Stockholm (HedgeNordic) -Given the heterogeneous nature of hedge fund strategies, identifying the winning funds at the Nordic Hedge Award solely based on traditional absolute or even risk-adjusted performance measures may not always be the best approach. Indeed, risk-adjusted measures such as the Sharpe ratio are a good starting point in the process of selecting the best hedge funds. After all, the name of the game for many hedge funds is to provide investors with high risk-adjusted returns, regardless of whether the return figures are singledigit or double-digit.

However, the Sharpe ratio and other measures do not tell the whole story. Due to the unique nature of hedge fund strategies, some of which may invest in relatively illiquid asset classes or may exhibit asymmetric return profiles, the traditional risk To determine the winners, HedgeNordic employs a scoring system that equally weights a quantitative score – that reflects several parameters such as short- and longer-term absolute, relative and risk-adjusted returns – and a qualitative score, which considers “qualitative” or “soft” factors.

The qualitative score is determined by a jury board comprised of industry professionals, with their voices accounting for half of the final scores that determine the rankings at the Nordic Hedge Award.

As Michael Halling, Associate Professor at the Stockholm School of Economics and Research Fellow at the Swedish House of Finance, tells HedgeNordic: “to select the truly deserving award winners, it is important to ask industry experts to comment on and evaluate the nominated funds.”

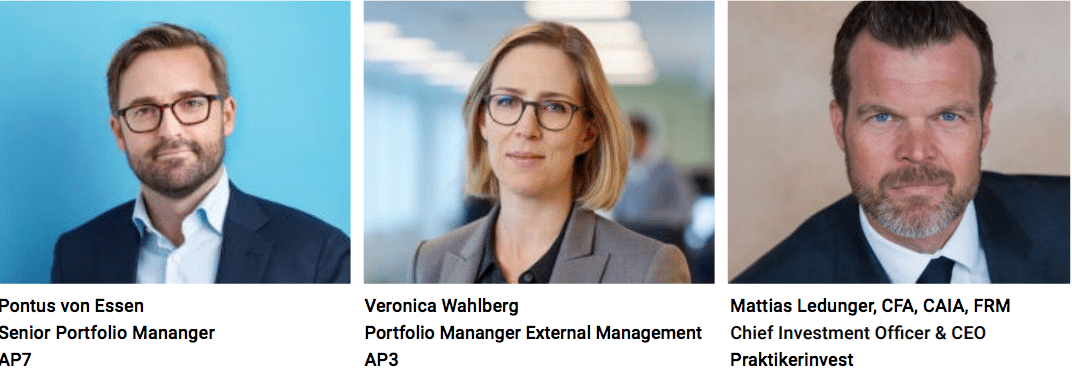

For the 2019 Nordic Hedge Award, the assembled jury board included Pontus von Essen, Head of Fixed Income, FX & Alpha at AP7, Veronica Wahlberg, Portfolio Manager of External Management at AP3, Mattias Ledunger, CEO of alternative investment vehicle Praktikerinvest and Chief Investment Officer of Praktikertjänst Pension Trust, Gustav Karner, Chief Executive Officer and Chief Investment Officer at Apoteket’s Pension Fund, Mika Jaatinen, Portfolio Manager of Elo’s Hedge Fund Investments, and Linsay McPhater, Senior Portfolio Manager at Nordea Wealth Management.

The members of the jury are asked to make a qualitative assessment of the funds that have been nominated through the quantitative screening codeveloped with the Swedish House of Finance at the Stockholm School of Economics. The jury members cast their final judgment based on various criteria, with the board being encouraged to overweight any qualitative criteria such as reputation, quality of communication, transparency and other characteristics relative to quantitative, performancebased criteria. The qualitative criteria may also include longevity, work ethics, sustainability, alpha generation, uniqueness, innovation, asset raising capacities, administrative setup, or any other relevant characteristics.

WHAT PURE PERFORMANCE NUMBERS CANNOT TELL ABOUT A HEDGE FUND?

