By Andrew Beer, Co-Founder of DBi: Managers of CTA hedge funds and mutual funds often argue that complexity leads to higher alpha generation. After all, why else would anyone bother to invest in hundreds of futures, run dozens of models and overlay risk controls? Conveniently, in the minds of many allocators, complexity can justify a higher fee structure.

The growth of the CTA ETF space provides an opportunity to test this thesis. Broadly speaking, CTA ETFs are simpler: fewer instruments, fewer models. The investment rationale is that daily disclosure of esoteric positions could increase the risk of getting front fun. As importantly, given lower fees in ETFs, managers of hedge funds and mutual funds have an incentive to claim that they are keeping their “best stuff” for higher fee products.

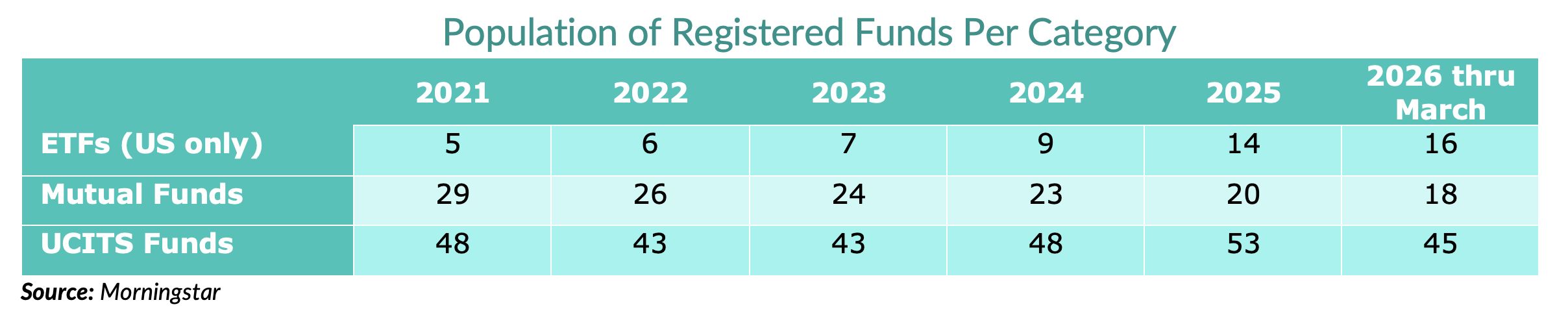

Based on Morningstar data, there are sixteen CTA ETFs today, more than half of which have launched in the past few years. The UCITS fund pool is surprisingly robust at 45 funds, and many have track records back to the early 2010s. The US mutual fund universe is a narrower list of 18 funds, down from nearly 30 five years ago, and most of which have reasonably long track records. To our knowledge, there is only one pure play UCITS ETF — which we launched in 2025; given the paucity of data, we will simply exclude this category.

To evaluate the question above, we start with the SG CTA index. The index is an equally weighted measure of the daily performance, net of all fees and expenses, of the twenty largest CTA hedge funds. Reliable data stretches back to 2000. Not surprisingly, most institutional allocators view this as the index gold standard: a window into the average performance of luminaries such as Winton, Man AHL, AQR, AlphaSimplex, Graham, Campbell, CFM, Systematica, Lynx, TransTrend and others (quite unusually, AlphaQuest was removed on March 1). The constituents are available here. This data is used primarily by allocators to build capital markets assumptions (“zero correlation to stocks and bonds,” “crisis alpha during the 2022, the GFC and dotcom crisis,” etc.) and benchmark managers.

Allocators cannot invest per se in the SG CTA index; it is merely the reported average returns of the “strategy.” Given manager dispersion, the solution for most institutional investors has been to approximate the index returns by intelligently investing in several constituents. For wealth managers, though, a second issue is that their clients generally cannot invest in hedge funds due to accreditation, investment minimums and other issues. Registered funds seek to solve this “access” issue. As we have written about extensively, “liquid alternative” versions of actual hedge funds have a truly dismal track record: the Wilshire Liquid Alternative index has delivered slightly more than 2% per annum over 15 years, roughly one third of the PivotalPath Hedge Fund Composite.

Hence the key question for allocators is whether the CTA “strategy” works as well in registered funds. To test this, we used Morningstar data to create equally weighted composites of monthly returns of US Mutual Funds, UCITS funds and (US)ETFs. We then compare those composites to the results of the SG CTA.

