By Arne Simensen and Jakob Gravdal at Anchora Capital: In the Dutch Golden Age, Isaac Le Maire, initial largest shareholder in the world’s first publicly traded stock—the Dutch East India Company—launched a crusade against its monopoly after his 1605 ouster amid governance disputes. As history’s first recorded activist investor, he filed a petition for shareholder rights and transparency, pioneered short-selling to pressure reforms, and funded expeditions discovering Cape Horn to bypass VOC routes—pursuing fairer competition and value creation.

This early story of a shareholder activism to reshape a corporate giant echoes modern active ownership. In this Special Comment, we explore active ownership’s role as a value creator, sources of outperformance, and why active ownership can be particularly effective in the Nordic technology sector.

Active Ownership – A Source of Outperformance?

Active ownership strategies can take many forms, from voting at general assemblies to actively engaging with management and other shareholders, and ultimately taking formal roles such as board seats or launching activist investor campaigns to influence the target company or enlighten investors on financial shenanigans.

The United Nations, in their Principles for Responsible Investment (“PRI”) guide, notes that even basic activism, such as proxy voting and initial dialogues, positively impacts share performance by promoting accountability, ESG integration, and long-term value.

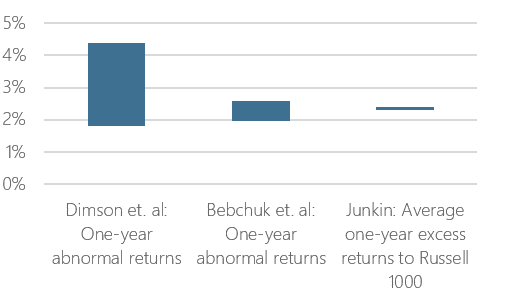

Elroy Dimson from Cambridge looked at how ESG engagement by active investors can drive superior returns. These engagements often have a broader motivation than traditional activism, as they seek among others the company to focus on its “triple bottom line,” corporate governance, and other matters. While this approach might be deemed “soft” by selected investors, it does potentially provide robust companies with sustainable growth patterns. In the study by Dimson et al., successful active engagement on ESG delivers strong results of 1.8-4.4% one-year abnormal returns.

A more activist approach further underscores the value of active ownership. A seminal study by Lucian Bebchuk from Harvard—The Long-Term Effects of Hedge Fund Activism—analyzed approximately 2,000 hedge fund activism events from 1994-2007, finding a sustainedpositive impact. In the study, targets experienced improved operating performance, higher payouts, and increased CEO turnover.

Target firms experienced improvements in profitability and efficiency, with three-year abnormal returns averaging 6-8% post hedge fund activist intervention. With a different angle, Brav, Jiang, and Kim (2015) further analyzed U.S. public firms using Census data, revealing 7-10% productivity gains through better asset allocation and labor efficiency in activist-targeted companies.

The activists’ approach also matters. An international study on hedge fund activism by Becht, Franks, Grant & Wagner (2017), find higher returns for wolf pack tactics. Several funds working together achieve higher returns than solo campaigns. Equally important, local activist funds tend to do better than foreign funds.

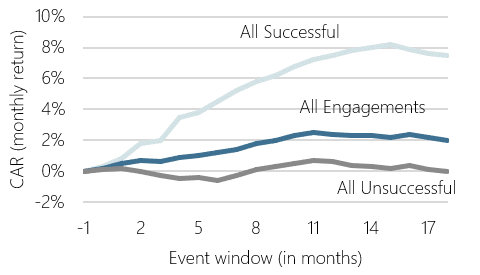

Less “noise” yields better returns

The California pension giant CalPERS demonstrated a positive impact with its “name and shame” approach in the Focus List. Here CalPERS named the companies with most potential to improve their governance standings among others. In “Update to the ‘CalPERS Effect’ on Targeted Company Share Prices” (Junkin 2015), companies targeted had a 12.3% average excess return to the Russell 1000 over a five-year period post engagement. More importantly, the companies targeted showed improvements in metrics like ROA, ROE, and reduced stock volatility, indicating that operational improvements should be the key driver behind the excess return.

CalPERS dropped the Focus List in 2010 however, in favour of private dialogue. The pension fund decided to shift course after research showed that companies responded better to being approached in private instead of being embarrassed in public.

Indeed, more recent studies, such as one conducted by Lazard Capital Markets Advisory (2023), point to declining effects of US activist campaigns. It may seem that a less confrontational, and more constructive engagement strategy yields better results.

Bill Ackman at Pershing Square, one of the World’s largest activist investors, announced in his 2021 letter to shareholders that they have permanently retired from the “noisiest” form of activism: activist short selling. They have also avoided proxy battles. While quiet, constructive engagement does not generate media attention, they are all the more productive, driving an exceptional run of returns for Pershing Square.

Active ownership at Anchora

We fundamentally believe active ownership, caring for the companies we invest in, is a force for good. Indeed, Øyvind Bøhren, prof. emeritus at BI’s Centre for Corporate Governance Research, claims the only type of board member there should be a quota for are owners. They are the only type of board member to make a significant positive contribution to shareholder returns. These findings mirror our own experience from active board work in the private equity setting.

However, we also find that taking up a board seat might not necessarily be the most efficient way to achieve results in a listed setting. We have already seen that working together with other owners (“friendly wolf pack tactics”) and engaging directly in private constructive dialogue with portfolio companies is a well suited approach in the Nordic small cap market.

The world of Nordic small cap technology companies is small, and therefore it is relatively easy to get an overview of the key players, co-operate, and build trust. At the same time, with an institutional set of funds that are mostly passive within Nordic small caps, it is also relatively easy to stand out from the crowd.

In our opinion, constructive, co-operative and active engagement with our portfolio companies has the best possible basis for success. Here the full breadth of Anchora’s strategy comes into play. Our in-depth industry research provides us with access to shareholders and management, where our well-founded opinions and perspectives create platform to impact as active investors.