The jury board assembled for the 2019 Nordic Hedge Award corroborates HedgeNordic’s view that pure performance measures, risk-adjusted or not, may now always tell the whole story. Linsay McPhater, a senior portfolio manager focusing on alternatives at Nordea Wealth Management, tells HedgeNordic that “performance numbers only tell one side of the story.” According to McPhater, “one should also assess the business aspect,” including “management, the culture of integrity, operational efficiency, disciplined and rigorous investment process, investment strategy, risk oversight, AuM growth and the client interface.” Last but certainly not least, “hedge funds must have an opaque structure, so we can see their underlying investments, so transparency is a key aspect,” argues McPhater.

Mika Jaatinen, who is Portfolio Manager of Hedge Fund Investments at Finnish employment pension company Elo, agrees. “Numbers cannot tell about a hedge fund’s culture,” Jaatinen tells HedgeNordic. According to Jaatinen, an understanding of the culture warrants questions such as: “How are organisations managed? How do they operate during times of crisis? How is the younger generation of managers and analysts trained and encouraged to take a more active and value-adding role in the organisation?” Jaatinen reckons that qualitative aspects such as “the company culture, all of their stakeholders (i.e. all third parties that are integral for running their operations), the current status of the management team” are essential in the evaluation of hedge funds. “Are they too rich and lazy to care about managing capital?” is a question worth asking, according to Jaatinen.

Gustav Karner, CEO and CIO at Apoteket’s Pension Fund, reckons that the custody, administrator and auditor of a hedge fund should not be overlooked either. In addition, a qualitative-based assessment can help identify hedge funds with a “strong risk culture,” which may not always be reflected in quantitative measures, particularly for funds with limited track records. Funds that are “closed or softclosed usually speaks for quality”, Karner points out another qualitative aspect worth considering.

THE ROLE AND VALUE OF HEDGE FUNDS

On the question of what is the role and value of hedge funds for institutional investors, Pontus von Essen of AP7 considers that “expertise and knowledge sharing” is the primary role of hedge funds, “above the other two components that they bring to the table: absolute return and diversification.” According von Essen, “hedge funds have the opportunity to be very focused on their particular niche, thereby providing a piece of the puzzle to an institutional investor in the form of expertise and knowledge sharing.” Pontus von Essen reckons that “it is hard for an institutional investor to internally create the right environment for these niche strategies to take off” and the role of hedge funds is “similar to the role of start-ups for large corporations in many other businesses.”

According to Linsay McPhater, “at a general level, the value of hedge funds is to maximise investor returns and eliminate risk.” She stresses that “hedge funds are designed to not correlate or behave like other investments.” During significant stock market declines, “hedge funds are expected to experience lower loses or even generate a positive return,” says McPhater. “Therefore, investors view hedge funds as a diversifier and risk reducer in their wider portfolios.” The other members of the jury board share the same view.

Mika Jaatinen, for instance, says that hedge funds should “act as an alternative source and stream of returns that do not correlate too much with other asset classes.” Mattias Ledunger, who is the CEO of alternative investment vehicle Praktikerinvest and CIO of Praktikertjänst Pension Trust, reckons that “the role of hedge funds is to add alpha, and why not beta too, particularly in sectors and niches that cannot be managed as efficiently in-house.” Gustav Karner also corroborates Ledunger’s view, saying that the role of a hedge fund is “to act as a diversifier that generates equity-like returns in the long run.”

WHICH HEDGE FUNDS CAN CLAIM SUCCESS?

The heterogeneous nature of hedge fund strategies makes the distinction between a successful and not-so-successful hedge fund quite blurry. “There are many hedge fund different strategies, all doing different things in different market environments, so it is hard to compare them and define a successful one,” Linsay McPhater tells HedgeNordic. For McPhater, “a successful hedge fund is one that performs as we would expect, in both up and down markets, and perform in the manners they claim to do so, therefore meeting its aims.” The annually-held Nordic Hedge Award strives to identify and distinguish the most successful hedge funds by relying on a combination of quantitative and qualitative measures. According to Mattias Ledunger, “the awards handed out at the Nordic Hedge Award add another opportunity and dimension by which to strive for excellence for locally-based funds.” McPhater agrees, saying that “the Nordic Hedge Award allows a common ground where Scandinavian players can be judged.” Ledunger points out that “winning an award at the Nordic Hedge Award adds a stamp of approval.”

The 2019 Nordic Hedge Award was supported by:

This article featured in: 2019 Nordic Hedge Award – The Highlights

Picture: (c) Sergey-Nivens—shutterstock.com