustainable downward path, before cutting interest rates, but job growth remains strong, and services prices are still increasing. It is unclear where rates will be by the end of 2024.

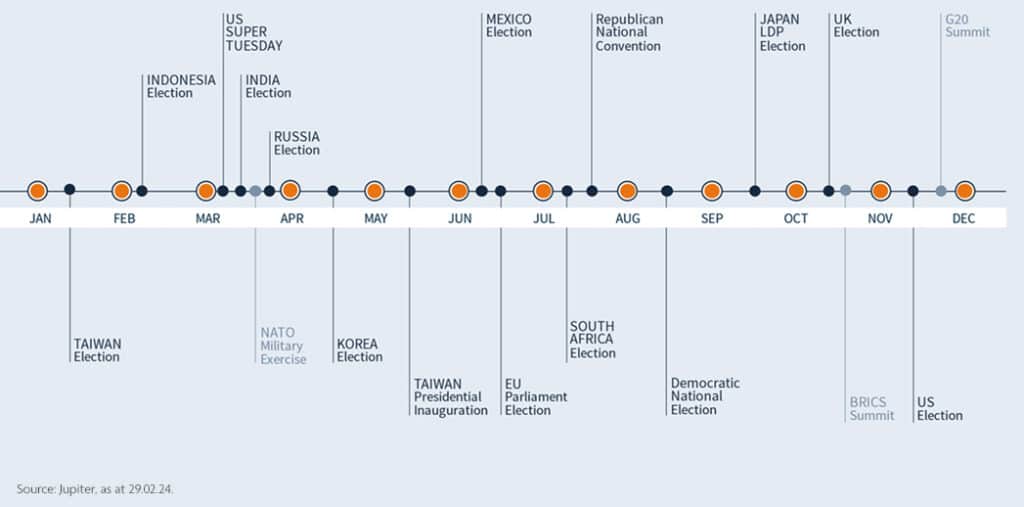

Part of the uncertainty is geopolitical, with wars in Ukraine and Gaza. In 2024, countries representing more than half the world’s GDP will have elections. The list of elections shown on the next page cumulates in the US election. That will probably be between Biden and Trump, but the result could easily be tipped either way by how many votes the main candidates lose to an outsider, such as Robert F Kennedy Jr.

Will there be a resurgence in populism? If so, there could be important consequences for global trade and stability. Potential risks include continued Russian expansionism and China’s designs on Taiwan.

Amidst all this uncertainty, we think the pursuit of diversification make sense. Our market neutral strategy is designed to provide genuine diversification, with returns not correlated to either equity or bonds. It is based on a large opportunity set and a repeatable, dispassionate approach. We don’t put much faith in stories. We prefer hard data.

In order to mitigate behavioural biases, we have developed a highly rigorous, systematic investment process. Rather than employing traditional techniques, such as manually scrutinising company annual reports, meeting management teams, and studying by hand third-party analysis, we prefer to use computer-based techniques to analyse huge volumes of publicly available information. This allows us to scrutinise a large universe of global stocks against our diverse set of proprietary stock selection criteria, which we have developed, scientifically researched and refined over years.

1 https://financesonline.com/how-much-data-is-created-every-day/

2 Alejandro Bernales, Marcela Valenzuela, and Ilknur Zer (March 2023), Effects of Information Overload on Financial Markets: How Much Is Too Much? Board of Governors of the Federal Reserve System, International Finance Discussion Papers, Number 1372. Available at https://www.federalreserve.gov/econres/ifdp/files/ifdp1372.pdf

Disclosure

The value of active minds: independent thinking

A key feature of Jupiter’s investment approach is that we eschew the adoption of a house view, instead preferring to allow our specialist fund managers to formulate their own opinions on their asset class. As a result, it should be noted that any views expressed – including on matters relating to environmental, social and governance considerations – are those of the author(s), and may differ from views held by other Jupiter investment professionals.

Important Information

Important Information: This document is intended for investment professionals* and is not for the use or benefit of other persons, including retail investors, except in Hong Kong. This document is for informational purposes only and is not investment advice. Market and exchange rate movements can cause the value of an investment to fall as well as rise, and you may get back less than originally invested. The views expressed are those of the individuals mentioned at the time of writing, are not necessarily those of Jupiter as a whole, and may be subject to change. This is particularly true during periods of rapidly changing market circumstances. Every effort is made to ensure the accuracy of the information, but no assurance or warranties are given. Holding examples are for illustrative purposes only and are not a recommendation to buy or sell. Issued in the UK by Jupiter Asset Management Limited (JAM), registered address: The Zig Zag Building, 70 Victoria Street, London, SW1E 6SQ is authorised and regulated by the Financial Conduct Authority. Issued in the EU by Jupiter Asset Management International S.A. (JAMI), registered address: 5, Rue Heienhaff, Senningerberg L-1736, Luxembourg which is authorised and regulated by the Commission de Surveillance du Secteur Financier. For investors in Hong Kong: Issued by Jupiter Asset Management (Hong Kong) Limited (JAM HK) and has not been reviewed by the Securities and Futures Commission. No part of this document may be reproduced in any manner without the prior permission of JAM/JAMI/JAM HK.

*In Hong Kong, investment professionals refer to Professional Investors as defined under the Securities and Futures Ordinance (Cap. 571 of the Laws of Hong Kong) and in Singapore, Institutional Investors as defined under Section 304 of the Securities and Futures Act, Chapter 289 of Singapore.