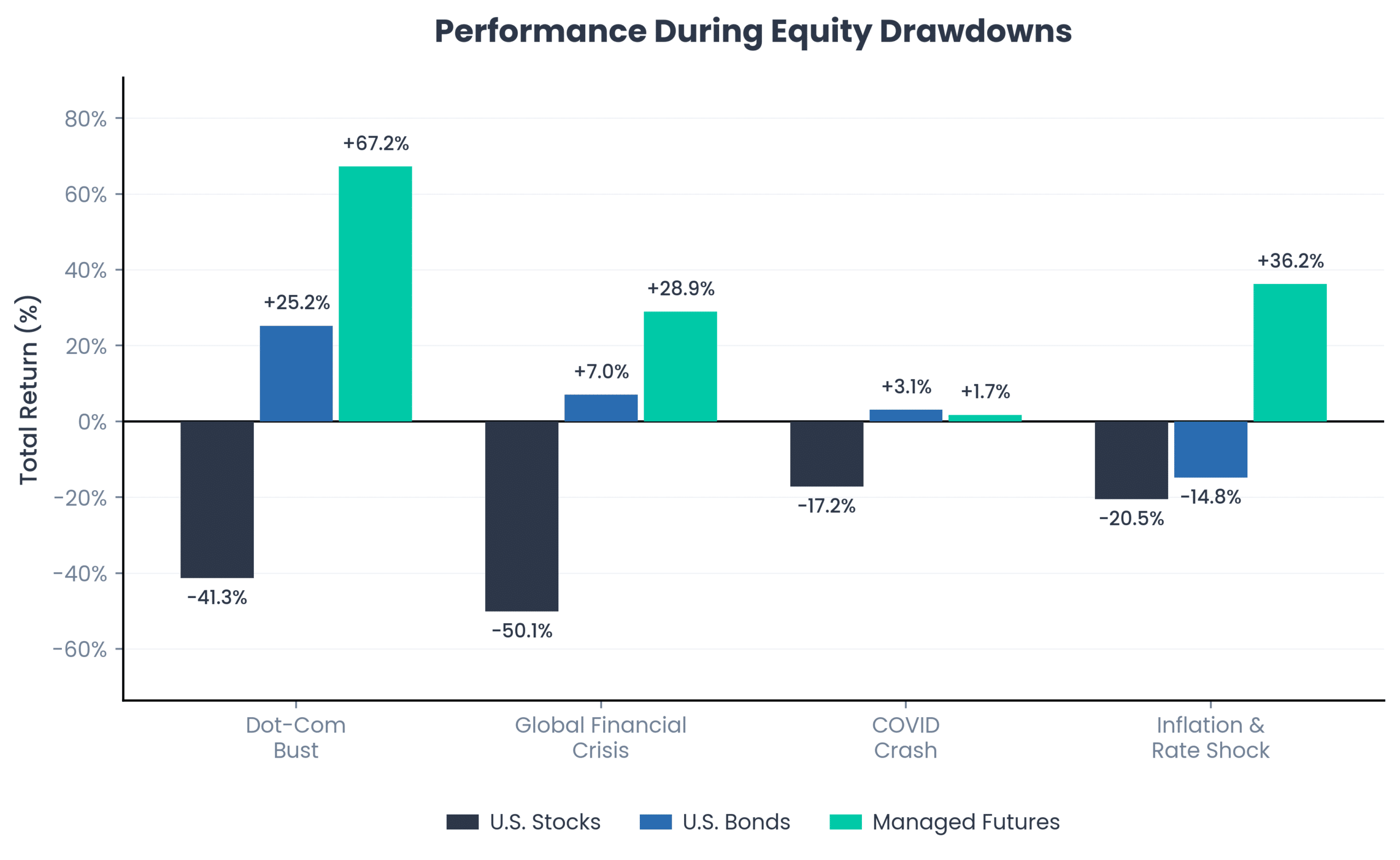

By Corey Hoffstein, Co-Founder, CEO and CIO at Newfound Research: The case for managed futures as a portfolio diversifier is well established. During the four major equity drawdowns since 2000, the SG Trend Index delivered positive returns every time, while stocks suffered deep losses and bonds offered inconsistent and inadequate offsets (Exhibit 1). Yet despite this track record, many allocators still struggle to maintain the allocation. The problem is not with the diversifier, but with how we diversify.

