Longevity is not a defining feature of the hedge fund industry. Wide performance dispersion, impatient capital, and a high fixed-cost base create a fragile equilibrium in which even short periods of underperformance or weak inflows can force closures. At first glance, the Nordic hedge fund industry appears relatively stable. Nordic hedge funds that shut down have exhibited an average lifespan of approximately 7.3 years, suggesting a reasonably durable ecosystem. Yet this headline figure is misleading.

The distribution of fund lifespans is markedly skewed. The median survival time is closer to 5.3 years, indicating that the typical fund fails well before reaching the “average.” A relatively small group of long-lived managers pulls the mean higher, masking the underlying fragility of the broader universe.

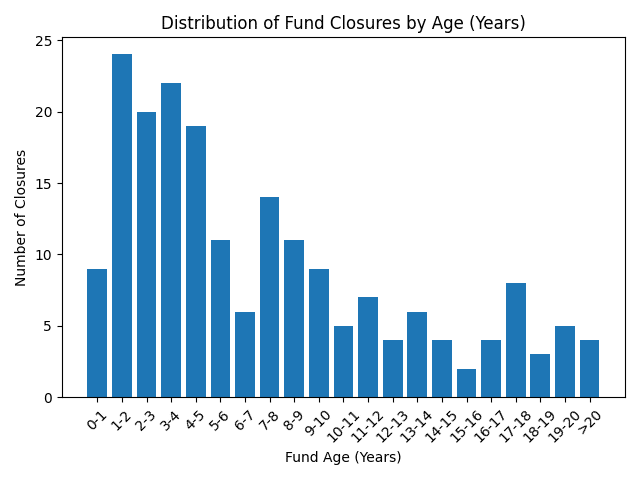

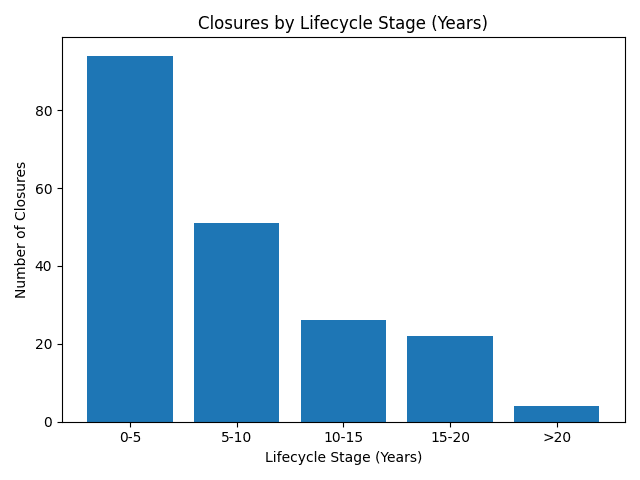

The lifecycle dynamics of Nordic hedge funds are not evenly distributed over time. Closures are heavily concentrated in the early years, pointing to a distinctly front-loaded risk profile. The majority of funds fail within the first five years, making early-stage viability, both in terms of performance and asset gathering, the single most critical hurdle.

However, passing this initial threshold does not eliminate risk. A meaningful number of funds continue to close between years five and ten, highlighting that structural challenges persist well beyond the startup phase. Even in the 10-20-year range, closures remain visible, underscoring that hedge funds are not “set-and-forget” businesses. Strategy relevance, team stability, and investor alignment must be continuously maintained, as even established managers remain exposed to eventual decline.

A complementary perspective comes from cohort analysis. Of the 169 hedge funds active at the start of 2015, only 55 remain in operation today, implying a survival rate of roughly 33 percent over the subsequent decade. This is particularly revealing because these funds had already navigated their early years. Yet two-thirds still exited the market, reinforcing the idea that attrition is not confined to younger vintages but continues across the lifecycle.

Of the 169 hedge funds active at the start of 2015, only 55 remain in operation today, implying a survival rate of roughly 33 percent over the subsequent decade.

A further layer of insight comes from examining the balance between fund launches and closures over time. Between 2015 and 2026, the Nordic hedge fund industry recorded an average of around 15 new launches per year, alongside approximately 17.8 closures. While this points to a degree of turnover and a modest net contraction in fund numbers, it also highlights the industry’s ability to continuously renew itself. New entrants steadily bring fresh ideas, strategies, and talent into the ecosystem, helping to sustain its relevance despite ongoing attrition. What may appear as stability at the surface level is, in reality, supported by an active cycle of entry and exit, where innovation and competition play a central role. In this context, the industry’s persistence reflects not just survival, but an ongoing process of adaptation and evolution.

The Nordic hedge fund industry recorded an average of around 15 new launches per year, alongside approximately 17.8 closures. While this points to a degree of turnover and a modest net contraction in fund numbers, it also highlights the industry’s ability to continuously renew itself.

Against this backdrop of high turnover, a distinct cohort of long-standing managers provides an important counterbalance, anchoring the industry with continuity and experience. Several Nordic hedge funds have built track records extending well beyond two decades, demonstrating an ability to navigate multiple market cycles and structural shifts. Systematic strategies run by Estlander & Partners now exceed 30 years, while Lynx Asset Management and Excalibur Asset Management has operated for more than 25 years. Other funds such as Brummer Multi-Strategy, Atlant Edge, Oceanic Hedge Fund, PriorNilsson Yield, Asgard Fixed Income Fund, among others, similarly exhibit longevity exceeding two decades.

This durability is not confined to a handful of outliers. A broader layer of managers further illustrates that long-term persistence, while uncommon, is achievable across a diverse set of strategies. Taken together, this cohort plays a disproportionate role in shaping industry perceptions, underpinning average lifespan metrics while providing a degree of stability within an otherwise dynamic and competitive landscape.

Importantly, these long track records should not be interpreted as representative of the typical fund experience. They are the outcome of a selection process rather than a baseline expectation. Only the most adaptable strategies, capable of navigating multiple market regimes, maintaining investor confidence, and scaling operations sustainably, persist over time. In that sense, longevity becomes a signal of resilience and adaptability, rather than simply a measure of time in the market.

Only the most adaptable strategies, capable of navigating multiple market regimes, maintaining investor confidence, and scaling operations sustainably, persist over time.

Taken together, the data points to a barbell-shaped industry structure. At one end, a large number of funds fail early, often within the first few years. At the other, a relatively concentrated group of managers achieves significant longevity, operating for decades and shaping industry averages. The space between these two extremes is comparatively thin, reinforcing the idea that the industry is defined by both high turnover and a stable core.

The implication is that the Nordic hedge fund industry operates less like a static ecosystem of enduring firms and more like a continuous selection process. Early attrition is high, mid-life risk remains meaningful, and true long-term survival is rare. Average lifespan figures obscure this reality, reflecting not the typical experience but the disproportionate influence of a small group of enduring managers.

For investors, the conclusion is straightforward. Longevity should not be viewed as a default expectation but as a differentiating signal, indicating an ability to adapt, endure, and remain relevant in a structurally competitive environment.