By Jens Nystedt and Oliver Faltin-Trager, Emso Asset Management – Prior to the Covid-19 pandemic, it was increasingly difficult to find fixed income assets with attractive nominal or real yields. This trend is expected to continue as G7 government yields are likely to hover near zero for the foreseeable future, and it is difficult for us to envision a world where economic output meaningfully accelerates as deflation remains a bigger risk than inflation.

This environment is likely to compel G7 central banks to continue providing monetary stimulus and capping real yields. As a result, we think that the performance of typical 60/40 portfolio allocation between DM equities and DM fixed income will likely lag the historical returns that this mix has achieved over the last two decades. With real and nominal government bond yields already low, we believe that the 40% fixed income portion of the 60/40 portfolio will no longer be able to act as a shock absorber during equity sell-offs. In addition, while there is limited upside to government bond positions that are already at zero or negative yields, we also believe that investors may be underestimating the asymmetric risk of these longer duration assets selling off materially during a period in which a stagflation scenario could develop in the G7.

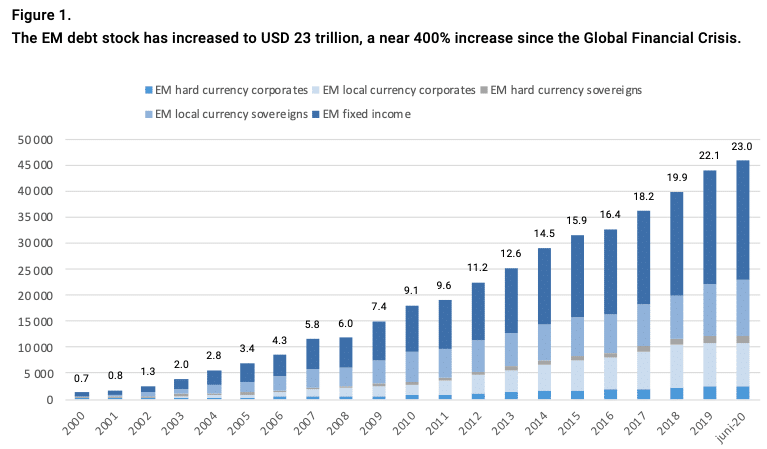

We believe that allocators will have to look increasingly towards non-traditional asset classes to deliver the yield and diversification that government fixed income has traditionally delivered. It is clear that allocations to “hybrid” fixed income asset classes, which offer equity-like returns but with traditional fixed income volatility levels, will likely increase. We think that EM fixed income should play a more significant role in these allocations due to their generally favorable risk/reward characteristics and the availability of higher nominal and real yields. EM fixed income is now a USD 23 trillion asset class that offers ample diversification, opportunity, and liquidity (see Figure 1). Historically, institutional investors in the US and Europe have strategically underinvested in EM due to home bias considerations or general risk concerns. However, given that the zero-yield world is likely to remain in place for the foreseeable future, we believe allocations to “hybrid” asset classes, including EM fixed income, should be significantly larger going forward. Jan Loeys and Shiny Kurdu, strategists at JP Morgan, for example, recently examined the optimal top-down macro asset allocation with forward looking return expectations and arrived at a 20/40/40 split of bonds/hybrid/equities.

Investors’ risk concerns about EM credit quality were more justified in the late 1990s and early 2000s when EM crises were quite frequent. Volatility in Russia, which led to the Long-Term Capital Management crisis, and general conditions in Argentina and Brazil in the 2000s left their mark on investors. In recent years, however, EM sovereigns have generally only experienced extreme volatility due to global shocks, including the Global Financial Crisis in 2008-09 and, currently, the Covid-19 pandemic. However, even these shocks have had a less significant impact on EM, due to the absence of fixed exchange rates and the development of local fixed income markets.

We believe that the secular improvements in emerging market fundamentals are not yet fully appreciated by developed market investors nor favorably priced into emerging market fixed income assets. It is important to fully examine the EM fixed income opportunity set and discuss the key characteristics of some of the major EM fixed income asset classes, the importance of EMFX hedging in mitigating drawdowns, and what role EM fixed income should play in an optimal global fixed income portfolio.

When we breakdown EM fixed income into its key components, we find specific opportunities in each of them. We believe that EM sovereign hard currency fixed income, which consists of issuers with a broad range of credit quality and risk exposures, offers ample opportunity for diversification and bottom-up research. After the recovery in EM, year-to-date EM sovereign IG returns have recovered all their losses and are now positive year-to-date, and, in our view, the EM non-IG segment still has value, particularly in frontier names where EM specialist experience can help to identify value and avoid credits with poor fundamentals

EM corporate bonds, whether hard or local currency, account for most of the outstanding EM debt stock. Asian issuers account for nearly 40% of the debt outstanding and have seen some of the most rapid growth during recent years. With over 700 issuers in the JP Morgan CEMBI BD Index, we believe that EM corporates can also offer many attractive idiosyncratic opportunities across regions and sectors at an attractive yield in current market conditions.