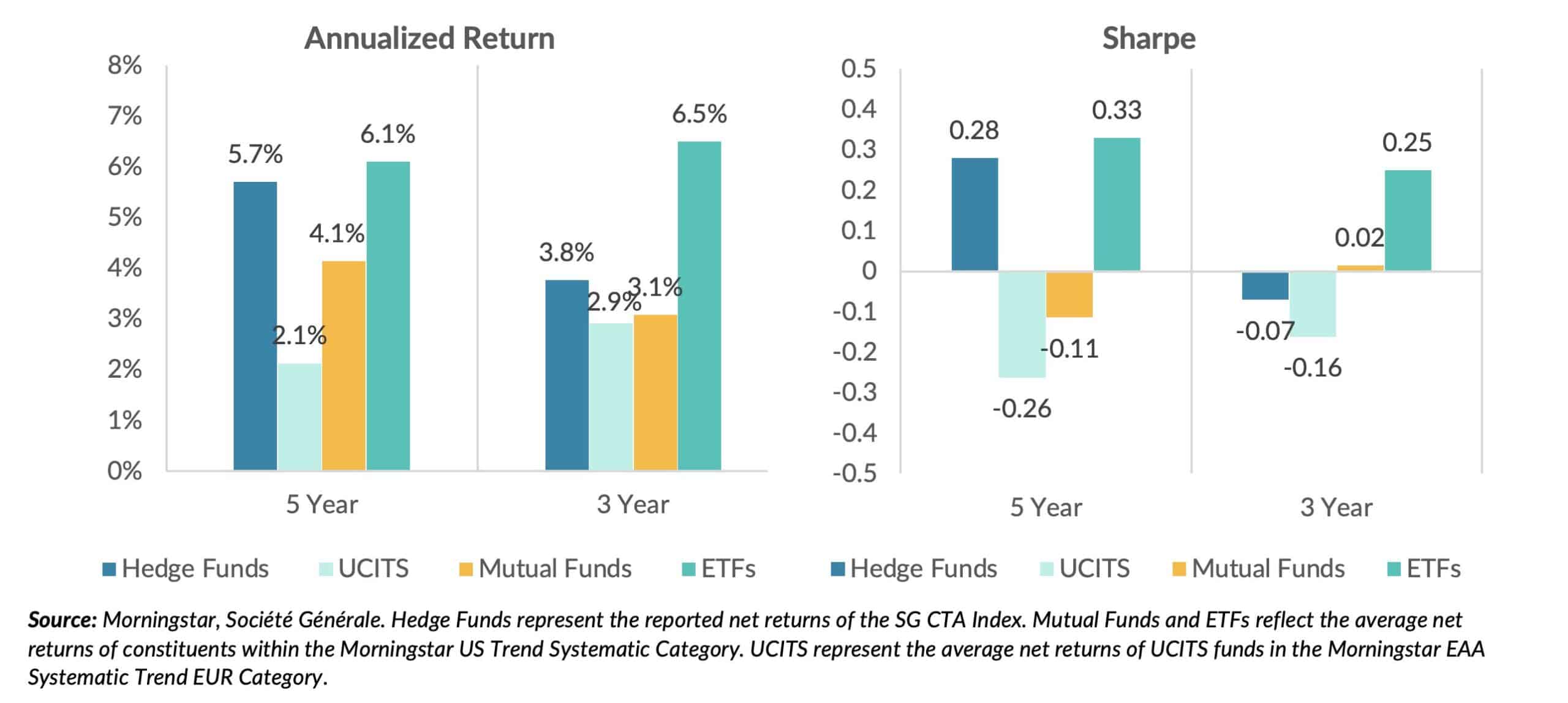

Given the recent growth of the CTA ETF space, we focus on the past three and five years. Recent results are striking. While mutual and UCITS funds have trailed hedge funds, CTA ETFs have outperformed on both an absolute and risk-adjusted basis, especially during the past three years – a difficult period for the space when modeling “enhancements” theoretically should have added value.

We see three possible explanations.