Source: Bloomberg. U.S. Stocks is the S&P 500 Index (“SPX”). U.S. Bonds is the Bloomberg US Aggregate Bond Index (“LBUSTRUU”). Managed Futures is the Société Générale Trend Index (“NEIXCTAT”), which is net of management fees, performance fees, and transaction costs. Returns for both U.S. Stocks and U.S. Bonds are gross of all fees. Returns are gross of taxes. Returns assume the reinvestment of all distributions. Past performance is not indicative of future results. Periods shown: Dot-Com Bust (August 2000 – September 2002), Global Financial Crisis (October 2007 – February 2009), COVID Crash (December 2019 – March 2020), Inflation & Rate Shock (December 2021 – September 2022). Periods selected reflect the largest drawdown periods of U.S. Stocks since index joint inception. You cannot invest in an index. Period is 12/31/1999 through 12/31/2025.

The Cost of Making Room

Most allocators do not start with a blank portfolio. They already own stocks and bonds and have stakeholders whose expectations are anchored to those allocations. This means traditional diversification is almost always a process of addition through subtraction: sell an existing holding to buy something new. That process introduces two challenges.

The first is numerical. Deciding what to sell requires estimating expected returns, volatilities, and correlations for both what we are giving up and what we are buying. These are notoriously difficult parameters to pin down, and small errors can flip the conclusion entirely.

The second is behavioral. We are hiring managed futures specifically because it behaves differently from stocks and bonds, but that very difference is what makes the allocation difficult to stick with.

CEO & CIO, Newfound Research.

Consider what has become the alternative product marketer’s new 60/40: the 50/30/20 (50% stocks, 30% bonds, 20% managed futures), which carves 10% from stocks and 10% from bonds to fund a managed futures sleeve. The 50/30/20 largely abandons any numerical precision by simply asserting that a 50/50 blend of stocks and bonds is the right swap for managed futures.