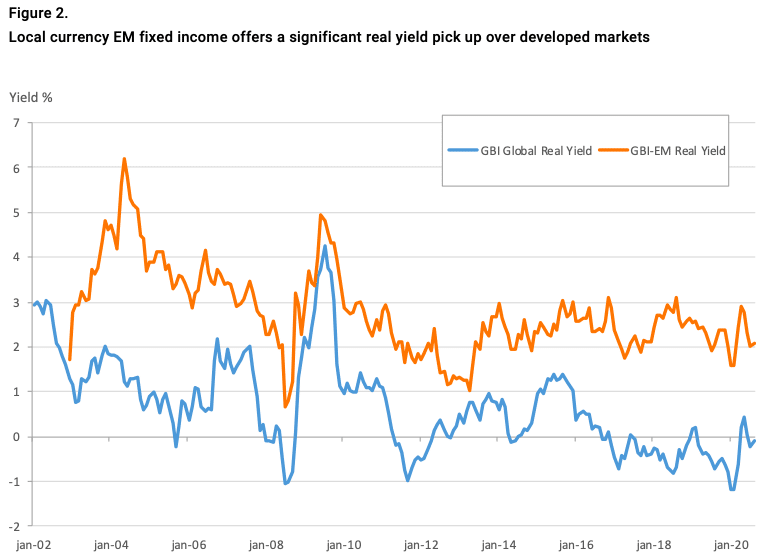

There are also many opportunities in local currency denominated fixed income assets for selective investors. Ongoing EM quantitative easing efforts, while supportive of a flattening curve trend, remain a headwind to EMFX outperformance. Yields for the key benchmark, the JP Morgan GBI-EM Global Diversified Index (GBI-EM), have declined significantly since mid-2018. However, on a spread to developed markets, many IG-rated EM local currency fixed income markets still offer attractive pick-ups, especially in real rates. Due to its volatility, EMFX has been a significant driver of local fixed income returns for developed market investors, and its annual performance has ranged from -17.6% to +5.8% since 2011.

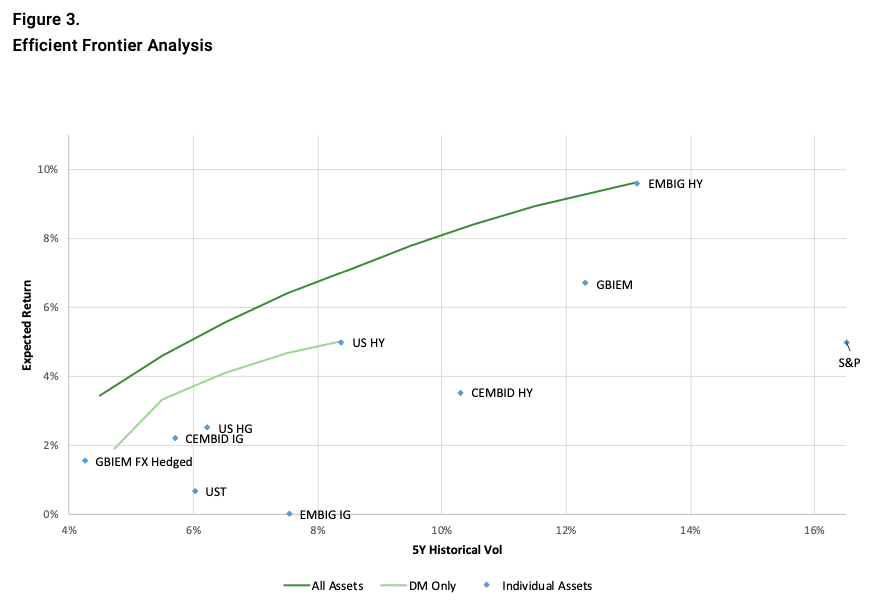

For our analysis, (Figure 3 below) we performed a mean-variance portfolio optimization exercise to bring these asset classes together to determine how they could provide value for a developed market investor by adding EM fixed income assets to a typical US fixed income portfolio. When considering the optimal portfolio allocation to emerging market fixed income, key inputs are return and correlation assumptions between asset classes. At Emso, we prefer to use forward looking returns. We typically generate a 12-month forward return expectation per asset class for the first year, and use 10-year historical returns thereafter. We break down EM fixed income into hard currency sovereigns, corporates, local currency sovereigns, and FX exposure, using the main JP Morgan EM benchmarks. We then implement a mean-variance portfolio optimization using our 12-month forward return expectations and empirical volatilities and correlations.

