Since mid-2018, Philip Engel Carlsson has been running a systematic trend-following strategy focused exclusively on commodity markets. Three years ago, Calculo Capital introduced a second fund with a volatility target set at twice that of the original strategy. Now, Carlsson is preparing to broaden the platform further with two additional strategies: a 3x higher-intensity commodity strategy and a return-stacked product that overlays equity exposure on top of its flagship fund.

A Tiered Commodity Platform

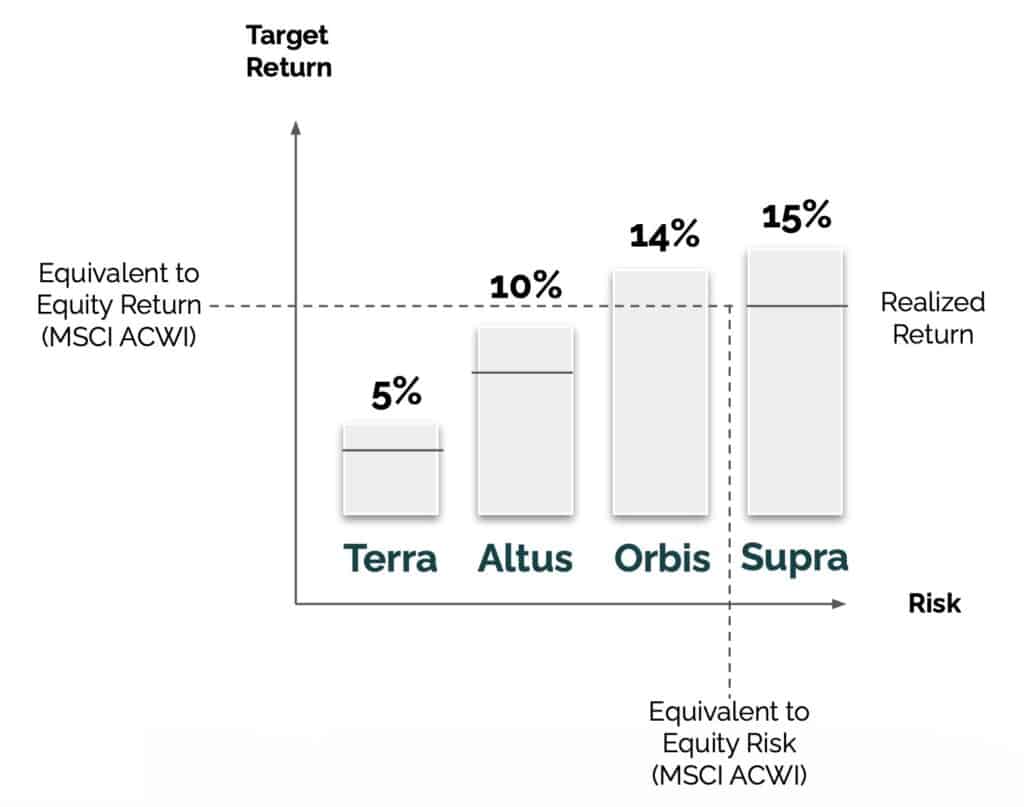

The foundation of the platform is Calculo Terra (formerly Calculo Evolution Fund 1x), which provides diversified commodity exposure with a strong emphasis on capital preservation and stability. The strategy targets annualized volatility of around 5-6 percent and serves as the low-volatility entry point to Calculo’s systematic commodity offering. The flagship vehicle today is Calculo Altus, the 2x version of the strategy, targeting volatility in the 10-12 percent range. Altus currently accounts for the largest share of the boutique’s assets under management.

“We have Terra, Altus, and Supra, all built on the same pure commodity strategy but with different levels of leverage.”

Scheduled for launch later in 2026, Calculo Supra will represent the 3x iteration of the strategy. Designed as a higher-intensity product, Supra aims to capture stronger momentum and breakout opportunities while reaching a more equity-like risk profile. “We have Terra, Altus, and Supra, all built on the same pure commodity strategy but with different levels of leverage,” Carlsson explains. “Supra is intended to complement Altus by offering a higher risk-return profile.”

From Diversifier to Return Stacking

All three strategies trade liquid commodity futures across energy, metals, agricultural commodities, and softs such as coffee, cocoa, and sugar. As is typical for futures-based strategies, capital requirements are limited to margin, leaving substantial cash balances. Most managers deploy this idle cash into high-quality interest-bearing securities to enhance returns. Altus, for instance, effectively combines 100 percent commodity exposure with an allocation to AAA-rated bonds.

While traditional trend-following strategies are often positioned as diversifiers to equity portfolios, Carlsson is now taking the next step. A soon-to-be-launched strategy, Calculo Orbis, will replace the bond allocation with direct exposure to global equities. The concept is rooted in return stacking: layering equity exposure on top of the commodity strategy rather than allocating to bonds. “Our strategy typically performs well during equity drawdowns,” Carlsson notes. “By layering equity exposure on top of our commodity performance, we aim to enhance long-term compounding.”

“Our strategy typically performs well during equity drawdowns. By layering equity exposure on top of our commodity performance, we aim to enhance long-term compounding.”

In practical terms, Orbis would combine exposure to Altus with approximately 50 percent exposure to global equity markets. Altus can already be viewed as a form of stacked product, pairing commodity exposure with a bond overlay. Orbis simply replaces the fixed income component with equities.

Backtested

Backtests extending to the launch of the commodity strategy in August 2018 suggest that the Orbis structure could enhance both return and risk characteristics. Over that period, Calculo Orbis would have generated an annualized return of 13.8 percent. According to Carlsson, the simulations show roughly a 30 percent increase in cumulative returns, alongside lower overall portfolio volatility and smaller drawdowns compared to a traditional equity allocation. “The result is a smoother equity curve,” he says, highlighting the improved compounding profile generated by combining commodity alpha with equity beta.

Because Calculo’s commodity strategy has historically acted as a stabilizer during risk-off episodes in equity markets, Carlsson argues that combining it with equity exposure in Orbis can enhance long-term compounding. “It allows us to compound from a higher base over time and thereby achieve higher overall performance.”