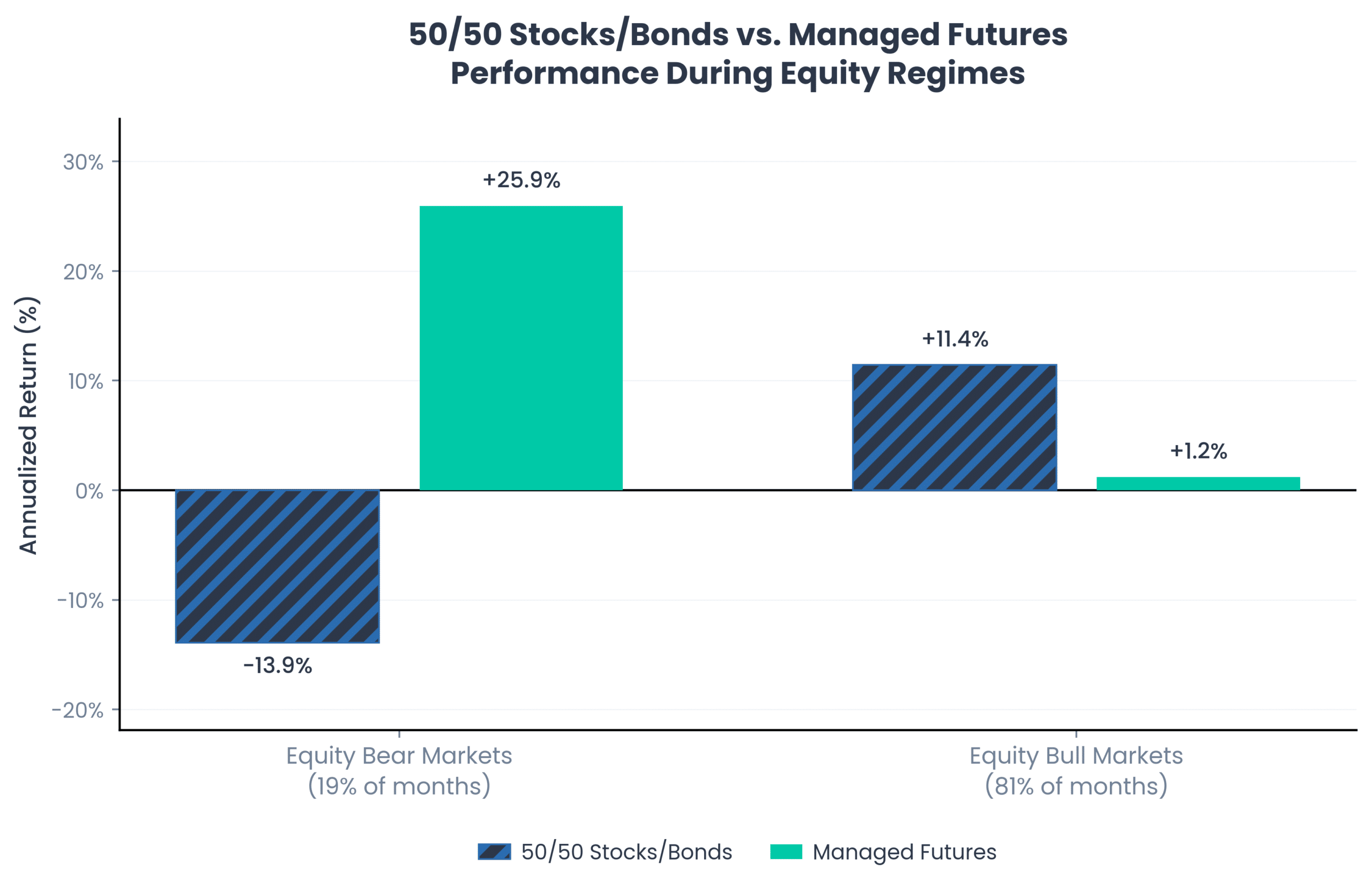

And the behavioral challenge is on full display: from January 2000 through December 2025 the trade required selling a blend that returned +11.4% annualized during the 81% of months classified as equity bull markets and buying managed futures, which delivered just +1.2% over the same periods. During the other 19% of months, managed futures returned +25.9% annualized while the 50/50 blend fell –13.9% (Exhibit 2). The payoff was real, but infrequent enough to test anyone’s conviction.

Source: Bloomberg. 50/50 Stocks/Bonds is a monthly rebalanced blend of the S&P 500 Index (“SPX”) and Bloomberg US Aggregate Bond Index (“LBUSTRUU”). Managed Futures is the Société Générale Trend Index (“NEIXCTAT”). All portfolios are rebalanced monthly. You cannot invest in an index. Returns are gross of all fees. Returns are gross of taxes. Returns assume the reinvestment of all distributions. Past performance is not indicative of future results. Equity Bear Markets defined as the four largest drawdown periods of U.S. Stocks since index joint inception. Equity Bull Markets defined as the periods from 12/31/1999 through 12/31/2025 not specified in the Bear Market periods. Period is 12/31/1999 to 12/31/2025.

A Better Way: Stack, Don’t Swap

Even for the allocators who endured the estimation uncertainty, the years of underperformance relative to the assets sold, and the difficult conversations with stakeholders, the historical results have been underwhelming. Over the period from January 2000 through December 2025, the 50/30/20 improved risk-adjusted returns (the Sharpe ratio rose from roughly 0.51 to 0.61), but the headline return barely moved, from approximately 6.5% to 6.6% annualized. Ten basis points. For 25 years, the diversification benefit was almost entirely offset by the reduction in stock and bond exposure.

Return stacking offers a different framework. The concept is a more generic implementation of portable alpha: use capital-efficient instruments to overlay one return stream on top of another. The difference is that what we are “porting” here is better described as hedge fund beta (systematic trend-following is well-documented and broadly accessible) rather than scarce single manager alpha.

In practice, a turnkey structure, often implemented through a single ETF, replaces the cash collateral that managed futures strategies typically sit on with underlying equity or fixed income exposure. This approach seeks to deliver both the core portfolio return and the managed futures excess return at the same time. In other words, instead of selling stocks and bonds to make room, the allocator can maintain their full stock/bond allocation and add managed futures exposure as an overlay.