Emso has found that including EM fixed income assets expands the efficient frontier. Figure 3 includes the liquid USD fixed income efficient frontier with and without EM assets. This illustrates the degree to which EM assets expand the efficient frontier outwards due to lower correlations, higher yields, and acceptable expected returns. Raising the efficient frontier by more than 1 percentage point for a given level of volatility implies a roughly 20% increase in its Sharpe ratio. High yield hard currency sovereign bonds are particularly useful for expanding the efficient frontier given a higher yield than US HY, but with a lower correlation of below one.

US HY credit essentially defines the efficient frontier for US fixed income, and its correlation with EM fixed income can vary significantly over time. Unsurprisingly, EM corporates tend to have the highest correlation with US HY, while local sovereign bonds have the lowest. Correlations have increased recently as a result of the Covid-19 sell-off and subsequent coordinated monetary policy support. However, rolling correlations remain below 1, indicating that even EM corporates offer some diversification benefit to US HY investors. EM sovereign HY, as well as local fixed income exposures (FX hedged), offer attractively low correlations, particularly during less volatile periods.

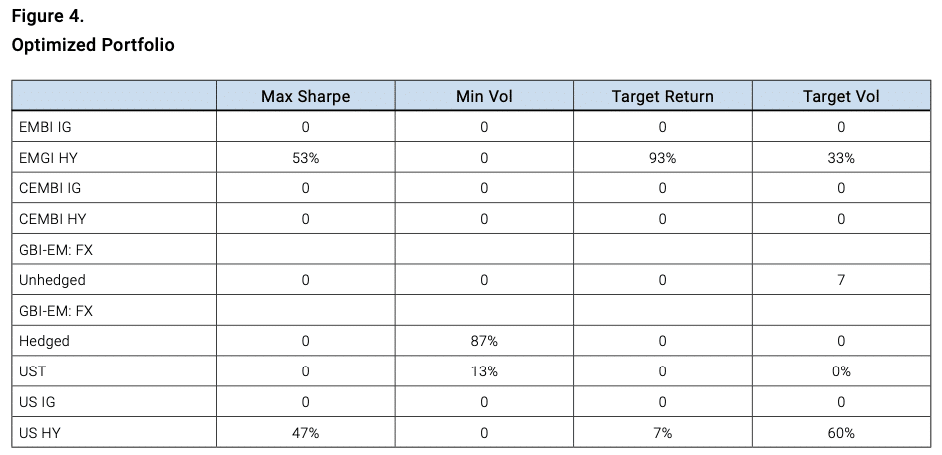

There are several ways to optimize a portfolio that includes EM fixed income assets. Clearly the optimal portfolio depends on what the investor is targeting: high Sharpe, high return, or low volatility. Using our most recent estimates, the maximum Sharpe portfolio in this framework is a combination of US HY and EMBI HY driven by the currently attractive valuations in EM sovereign HY as well as longer-term return potential and its diversification value (see Figure 4).

Given the future challenges to returns, Loeys and Kurdu recommend a 20/40/40 allocation to bonds/ hybrids/equities for investors who do not want to cut equities too aggressively. Although we do not include a range of hybrids in this exercise, this portfolio optimization exercise suggests that within the hybrid component, a higher allocation to EM fixed income can work across a range of optimization targets. This seems both intuitive and consistent with our empirical portfolio optimization results given current valuations and empirical correlations. For example, in a maximum Sharpe portfolio, as Figure 4 below suggests, nearly 50% of the hybrid bucket could be filled by making an allocation to EM sovereign HY.

In conclusion, as the traditional asset allocation model is likely to be challenged over the next decade, we believe that investors are going to seek out more attractive risk/return opportunities outside of the 60/40 model including hybrid fixed income. At Emso, we believe that EM fixed income should be a significant part of that new mix given the depth and breadth of the asset class, its relatively high yield, the diversification opportunities it provides, and the exposure that it provides to the faster growing parts of the global economy. Active management could add incremental returns, if paired with a successful EMFX hedging overlay. Moreover, we currently find EM HY exposure particularly attractive, but bottom-up research capabilities remain a critical component of the security selection process to avoid exposure to assets with genuinely fragile fundamentals given the shock to global growth that Covid-19 has generated.

Photo by Romain Tordo on Unsplash

This article featured in HedgeNordic’s report Alternative Fixed Income Strategies.