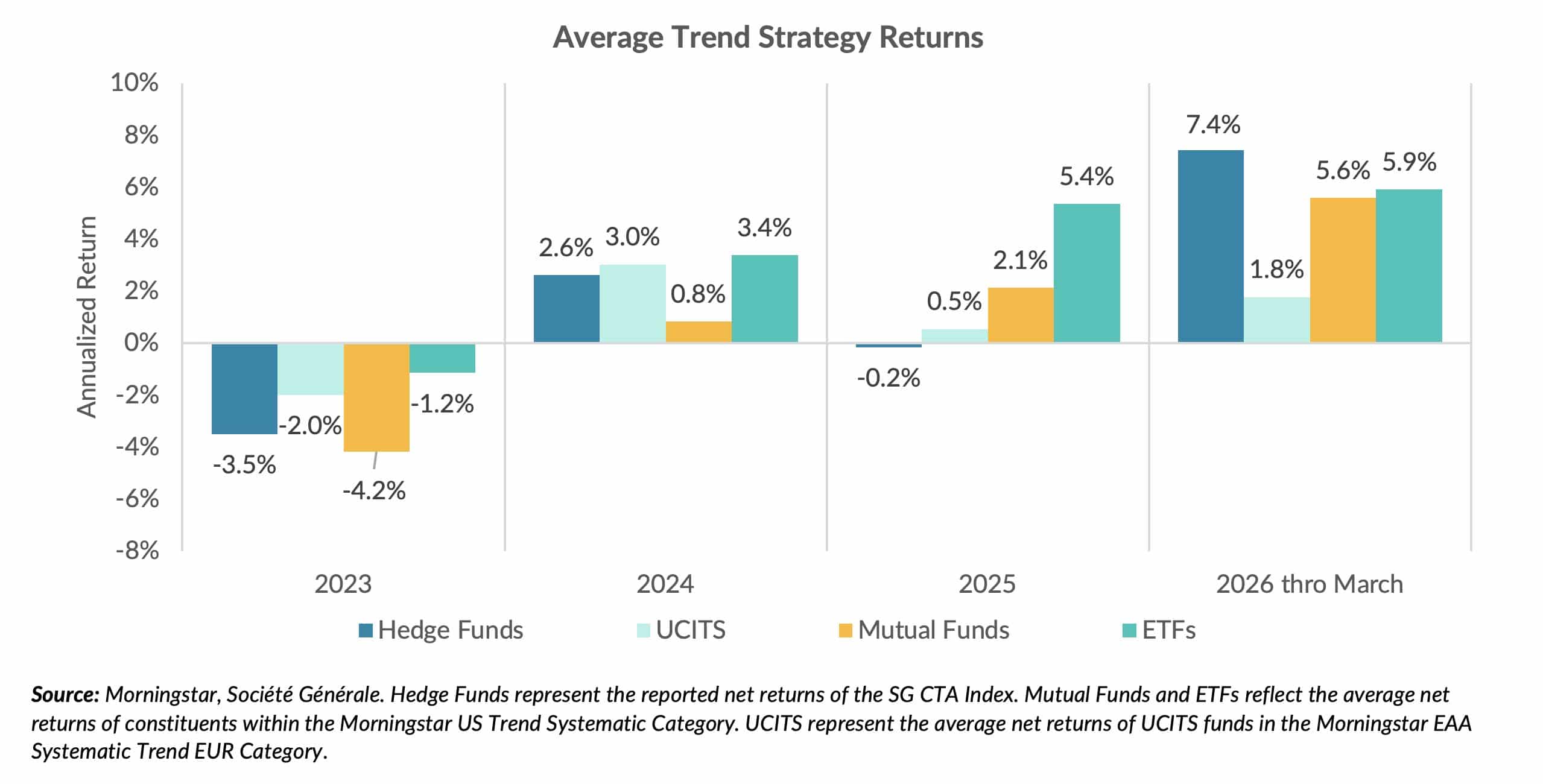

The first is that these windows might be skewed by selection bias. Essentially, the argument would be that a few ETFs happened to do well, they raised assets, rivals launched competitors, and as the field expands, performance should revert to the mean. Yet as the field of ETFs has grown since 2023 (see table 1), outperformance has persisted, with the notable exception of the first quarter of 2026.

A second explanation is that this might have been a uniquely good period for simpler models. Goldman Sachs and other serious analysts of the space have presented evidence that longer term models that focus on major markets have outperformed in recent year. Supporting this thesis, ETFs run by AlphaSimplex and Man AHL have outperformed their own (more complicated) mutual funds.

A more controversial explanation is that the simplicity of CTA ETFs is a strength, not a weakness. We discussed it last Fall here. The “simplicity is better” argument is that CTAs generate alpha by being early, contrarian and right in a handful of trades in major markets. Diversification beyond a certain point has diminishing benefits. Trading costs can rise geometrically in more esoteric markets and offset theoretical benefits. Short term models can get kicked out of important trades and, with Sharpe ratios close to zero, are a drag on returns. Risk controls can get head-faked half the time. If this framework, the lower fees of CTA ETFs translate into more alpha for clients. (In a forthcoming article, we will explore whether further savings are available through more efficient implementation.)

If ETFs match or outperform hedge funds and mutual funds going forward, the implications for allocators are profound. Why tolerate lower risk-adjusted returns from higher cost products? Why accept anything longer than daily liquidity? Could a low cost, passive ETF that invests efficiently across the CTA ETF landscape become an “investable beta” like the S&P 500? And would this then expand the CTA pie?

Several years ago, CTA ETFs were derided as cheap knock offs. Today, they seem like progress.