As an example, a return-stacked 60/40/20 portfolio would have historically delivered approximately 7.4% annualized over the same period, compared to 6.5% for the traditional 60/40 and 6.6% for the make-room approach.

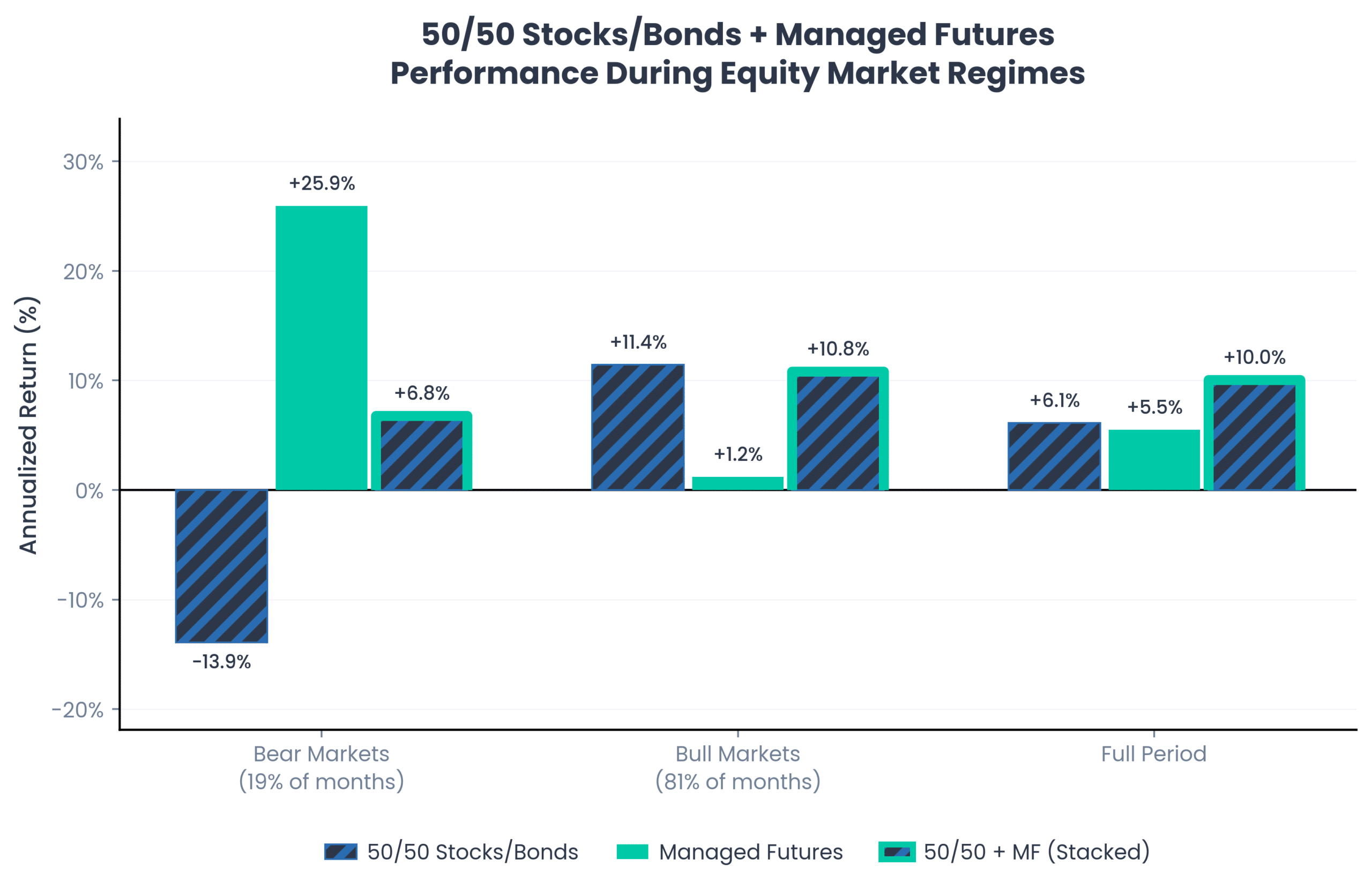

At its fullest historical expression, stacking 100% managed futures excess returns on top of the 50/50 blend would have returned +10.8% annualized during bull markets, nearly matching the 50/50’s +11.4%. During bear markets, it would have returned +6.8% versus –13.9% for the 50/50 alone (Exhibit 3). Over the full period, stacking delivered 10.0% annualized returns compared to 6.1% for the 50/50 and 5.5% for managed futures individually.

Source: Bloomberg. 50/50 Stocks/Bonds is a monthly rebalanced blend of the S&P 500 Index (“SPX”) and Bloomberg US Aggregate Bond Index (“LBUSTRUU”). Managed Futures is the Société Générale Trend Index (“NEIXCTAT”). 50/50 + MF (Stacked) adds the monthly excess return of the SG Trend Index over T-bills to the monthly rebalanced 50/50 blend. All portfolios are rebalanced monthly. You cannot invest in an index. Returns are gross of all fees. Returns are gross of taxes. Returns assume the reinvestment of all distributions. Past performance is not indicative of future results. Equity Bear and Bull Market definitions consistent with Exhibit 2. Period is 12/31/1999 to 12/31/2025.

Beyond Defense: A Tool for Growth Mandates

The potential diversification benefits that managed futures introduce to a traditional stock/bond portfolio are most often framed through the lens of risk management, but return stacking opens a compelling avenue for growth-oriented allocators as well. The traditional path to excess returns within an equity mandate is security selection, yet according to the SPIVA Scorecard, over 90% of active U.S. large-cap equity funds have underperformed the S&P 500 over rolling 15-year periods. Return stacking offers an alternative: rather than pursuing alpha within core equity beta, an allocator can layer additional, complementary return streams on top. For example, a growth allocator could hold 100% equity exposure and add a 20% managed futures excess return overlay. Historically, this stacked approach would have delivered roughly 8.7% annualized compared to 7.7% for the S&P 500 alone, introducing approximately 2.7% annualized tracking error.

Why Not Just Use Higher-Volatility Funds?

Astute readers might point out that higher-volatility managed futures funds are, in a sense, already capital efficient. A fund running at 2x or 3x the typical volatility allows the allocator to achieve the same notional exposure with a smaller allocation, freeing up capital for stocks and bonds.

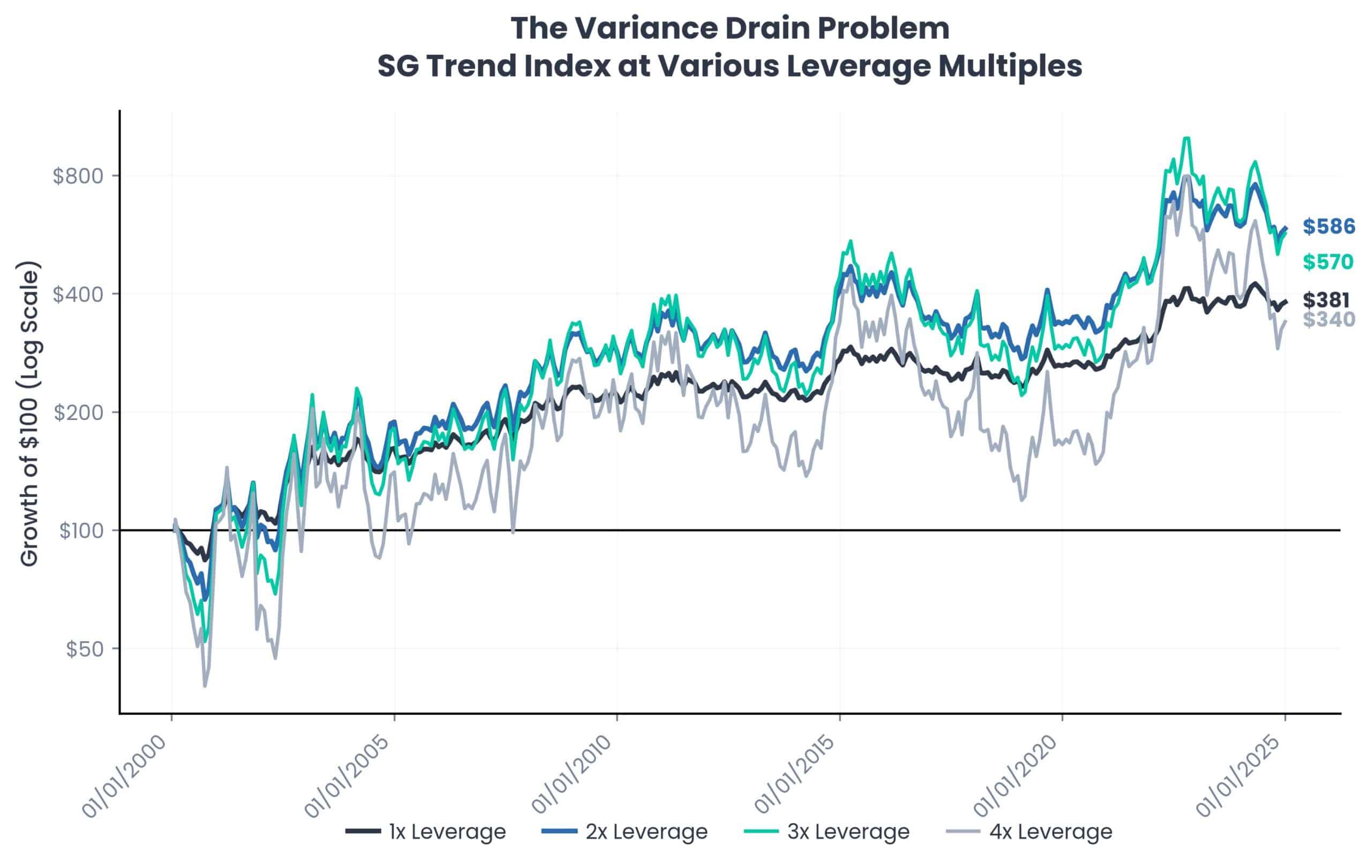

This approach introduces two underappreciated problems. First, higher leverage accentuates variance drain: the mathematical drag on compounded returns that increases with the square of volatility. At moderate levels, the additional exposure still improves outcomes. At 1x, the SG Trend Index delivered roughly $3.81 of cumulative growth per dollar invested since 2000; at 2x, this rose to $5.86. But at 3x, returns improved to only $5.70, and at 4x, they actually declined to $3.40, underperforming the unleveraged index (Exhibit 4). The mathematics are manageable in a portfolio context, where the higher-volatility fund is sized to a target notional contribution and rebalanced frequently. The problem is product salability: when the line item underperforms its own unleveraged benchmark, the conversation shifts from portfolio construction to manager due diligence, and the allocation becomes difficult to sustain.

Source: Bloomberg, Société Générale. Hypothetical growth of $100 invested in the SG Trend Index (“NEIXCTAT”) at various leverage multiples. Leveraged returns are calculated by scaling monthly excess returns (over T-bills) by the stated multiple and adding back the monthly T-bill return. Leverage is rebalanced monthly (i.e. the leverage multiple is maintained at the stated level each month). You cannot invest in an index. Returns are gross of all fees. Returns are gross of taxes. Returns assume the reinvestment of all distributions. Past performance is not indicative of future results. Period is 12/31/1999 through 12/31/2025.

Second, higher-volatility funds force the rebalancing burden onto the allocator. Because the fund is running at elevated leverage, the allocator must actively manage position size to maintain a consistent risk contribution. A return-stacked solution, by contrast, delivers the overlay at a target volatility within a turnkey ETF structure, so the rebalancing happens inside the product, not in the allocator’s portfolio.

Conclusion

For too long, the managed futures conversation has been stuck on how much and what to sacrifice to make room. Return stacking reframes the question from “what do I give up?” to “what can I add on?” For defensive allocators, the goal is building inflation resilience without surrendering equity upside. For growth mandates, it is the potential to pursue excess returns without the long odds of stock-picking alpha. More offense, more defense, same dollar.